A small number of quantifiable first principles in stock transactions, namely, the long-term value of equities, are equivalent to the depreciation of the enterprise's future free cash flow, which is the bottom line of justice for value investments and the underlying logic of buffett graham's life. I. Core essence

You buy a stock that essentially buys a part of the enterprise's ownership, the ultimate value of which depends only on the present value of the total free cash flow that the enterprise can create for shareholders during its lifetime。

There are two irreplaceable cores:

Why free cash flows rather than net profits

Since net profits are the product of accounting reconciliations, net profits can be glorified on credit, inventory, depreciation, and only free cash flows are the real silver and silver that an enterprise can truly dispose of and distribute to shareholders after all operating costs and capital expenses have been deducted

2. Why the discount

Because money has time value, today's $100 is worth more than 10 years later. The nature of the discount rate is your opportunity cost + risk compensation, the higher the risk-free interest rate, the higher the business's exposure, the lower the current value of the enterprise。

Specific formulas are as follows:

Enterprise free cash flow (fcff) formula: fcff = pre-tax profit (ebit) x (1 - tax rate) + depreciation and amortization - capital expenditure - increase in operating capital

Enterprise value (ev) = fcff1/(wcc-g)

Fcff1: expected enterprise free cash flow next year

Wacc: weighted average capital cost (discount rate)

G: long-term sustainable growth (generally not exceeding GDP growth)

In the short term, stock prices can be devalued by emotion, money, news; but in the long run, stock prices must return 100 per cent to the inherent value of the enterprise. In the last 30 years, all the shares that can get out of 10 years and dozens of times, without exception, have increased by more than 10 times the enterprise's free cash flow. There are, of course, many valuation systems for the characteristics of a shares and for realism, which can be explained in detail by reference to equity valuation methods and cases。

Ii. Demolition of real cases

1. Long-term value growth poles driven by free cash flows

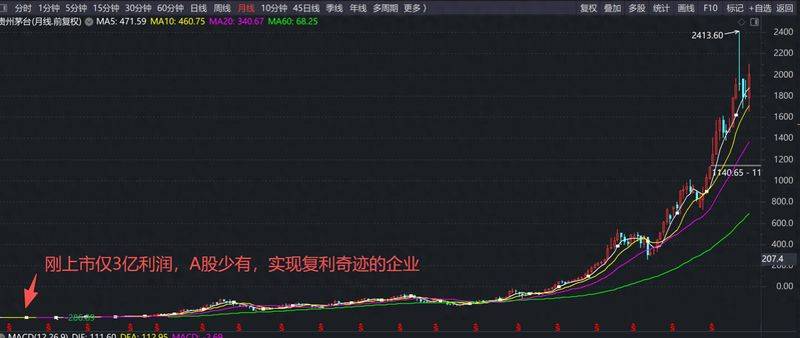

Guizhou is the most perfect proof of this principle, and even though it is now nearing the title of the “oldest”, time will at last reflect its value again. At the time of listing in 2001, company net annual profits were 328 million and free cash flows were 270 million; in 2024, net annual profits exceeded 80 billion, free cash flows exceeded 90 billion and free cash flows increased more than 330 times in 23 years. Correspondingly, their share price rose from $31 (post-rehabilitation) at the time of listing to a peak of $20,000 in 2024, an increase of more than 600 times, fully consistent with the increase in free cash flows. Even in the middle of the 2008 stockfall, the 2013 plastics crisis, the bear market, the short-term price cut short in 2022, the long-term highs of the free cash flow were perfect proof that "long-term stock prices must return to their intrinsic value."

2. Value foam bursting without cash flow

In 2015, bullsville's super-cow stock was fully educated, with the concept of “online education” rising to a maximum of $467, a market value of over $50 billion and a market gain of over 1,000 times. But the essence of it is a collection from mergers and acquisitions, which has never created a stable free cash flow of 120 million in 2015. The final concept bubble burst, the value not supported by the cash flow collapsed completely, the stock price fell by a minimum of 1. 6 dollars, over 99 per cent, and eventually came out of the market, perfect proof that “the value of the free cash flow is all in the sky”。

Iii. Empirical revelation

At the heart of long-term investment is understanding the business model of an enterprise: can it continue to create free cash flows? Does its moat guarantee that future cash flows will not be eroded by competitors? If you do not understand this, you do not have to hold it permanently

2. The error in the investment of the periodic share is precisely contrary to the principle that the highest profits of the enterprise at the top of the cycle are often the worst expected cash flow in the future, as the industry is overcapacity, prices are about to fall, and buying is the switchboard

Do not pay a high premium for “concept” and “story”, and the concept that is not supported by cash flows will end up as a chicken hair, either on the internet in 2015 + or on ai in 2023, and will end up with no return to value。

Iv. Common error zones

By equating short-term profit growth with long-term value, the market share, the size of the revenue, and the core competitiveness of the enterprise, the enterprise's ability to translate these into sustained free cash flows is overlooked。

V. Simplified trading procedures

One, only "real money" and no books

The valuation first focuses on free cash flows rather than on net profits, with businesses that are on credit, with windfall profits, with high capital expenditures, directly disallowing their eligibility for valuation。

2. Simplified discount rate without precision

Without complex calculations of wacc, direct no-risk interest rates + enterprise risk premiums: the more stable the firm, the deeper the moat, the lower the discount rate; the higher the risk, the more the industry becomes。

3 - future growth is not guessed, tops, GDP growth

Lasting growth rates must not exceed GDP growth rates, overestimate the long-term growth of enterprises and avoid miscalculating the valuation。

4. Valuation first screens, then figures

Only enterprises with free and sustainable cash flows, with moats, are valued, with pure concepts, no profit, no negative cash flows, and no valuation, no participation。

5. Periodicity shares look backwards without top valuation

At a time when future cash flows are well-valued at the top of the cycle, there is a strong determination not to pay high premiums to current cash flows。

6. Ignore short-term fluctuations and anchor long-term returns

Equity prices deviate from valuation in the short term with funds and emotions, and long-term stock prices will inevitably rise simultaneously as long as the enterprise's free cash flow continues to grow, leaving open short-term discounts。

Seven, set the valuation floor. No foam

High valuations and subject matter shares, which are not supported by stable free cash flows, are considered to be of no intrinsic value and no premium is paid。

Investments are risky and market entry requires caution. This is a reference, not superstition

Ps: today is my girl's birthday. Happy birthday to her