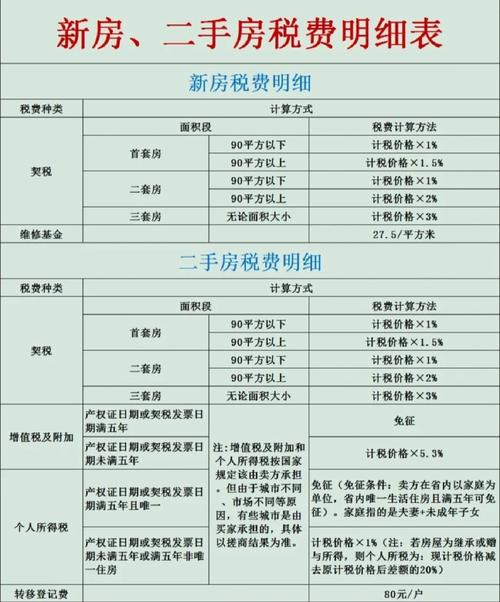

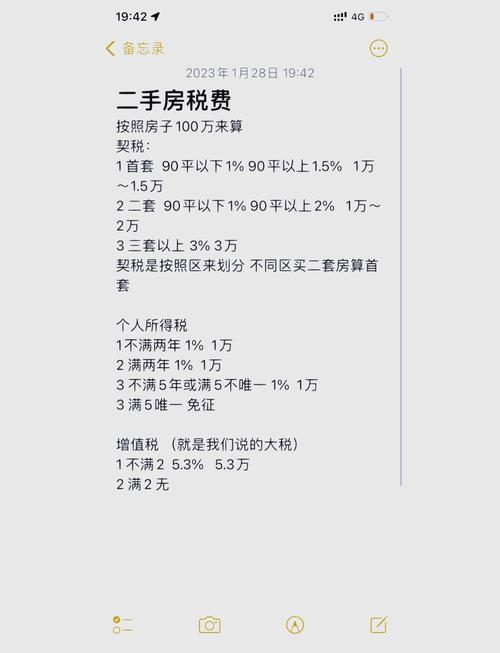

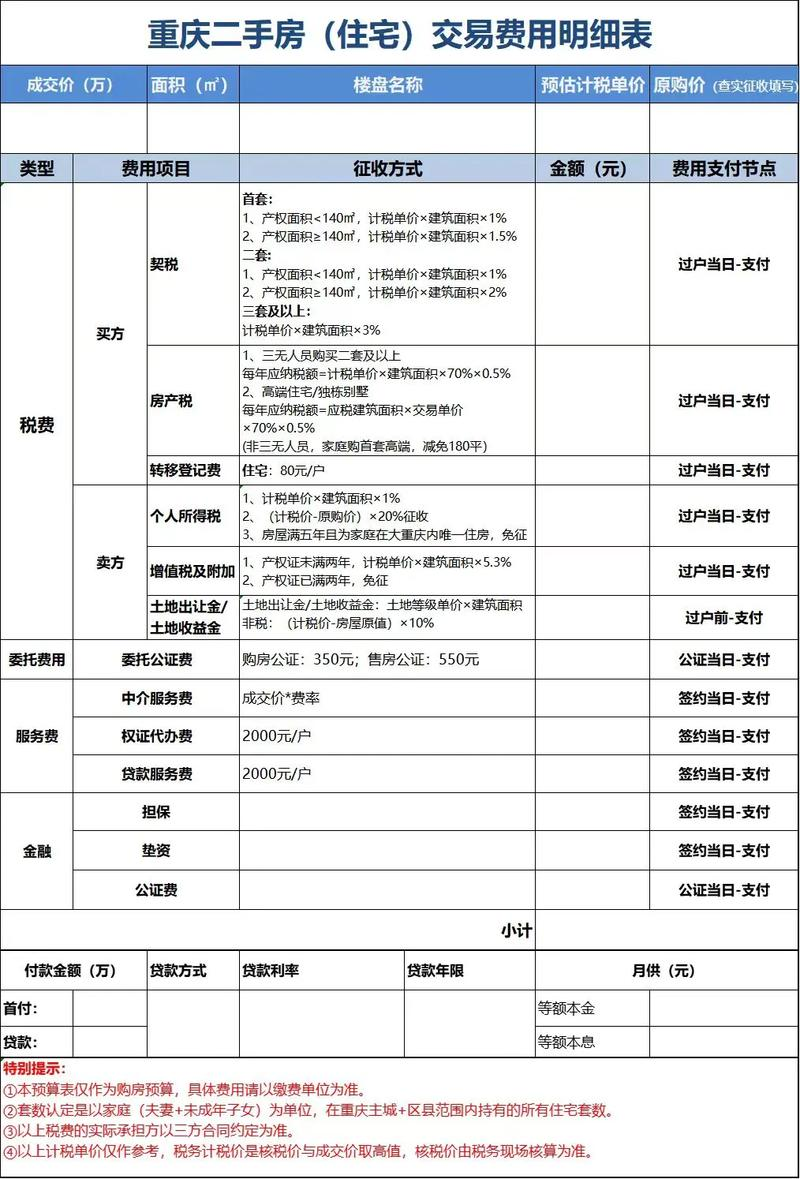

It is important to know how the relevant taxes and fees are calculated when buying used houses, which helps the buyer to budget the cost of the house accurately. The following is a detailed account of the taxes and fees that are common in second-hand house transactions and how they are calculated。

1. Taxes

The tax is a tax that must be paid for the purchase of a used house at a rate determined by the actual transaction price of the house. In general, the tax rate is between 1 and 3 per cent, depending on the size of the house and the number of purchases made by the buyer. For example, buyers of first-time homes may benefit from lower tax rates, while buyers of non-first-time houses may need to pay higher rates。

2. Personal income tax

If the seller holds the property for less than five years or is not the only dwelling, personal income tax may be required. Personal income tax is usually calculated on the basis of the added value of the house, at a rate of 20 per cent. The formula is: (a transfer price - a purchase price - a reasonable cost) x 20 per cent。

3. Value added taxes

In the case of non-ordinary dwellings (e. G. Commercial houses or high-end apartments), vat may be paid if the seller holds the property for less than two years. The vat rate is usually 5. 6 per cent and the base figure is the transfer price of the house。

4. Stamp duty

The stamp duty is another small levy on second-hand house transactions, usually 0. 05 per cent of the transaction price. The buyer and the seller share this tax。

5. Intermediary fees

Intermediary fees are also payable in cases of sale of houses through intermediaries. The rate of the intermediary fee is usually between 1 and 3 per cent of the transaction price of the house, which is determined by the intermediary and market conditions。

The following is a simple example of tariff calculation:

Example of method of calculation of tax type (assuming a value of $1 million)

Taxes

1 - 3% of the transaction price

1 million x 1. 5% = 15 000

Personal income tax

(transfer price - purchase price - reasonable cost) x 20%

(1 million - 800,000 - 20,000) x 20% = 36,000

Value added tax

5. 6% of the bargain price

1 million x 5. 6% = 56,000

Stamp tax

0. 05% of the deal price

1 million x 0. 05 per cent = 0. 05 million

Intermediary fees

1 - 3% of the transaction price

1 million x 2 per cent = 20,000

Through the above-mentioned forms, buyers are able to see clearly the method of calculation and the amount of each tax charge, thereby better planning the purchase budget. In practice, buyers and sellers are advised to consult in detail local tax authorities or professional tax consultants prior to the transaction to ensure that the calculation of taxes and fees is accurate。