In the category of life insurance, “periodic” and “lifelong” who is better has been the subject of debate. Ordinary people find life insurance too expensive and unnecessary, and rich people feel that regular life insurance coverage is inadequate and not compensable。

But in 2026, the difference between the two was no longer as simple as "suspension" . In essence, this is a choice between “consumption” and “asset allocation”。

1. What is the nature of periodic life and lifetime insurance

One sentence:

Periodic life insurance = risk hedge tool to prevent families from falling due to the fall of the pole at low cost. Lifetime insurance = a means of passing on wealth to ensure that money is left to a named person sooner or later。

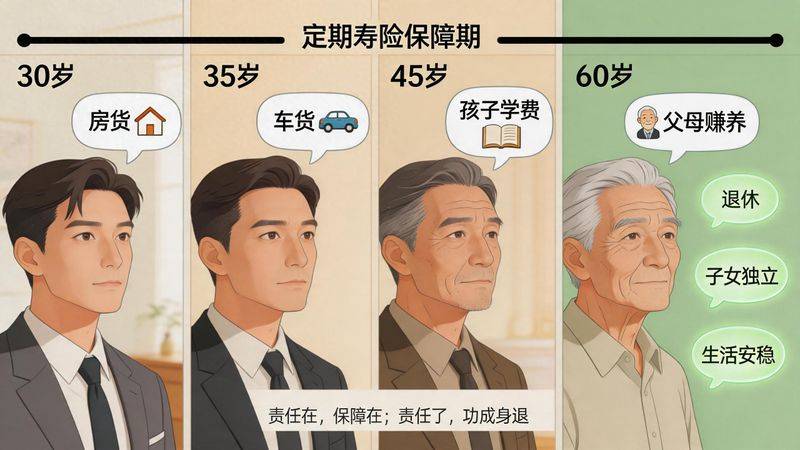

2. Why is regular life insurance preferred for ordinary families

In summary, low premiums and high premiums are the most useful “financial safety net” for ordinary households。

Why is life-long life insurance a “fresh” for rich people

In the eyes of high net value groups, life insurance is not insurance, but a “cash asset” with its own legal attributes。

Periodic vs life: a table that understands how to choose (2026 edition)

Don't treat life-long risk as an all-powerful tool to avoid crime。

The proceeds of the offence are not taken into account: if the source of the premium is problematic (money-laundering, illegal collection of funds, etc.), the court can enforce the policy. The designated beneficiary must write: if the beneficiary is not designated, the settlement of the claim becomes a “inheritance”. This is a time not only for debt repayment but also for “directed inheritance” that you want. The increase in life expectancy has changed: in 2026, the mainstream “incremental life risk” not only kept alive, but also reduced off-the-shelf pensions and was much more mobile and safe than before. 6. Pipes for each of the two products

A smarter idea: to save “current responsibility” with periodic life insurance, and to save “money for the future” with lifetime risk。

One last word

Many people would say, "i buy life insurance to fight inflation."

The truth is that the traditional quota life insurance, which is fixed, will shrunk in decades. If you really have an inflation-resistant demand, pay attention to ** “additional life insurance”** — its insured and cash value increases by around 2. 0 per cent to 2. 5 per cent per year。

Remember one thing: money that can't grow up is often meaningless after decades。