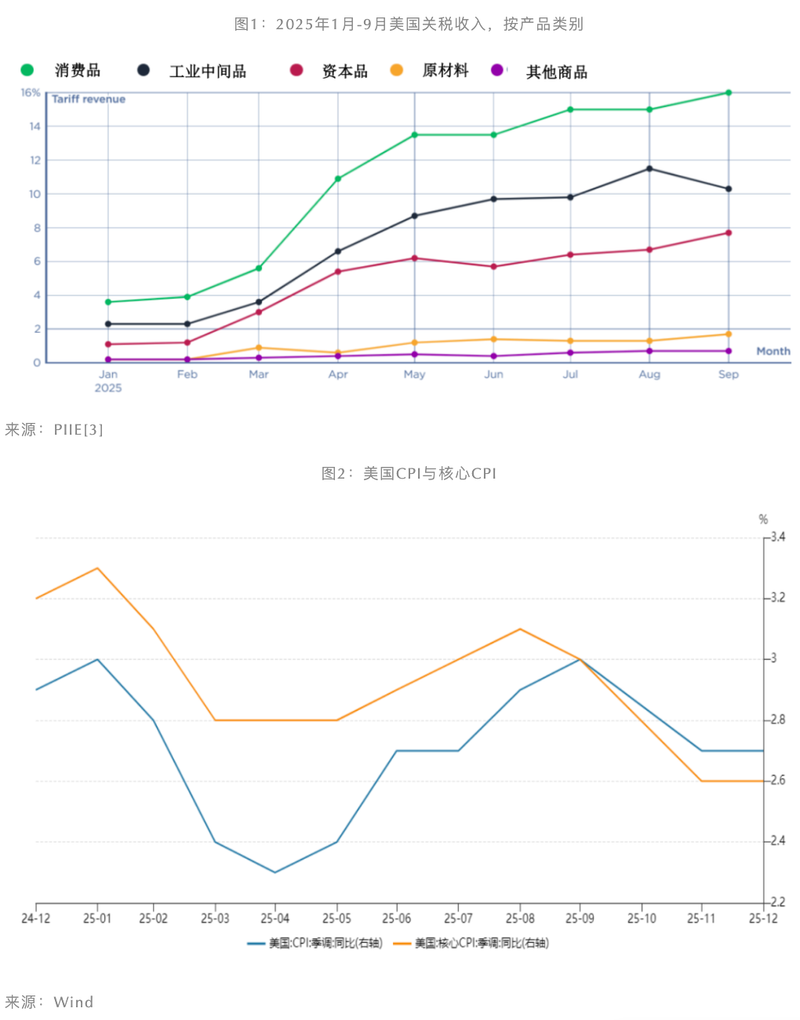

According to the united states department of the treasury, united states tariff revenues grew rapidly in 2025. Throughout 2025, the united states department of homeland security collected $28. 7 billion in customs duties and fees, an increase of 192 per cent over the same year. Of these, about one third increased in the fourth quarter, up 5. 2 per cent from the previous quarter。

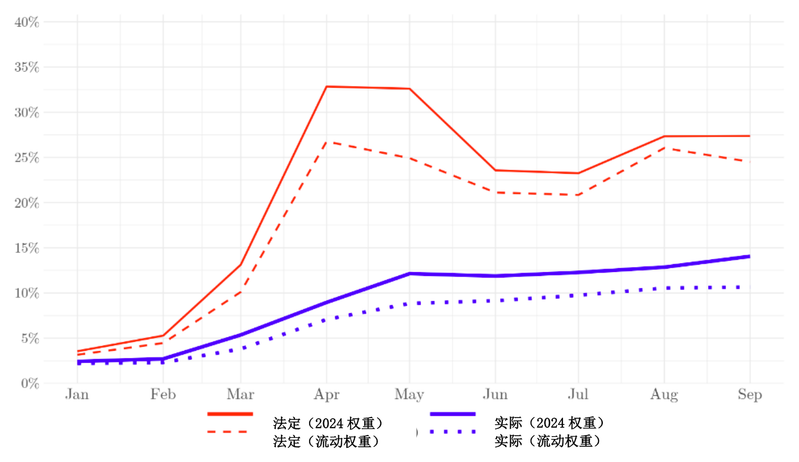

At the same time, inflation in the united states, while still significantly above the target level of 2 per cent, has not surged. After rising to over 3 per cent at the beginning of the year, the consumer price index (cpi) began to fall in mid-year and stabilized at 2. 7 per cent at the end of the year. The core cpi after the elimination of food energy increased by 2. 6 per cent over the year, well below the 3 per cent previously expected by economists. The personal consumption expenditure price index (pce) increased by 2. 8 per cent in november and the producer price index (ppi) by 3 per cent in november。

Why didn't tariffs cause inflation to soar

There are several main explanations for why tariffs have not led to soaring inflation:

Reason 1: actual tariffs are much smaller than statutory rates

To date, the united states has implemented tariff policies on a much smaller scale than it claims。

According to studies by the former first vice-president of the imf and professor of economics at harvard university, geeta gopinate, and professor of economics at the university of chicago, brent neiman, the actual tariff rates imposed by the united states are significantly lower than the officially published statutory rates。

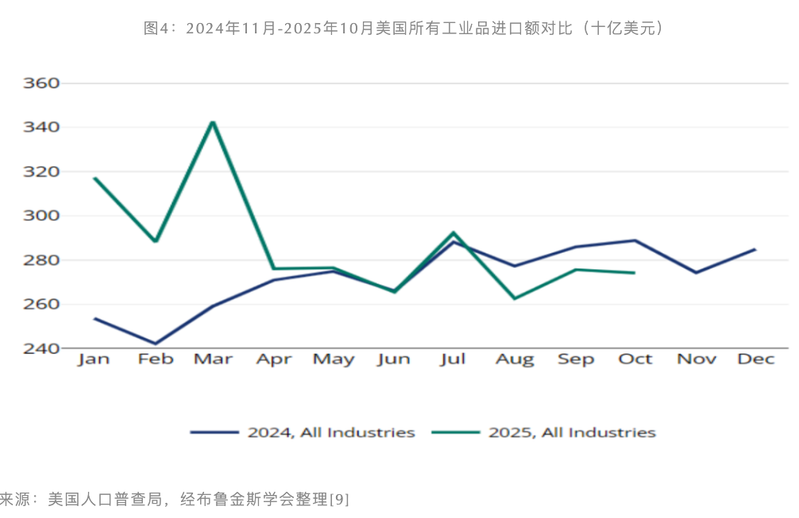

As of september 2025, the united states average trade-weighted tariff rate peaked at 32. 8 per cent in april 2025. However, when the actual tariff rates obtained by dividing the total value of imported goods by customs revenues were only 5 per cent in march, the actual tariff level rose gradually, reaching 14. 1 per cent at the end of september, about half the legal rate for the same period。

Estimates from the yale university budget laboratory also found that, as at 17 november 2025, the overall average effective tariff rate faced by united states consumers was 16. 8 per cent, and that the average effective tariff rate was 14. 4 per cent, after considering that importers minimized tariff costs by adjusting their procurement channels。

This gap is due to a number of factors:

One is the delay in transport. At the time of the issuance of the new tariff policy, part of the goods already in transit were still taxed at the old tariff rate, and this “in-transit exemption” meant that the new tariffs would not immediately be reflected in all imported goods, particularly seaborne goods, which took several months。

Second, many commodities and enterprises were granted tariff exemptions, including medicines, electronics, semiconductors, bananas, coffee, etc., in view of repeated delays, withdrawals and cuts in tariff policies。

Third, differences in enforcement and tariff evasion may also lead to a gap between statutory and actual tax rates. According to the richmond federal reserve study, the difference between statutory and actual tariffs as of may 2025 was due in part to delays in enforcement, incomplete updates of customs systems and the application of zero actual collection rates for some products that should have been subject to high tariffs. A small part of the reason is the shift of importers'sources of procurement from china, which faces high tariffs, to regions such as viet nam and the european union, which have lower tariffs。

Reason 2: enterprises delay price increases through early import and use of stock strategies

The study found that enterprises imported early between the november 2024 general elections and july 2025, which resulted in large stocks of commodities. Thus, even after full entry into force of tariffs, most retailers are able to delay orders and raise prices by consuming lower-priced stocks。

Data on imports of goods by the united states census bureau up to october 2025 indicate that “run-off” by enterprises began to accelerate at the end of 2024 and peaked in the first quarter of 2025. As part of the tariff came into effect in april and may, import surges receded rapidly and imports began to fall below historical levels after july。

The united states total imports in the first quarter of 2025 were 26 per cent higher than historical trends, as measured by the budget model of the university of pennsylvania's wharton school of business. As of may, this “run-off” strategy is expected to save importers as much as $6. 5 billion, equivalent to 13. 1 per cent of the new tariff revenues of the united states。

In terms of specific imports, the bulk of imports include gold, pharmaceuticals, semiconductors, auto parts, steel aluminium, mechanical equipment and industrial goods。

In the case of country-specific imports, such raids occurred first from china. As the market expects tariffs on china (e. G. Fentanyl tariffs) to enter into force as early as february, imports from china by united states enterprises surged by about 35 per cent in january 2025 and fell back after fentanyl tariffs landed in february。

From january to july 2025, the cumulative united states imports from china decreased by 16. 9 per cent compared to the same period in 2024, according to the peterson institute for international economics (piie). During the same period, the united states also increased imports from countries such as the european union and viet nam。

After the united states government announced delays in “reciprocal duties” in april and july, united states importers continued to hoard from non-china areas such as viet nam and india until july. The centre for global development (cdg) suggested that by july 2025, cumulative united states imports from asia outside china had increased by more than 40 per cent, more than twice the same level in 2024。

In addition to pre-positioning, importers use warehousing instruments such as bonded warehouses and foreign trading zones to delay tariff payments and wait for tariff adjustments during periods of trade policy volatility. According to warehousequate, the demand for bonded warehouses and warehouses in the external trade zone increased by more than 150 per cent in the first quarter of 2025, and the rent of the bonded warehouses doubled the price of the general warehouse rental compared to the same period in 2024。

Reason 3: importers have not yet started significant transfer costs

Various studies indicate that the cost of tariffs is currently borne almost entirely by united states enterprises and that exporters do not share the cost through price reductions. At the same time, prices have not risen significantly, which means that united states enterprises absorb tariff costs by compressing profits, thereby delaying the transfer of costs to consumers。

The kiir institute of world economics, which measures unit import prices based on bill of lading data on united states maritime imports from january 2024 to november 2025, and corresponding to official united states tariff schedules, found that foreign exporters barely absorbed tariffs by lowering prices, absorbing only 4 per cent of tariff costs and passing the remaining 96 per cent to united states importers。

A survey conducted by the fed in richmond between early 2025 and august found that many enterprises had expressed caution about price increases before tariff policies became clear, for fear of demand reduction and loss of market share. Moreover, most enterprises are in the phase of demand elasticity testing and are more inclined to adopt “step” price increases, such as small price increases once or twice, to observe whether consumer demand is stable or, if demand is stable, then again in two months. Finally, many enterprises do not adjust prices frequently because of such factors as annual contracts or pre-sale。

Reason 4: tariffs tend to transmit macrodata more slowly in

To date, the impact of tariffs on retail prices has been gradual. A study of real-time price data by scholars such as alberto cavaro, professor at the harvard university business school, based on large united states retailers, found that tariff-affected commodity prices began to rise in april 2025, that imports rose 5. 4 per cent over pre-tariff trends between march and september and 3 per cent over pre-tariff trends over united states domestic goods due to reduced competition。

Historical experience shows that tariffs are slow to transmit macroeconomic data. On the basis of an analysis of the effects of the 2018-2019 trade war, only tariffs of about 20 per cent can be seen to be fast and significant to prices. If final tariffs remain at 10 per cent, it is expected that very slow price transmission will continue to be observed, with consumers likely to notice price increases of around 10 per cent in a few years or more。

According to a study by the federal reserve of dallas based on trade disputes in 2018-2019, tariffs on final consumer goods usually lead to a one-time inflationary shock, while tariffs on intermediate inputs lead to more lasting inflationary effects。

Other reasons

According to jeffrey franker, professor at the kennedy school at harvard university, part of the cpi data is missing as a result of the united states government's suspension from 1 october to 12 november, which prevented the bureau of labor statistics from collecting data as usual. It is therefore reasonable to suspect that, in the absence of partial data, inflation in housing costs may be incorrectly recorded as zero, which would lead to a lower overall cpi valuation。

Next steps in the impact of tariffs in 2026

Many analyses suggest that 2026 will be the year when the impact of tariffs will become apparent, that enterprises will have to begin transferring tariff costs to consumers, and that the impact of tariffs will be further reflected in macro-data such as inflation。

1. U. S. Enterprises had to start transferring costs

By 2025, enterprises had accumulated large amounts of low-cost stocks before tariffs came into effect, and that advantage would no longer exist in 2026。

According to united states census bureau data, as of october 2025, the overall commercial stock sales ratio in the united states (i/sratio) was 1. 38, indicating controlled consumption. In december 2025, inventory levels in the logistics economy index stood at 35. 1 per cent, the fastest rate of cargo consumption since the index was created at the end of 2016. Warehouse utilization has also fallen to a new historical low of 42. 9, indicating that enterprises are rapidly moving from a precautionary to a lean, punctual model。

According to a brown paper published by the federal reserve in january 2026, many enterprises reported that pre-tariff stocks had been depleted or were in the process of being depleted, which meant that enterprises would have to make up for the goods at higher prices. In the face of increased cost pressures, firms have to choose to sacrifice their profit margins or to shift costs to consumers。

Many businesses in atlanta are expected to raise their prices in the first half of 2026 in order to maintain their profitability, especially those that have maintained stable prices in 2025. Various industries in the boston region are also planning selective price adjustments in the coming months, ranging from the pharmaceutical industry to some consumer goods, with increases ranging from 1 per cent to 5 per cent to 10 per cent。

In addition to consumer prices, as intermediate inputs continue to flow to manufacturing prices, the ppi will also continue to face pressure in 2026, and the increase in ppi will eventually be reflected in retail prices. Recent global surveys of the scale-up show that manufacturers have had to raise prices because of higher input costs。

2. Whether tariff impacts will be further reflected in inflation data medium

Major financial institutions were generally cautiously optimistic about the macro-impact of tariffs in 2026. Goldman sachs has even argued that the inflation problem in the united states has been resolved and that, as the base figure effect recedes, the effect of tariffs on inflation will decline sharply from the second half of 2026。

However, some scholars consider this optimistic projection to be an erroneous reading of the impact of the policies of the trump government. Economists such as frankle have pointed out that the effects of tariffs are slow, that the seemingly stable state of 2025 is only a illusion of corporate stock reserves, profit compression, and policy expectations, and that the effects of continued high tariffs are expected to be evident in macro-data starting in 2026。

Person expects that the “stagnating” effect of the trump policy portfolio will become clearer in 2026 and that by the third quarter of 2026, cpi inflation may rise to 4 per cent or higher. As pre-tariff stocks are depleted, immigration policies lead to labour shortages in such areas as nursing, food processing, construction, etc., the supreme court ruling, trade negotiations, etc., have become clearer, enterprises will be forced to shift tariff costs to consumers and substantially raise wages and become paralysed in decision-making by watching tariff policies enterprises will also start pricing adjustments by taking into account long-term tariff costs。

At the same time, in the context of supply-side constraints imposed by tariff and immigration policies, continued ai investment booms and fiscal stimulus policies are exacerbating inflationary pressures; expectations that the trump government will undermine the fed’s independence may also lead to a relaxation of inflation expectations and further increase the adhesiveness of inflation. The impact of these factors will go beyond the downward factors of inflation that are of concern to the market consensus — the continued decline in housing inflation and the rise in productivity。

The first money was authorized to be reproduced from the china finance forty-people's forum。