I've been asked by a lot of friends recently to say, "do you want to buy some regular life insurance and raise the price of new products?"

I understand this anxiety. After all, money is involved, family security is involved, and nobody wants to “buy expensive” or “buy wrong”。

Let's talk about this today. - why? How much? What do we do now

First of all, the conclusion is that this is not a “cut-off” job, but a real product overlay。

In late march, a series of internet periodic life insurance products will continue to be installed. For example, the 2026 periodic life insurance for chinese barley, the 2026 periodic life insurance for sweets were suspended on march 21, and the rich people will also retire by the end of march for the 7th sea column and the 11th chinese life pillar。

Once these products fall, the insurance company will launch a new version, but the premium will follow。

What's the increase? The basic anchor is around 7%。

For example, the global “love 2026” internet is scheduled to expire on 1 march, and the new edition is online on 10 march, with a full 7 per cent increase in premiums under the same safeguards. Data for other platforms are similar, in part more than 7 per cent。

The first reaction of many people to see this is to buy it

Don't worry. We need to figure out why it went up. It's more important than buying。

Reason one: tax policy has changed, costs are passed directly to consumers

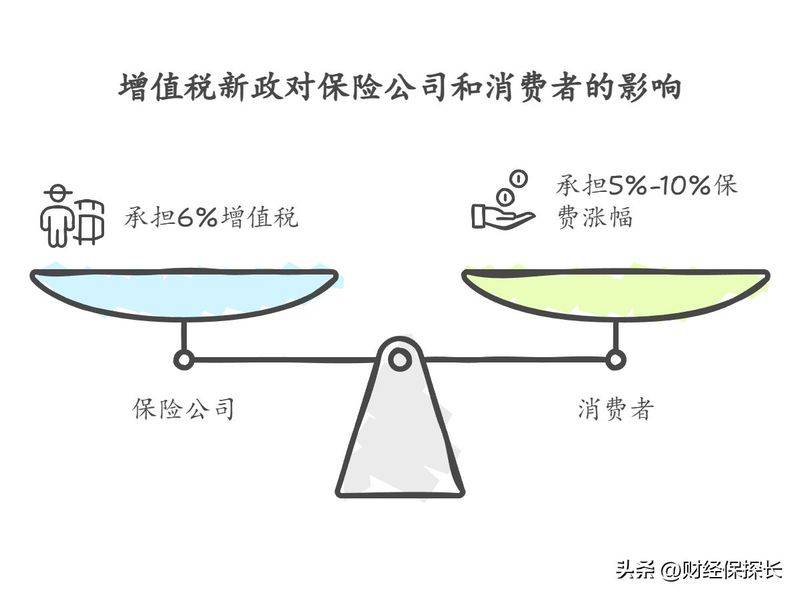

Since 2026, the new vat policy has made a key adjustment — non-refundable periodic life insurance, which is no longer tax-exempt。

What is a non-repatriation type? It's a pure-assured product that “exempts during the security period and does not fall due”. This is basically the logic of periodic life insurance。

A 6 per cent additional vat has been added, which insurance companies have to cover. However, the product structure of periodic life insurance is relatively simple, unlike the fact that some complex products can absorb taxes through internal offsets, so the 6 per cent final rate is transmitted to consumers in the form of a premium increase of 5 to 10 per cent。

Let's be clear: the knife is policy-relevant, and the insurance company can't handle it entirely。

Reason two: disbursement rate is problematic and actuarial pricing is forced to increase

Many think that life expectancy is now increasing, that insurance companies should be less pressured to pay, and that premiums should be reduced。

That logic is correct, but reality is more complex than theory。

The core clients of periodic life insurance are often young and middle-aged people between the ages of 30 and 50, especially the economic backbone of the family. While the overall life expectancy of this group is increasing, the problems of high-pressure work, sub-health and the risk of sudden death have been prominent in recent years. Data on actual payments show that the mortality rate in this age group does not decline simultaneously with the increase in life expectancy。

When pricing the product, the actuary does not simply reproduce the lifesheet data, but adjusts them in the light of historical recovery experience. When the actual rate of payment is higher than expected, the pricing will naturally have to be improved。

That is why the new version of life clearly reflects an increase in life expectancy, but instead the premium has increased — because “a longer life” and “a lower risk of payment for this group” are different things。

Reason three: pre-set interest rates are reduced, squeezing the pricing space of the product

That's a little technical, but let's try to be clear。

The insurance company collects your premiums and invests them. The higher the investment returns are expected, the cheaper the pricing will be. In recent years, however, the overall investment climate has been downgraded, and regulation has continued to reduce the interest rates set for insurance products。

Once the interest rate is reduced, it will be equivalent to less than the insurance company's “expected gain” and the premium will have to rise in order to remain operational。

It has been measured by professionals that the pressure of the downward revision of the scheduled interest rate as a result of this round is substantially greater than the “dividend” of the life schedule. In other words, the increase could have been more than 7 per cent if it had not been offset by an increase in life expectancy。

Speaking of which, many might ask: what does a 7 per cent increase mean

Let's figure out a specific number。

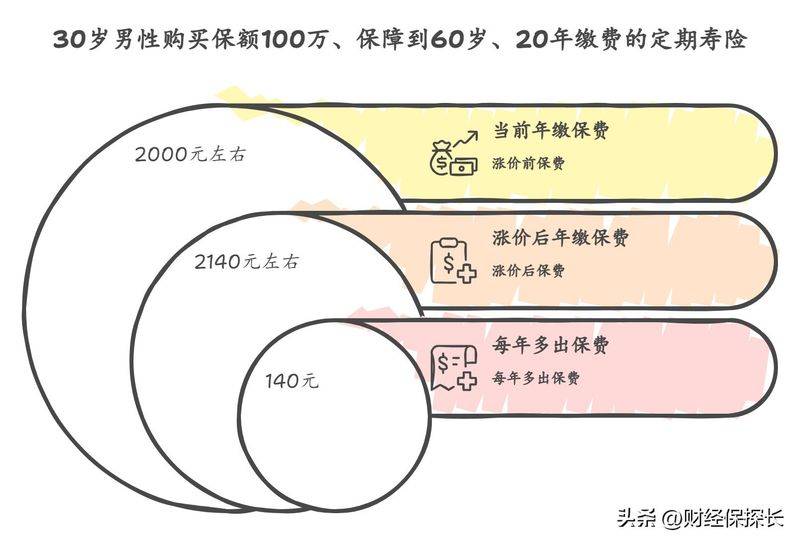

Assuming that a 30-year-old male buys a periodic life insurance rate of 1 million, guaranteed up to age 60 and 20 years of contributions, the current year's contribution is around 2000 yuan (slightly different products)。

After an increase of 7 per cent, the annual contribution became about $2140, an additional $140 per year, or less than $12 per month。

You're saving a million. Would it be entirely acceptable to spend an extra $12 a month for this $1 million

This is also why many insurance practitioners would say that the increase in the price of periodic life insurance is actually very limited in actual perceptions. Most people feel no difference without a reminder。

This, of course, is not to say that “price increases don't matter”, but rather to remind everyone that it is the right way to open it by not being taken away by the mood of the stoppage, and by being cool about whether they really need it。

Returning to the most fundamental question: do products such as periodic life insurance have the necessary configuration

My answer is: for those with family responsibilities, it is almost obligatory。

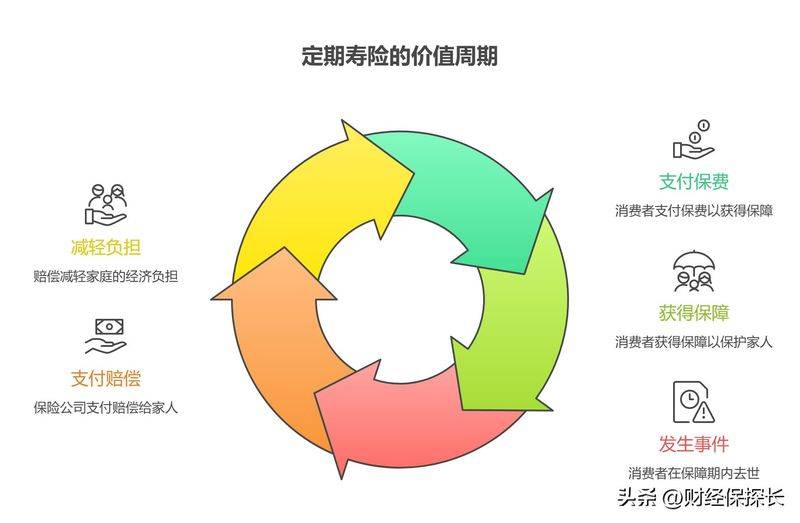

The logic of periodic life insurance is pure -- you pay a small amount of money in exchange for a promise that the insurance company will pay a sum of money to the family in the event that it leaves during the security period。

What's this money gonna do

There is no alternative to this guarantee, which is aimed at “the premature death of the family economic pillar”。

Many feel they are young, healthy and less likely to happen and do not need to buy. But it is this “low probability” that the cost of periodic life insurance will be so cheap. The risk of extremely low probability but very high destructive impact at a very small cost is the significance of insurance。

Even with this round price increase of 7 per cent, periodic life insurance remains one of the most affordable guaranteed products on the market, without change。

What do we do now

First, there is a real need, which has not yet been purchased, and it is possible to consider entering the old version before closing down。

The focus is on “real needs”. If you have an old man and a small family, you have a loan, you have a family income. It's real if you buy it before the price rises。

Secondly, they have already been bought for a fixed life, without anxiety or easy switching of products。

The products that have been configured should remain in possession, and there is no need for a “new version”. A change of product would mean re-insurement, and in the event of a change in physical condition, it could be subject to additional fees or denials。

Thirdly, it is not for decision to be kidnapped by “sold off” emotions。

Cut-off is the normal rhythm of product overlaps, almost every year. It's the best that suits you, not the best that closes。

Fourth, pre-purchase coverage is recommended。

The higher the premium, the less the less it is. Reference is made to the total household debt (loans, car loans, etc.) and to the annual household income of three to five years as a reference for the base guarantee. This is neither excessive insurance coverage nor inadequate safeguards when really needed。

Finally, the matter of insurance has never been about catching up with hot spots and stopping sales。

It is a safeguard tool that needs to be calm, rational and long-held。

This round of periodic life insurance rose by 7 per cent, with the combined effect of tax policy adjustments, data pressure on payments and changes in the interest rate environment. It happens, and it follows, and it reminds us that the costs of safeguarding can only be higher, not lower, in the future。

Early planning and allocation are the most responsible for themselves and their families。