In beijing, on may 24, china (journalist ko qi-sung wang) reported that life insurance has been an important component of family insurance, with the insured's life insured and the insured's survival or death guaranteed for countless families. How can products fit for themselves be selected? What's the beauty of a flat life risk and an increase in life risk? The moderator, mr. Ko, was a senior global insurance planner。

Life insurance must be "forever"

“there is no product that solves all the problems, and each product has its own application scene”, and it is argued that periodic life insurance is more functionally focused on safeguards. Groups with the greatest household economic responsibility and the least risk-resistant are often in need of adequate security at a lower cost, while periodic life insurance has a high-value ratio of “small expenses, large security”, combined with flexible configurations, multiple durations, diversified products and needs-based combinations, which are the immediate needs of people with “family liabilities”。

A long-lived "rich housekeeper"

In the age of longevity, “100-year-old life” is likely to become normal. There are a wide variety of concerns, such as “in case the goals and dreams are not fulfilled”, “in case the promises to families are not fulfilled”, “inventory medical care costs and pensions are inadequate” and “accumulated wealth is poorly planned and shrunk”, and these needs, covering the entire life cycle, can reassure you by taking on a life-long life risk that covers most of the family responsibilities in life。

During periods of heavy responsibility, the family's economic pillar, such as extreme personal risk, can continue to provide for the daily life of the family, the education of children, housing support for the elderly, etc., and the family's economic pillar's income for the family's future is realized ahead of time。

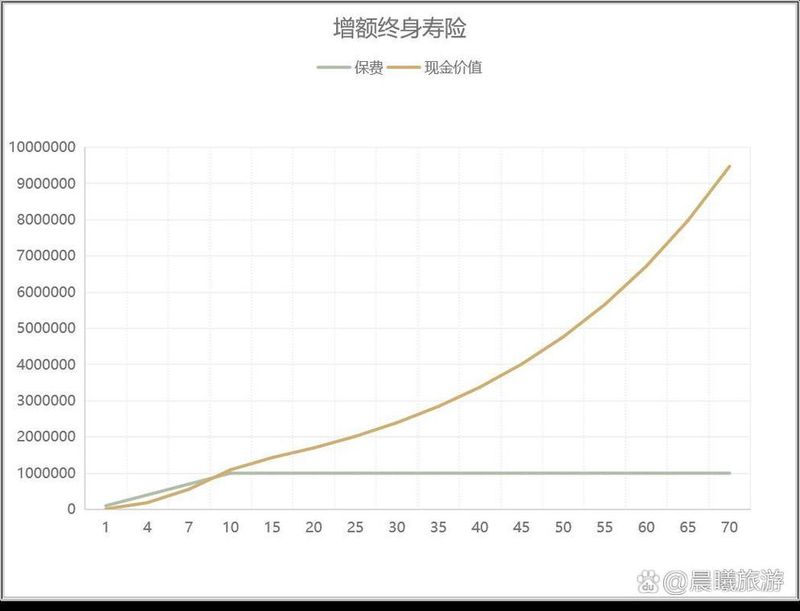

During retirement, life insurance can address three main risks: old age, illness and disability. Lifetime insurance has the function of adding value to savings, with a higher value of later cash and a significant amount of money in the future that can be used as a supplement to old age。

What are the options for the increase in vs life expectancy

The quota life risk is based primarily on the risk of displacement, while the main effect of the increase is on the risk of long life。

Insurance should be considered in three respects. First, consideration should be given to the financial situation of the individual, and the choice of a fixed life risk that is more stable and accessible if the financial situation is tight; secondly, to the health status of the individual, his/her health is better and his/her age is lower, the option could be to increase the level of security over his/her life risk over time; and thirdly, to family financial planning, the choice of a fixed life risk would make it easier to plan family finances over the long term, but the increase would be better able to meet future needs if there were large expenditures at some point in the future, such as the education of children, the purchase of property, etc. If the financial conditions of the insured permit, the two may be combined。