Q: what tax policies are the main actors in individual home buyers

Response: 1. Taxes

The rate is 3 per cent。

The tax is reduced by 1. 5 per cent for the purchase of ordinary housing by individuals, which is the sole home of the family (including the purchaser, the spouse and the minor children, respectively). The tax is reduced by 1 per cent if an individual buys a general dwelling of 90 square metres or less, which is the only home for the family。

Stamp duty

From 1 november 2008, a stamp duty was temporarily waived on the purchase of housing by individuals。

The home title certificate is levied on the basis of a five-dollar permit。

3. Property tax

(1) the charge is made on 28 january 2011 in respect of new houses purchased by the families of residents of the municipality that belong to the latter's second home and above (including second-hand stock and new commodity housing, respectively) and new houses purchased by non-resident families of the municipality (hereinafter referred to as “taxable housing”). The purchase time for the new house is based on the date of the online filing of the purchase contract。

(2) in the case of newly acquired housing units of the municipality and belonging to the second and more dwellings of the residents, the total housing area of the combined household (i. E., the building area, the same size) does not exceed 60 square metres (i. E., the free-of-charge housing area, which covers 60 square metres), the property tax is temporarily waived; in the case of new housing units over 60 square metres per person, the property tax is calculated according to the rules。

(3) the property tax is temporarily calculated at 70 per cent of the market price of the taxable housing, and the applicable rate is tentatively 0. 6 per cent. The market transaction price per square metre of taxable housing is twice as high as the average sales price for new commercial housing in the last year of the city, and the tax rate is temporarily reduced to 0. 4 per cent。

Question: what tax policies are the main providers of individual housing

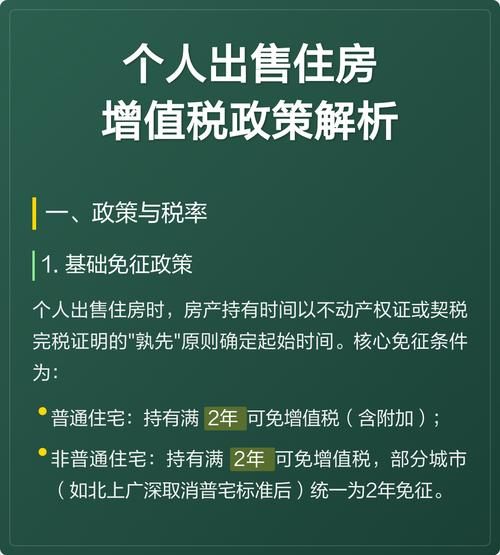

1. Business tax

Individuals who purchase housing for a period of less than five years will be subject to a full turnover tax; individuals who purchase non-ordinary housing for a period of more than five years (including five years) will be subject to a turnover tax based on the difference between their sales income and the price of the house purchased; and individuals who buy a general housing for a period of more than five years (including five years) will be exempt from the turnover tax。

The date of the individual purchase of the house is fixed on the basis of the first-in-first-in-first-in-first-in-first-in-first-in-first-in-first-in-first-out basis, with the date given on his/her home title certificate, the date indicated on the tax clearance certificate and the date on which he/she will complete the tax。

The established turnover tax is paid in addition to the established city construction tax (7 per cent, or 5 per cent, or 1 per cent), education surcharge (3 per cent), local education surcharge (2 per cent) and maintenance fees for the construction of riverways (1 per cent)。

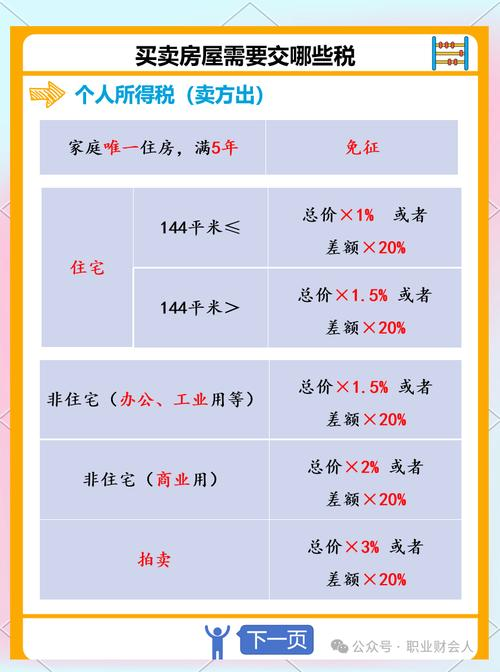

2. Personal income tax

(1) collection of personal income tax

Individual income tax is levied at a rate of 20 per cent on the sale of their own home, less their original value and reasonable expenses. If the taxpayer does not provide complete and accurate proof of the original value of the house and cannot correctly calculate the original value of the house and the amount due, the tax authorities may impose an authorized tax on it, i. E. The amount of personal income tax payable in proportion to the income transferred from the taxpayer's housing. The city has an approved rate of 1 per cent for general housing and 2 per cent for non-general housing。

(2) individual transfer of the family's sole living home

Persons are exempt from personal income tax for the transfer of income derived from their own use for more than five years and as the sole household dwelling。

3. Land value added tax

With effect from 1 november 2008, individuals were temporarily exempted from land value added tax on the sale of housing。

4. Stamp duty

From 1 november 2008, stamp duty was temporarily waived for the sale of housing by individuals。

Q: what are the criteria for distinguishing between general and non-general housing

As of 1 november 2008, general housing must meet the following conditions:

(a) multi-storey housing of five or more floors (including five floors), as well as old-style apartments of less than five floors, new-style inlays, old-style inlays etc.

2. A single building space of less than 140 m2

The real transaction price is less than 1. 4 times the average transaction price for housing on land of the same level, less than $2. 45 million/snap within the inner ring line, less than $1. 4 million/snap between the inner ring and the outer ring and less than 980,000/snap outside the outer ring line。