The amiba business is a model of financial management created by rice and husband in japan, based on the idea that "everyone is an operator and is fully involved in the business", allowing everyone to look at the problems in the business and give value to the smallest unit, also known as the system of independent accounting for small sectors. Essentially, the following features are included:

I. Delineation of minimum operating modules

Each enterprise has different organizations, and some enterprises can divide costs into different sectors. Amiba, on the other hand, operates on the premise that it divides the smallest business units, bringing revenues, costs and costs to the smallest organization, such as “one group, one production line”. This allows the smallest units to be involved in the operation and to find problems in the smallest organization to the point where there are gods on the ground。

It's not the smallest structure, but the smallest in business

Ii. Employment is valor, not cost

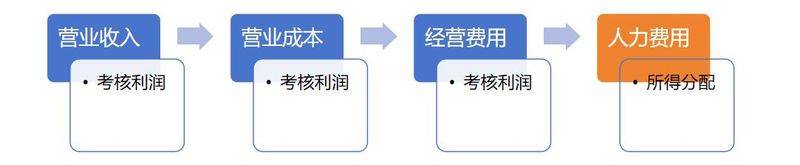

The focus of amiba operations on distinguishing between traditional financial accounting is the redefinition of value added, i. E. “additional value = operating income - operating costs - operating costs” and excluding human costs. They see human costs as wealth created by enterprises (like china) and as value creation, not a burden on enterprises。

Difference in human costs

The exclusion of human costs does not mean that they do not value this part of the expenditure, but some enterprises increase human expenditure after adding value to measure their impact on profits

Time accounting

As amiba does not have human costs, the actual analysis needs to take into account the impact of the person on the operation, on this basis the staff member's time of attendance has been increased, i. E., “the value added per unit time (the value added per unit time = value added/time of attendance)”. Enterprises ' wealth and attendance are measured in terms of the value created per hour。

Unit time accounting

The focus of unit time accounting is that all people are equal, with a monthly pay of 10,000 and 5,000 hours of attendance of eight hours each, and the value they create in unit time accounting is a striking feature。

Iv. Increased internal transactions

Each enterprise has its own business and logistics units, but without exception, is a salesman, and whoever earns money has a reason. However, the amiba operation redefined the process of creating the value of the enterprise, i. E. That value creation is the result of a joint effort by all sectors and not the achievement of a sector in the final marketing sector. Therefore, for non-operational logistics units, there is a need to increase the contribution of their operations in a way that achieves a balance of value and profit-sharing, in the form of “internal transactions”。

Cases of internal transactions

The bottom line of internal transactions is that the turnover of the marketing sector is done in a range of sectors, such as production, research and development, and finance. If a turnover of $10 million is generated, the production sector can be raised by 1 per cent, the research and development sector by 2 per cent, and the corresponding sales sector by 1 per cent or 2 per cent. While the logistics sector does not produce performance directly, its contribution to performance is reflected through internal transactions。

V. Budget and planning

On an annual budget basis, amiba operations also need to complete monthly projections, i. E., the current forecast for next month's operations, the forecast for next month and the budget for the current month, to increase the level of recognition or sensitivity of the budget。

Conducting business analysis

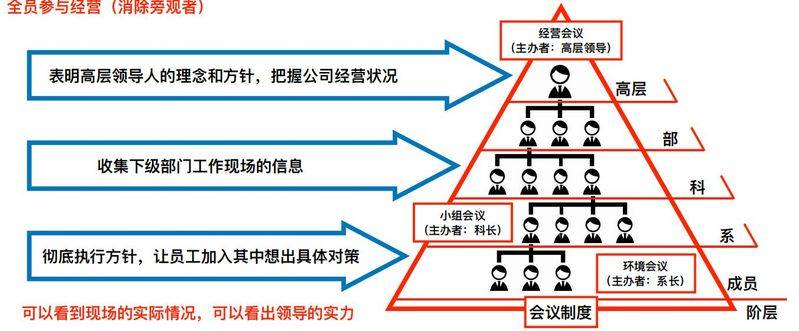

Business analysis is generally done by the main sector or financial sector. However, the analysis of amiba's operations was completed by the business modules, each of which analysed its own strengths and weaknesses during the period and identified problem points and improvements, leading to the completion of the company's performance. The monthly business analysis therefore requires departments to start with each number and to find gaps in detail。

Elimination of bystanders

Final: strengths and weaknesses

The following points should be taken into account: (1) the theory of unit time accounting and increased time spent on duty; (2) the value added, which treats staff as value creation rather than as a burden on the enterprise; and (3) internal transactions, which consider contributions to logistics。

Possible problems: 1 — the requirement for accuracy and timeliness of data is extremely high — and the most basic work cannot be done if an enterprise fails to do both; 2 — the requirement for staff is high, and not only is it not valuable if the business sector is not sensitive to figures; and 3 — because of the impact of internal transactions, it may also create a situation of internal push and cross-fertilization。