The tax administration of guangzhou, the local municipalities, and the district of in-depth cooperation of yokohama are:

In order to do my work on housing rentals in the province, to promote the healthy development of the housing rental market and to ensure the accurate implementation of tax incentives, in accordance with the proclamation of the ministry of housing, urban and rural construction of the ministry of finance on tax policy for the improvement of housing rents (official gazette no. 24 of 2021 of the ministry of housing and urban and rural construction of the people's republic of china of the people's republic of china of the people's republic of china of the state tax administration) and the opinion of the office of the people's government of guangdong province on the implementation of the recommendation on accelerated development of secure rental housing (2021) in accordance with the relevant provisions, the provincial revenue service has prepared the operational guidelines for implementing housing rental policy, which are being issued to you。

State tax administration, guangdong province

26 april 2022

Operational guidelines for implementing housing rental policy

In order to do my work on housing rental in the province, to promote the healthy development of the housing rental market and to ensure the accurate implementation of tax incentives, in accordance with the proclamation of the ministry of housing, urban and rural construction of the ministry of finance of the people's republic of china on the tax policy for the improvement of housing rentals (official gazette of the ministry of housing and urban development of the people's republic of china no. 24 of 2021 of the state tax administration of the people's republic of china, hereinafter referred to as the proclamation) and the opinion of the office of the people's government of guangdong province on the implementation of measures to accelerate the development of secure rental housing (2021) 39), which sets out these guidelines。

Policy basis

(i) bulletin of the ministry of finance of the ministry of housing, urban and rural construction of the general directorate of taxation of the people's republic of china on tax policy for the improvement of housing leases (ministry of finance of the people's republic of china of the state tax administration of the people's republic of china of the ministry of housing and urban and rural construction of the people's republic of china of 2021)

(ii) opinions of the office of the people's government of guangdong province on the implementation of measures to accelerate the development of secure rental housing (2021) no. 39)

Scope of application

(i) the total rental income from vat to private or guaranteed rental housing in housing rental enterprises may be subject to a simple tax method, calculated at a rate of 5 per cent minus 1. 5 per cent, or vat based on a general tax method

(ii) value-added tax (vat) paid by small-scale taxpayers in housing rental enterprises to private or guaranteed rental housing, reduced by 1. 5 per cent at a rate of 5 per cent

(iii) the rental of personal or guaranteed rental housing by the housing rental enterprise shall be subject to the application of the above-mentioned simple tax method and to advance payment, less the advance value added tax at the rate of 1. 5 per cent。

The formula is as follows:

Tax reduction = tax inclusive sales ÷ (1+1. 5%) x (5-1. 5%)

Taxable = ÷ (1+1. 5%) x 1. 5%

(iv) real estate tax is reduced by 4 per cent for enterprises, social groups and other organizations that rent housing to individuals, specialized housing rental enterprises or secure rental housing。

The above-mentioned tenancy enterprises are those that report to or file with the urban and rural construction sector as required for the opening of a business。

The above-mentioned guaranteed rental housing refers to secure rental housing built on non-inhabited land and non-inhabited housing (including commercial office housing, housing rented for residential use after the conversion of industrial plants) and shall be certified as a guaranteed rental housing project. The certificate of the guaranteed rental housing project was issued by the relevant authorities of the municipal and district people's governments after a joint review of the construction programme。

The above-mentioned criteria for specialized-sized housing rental enterprises are: 1,000 units of rented housing and above, or 30,000 square metres and above, in the city where the establishment is reported or filed。

The above-mentioned individuals include individual traders and other individuals。

Iii. Policy access

Eligible taxpayers are entitled to tax incentives for housing rentals, which are processed by means of a “self-determination, declaration of entitlement, record-keeping of information” and are subject to a tax-exempt declaration in accordance with the relevant provisions of the present guidelines

(i) a lease contract evidencing ownership of the immovable property or evidencing the right to use the property

(ii) a certificate for a guaranteed rental housing project

(iii) tenancy contracts

(iv) other relevant information。

Iv. Vat and surcharge reduction filing process

(i) the taxpayer shall file for tax relief within the prescribed filing period。

(ii) the electronic taxation authority (vat general taxpayer):

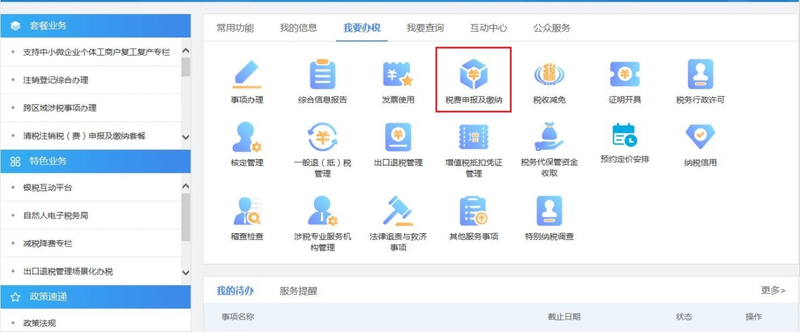

Access to the filing interface through the electronic taxation authority by clicking on “i'm going to tax” - “tax and payment” - “closure of declaration” - “scheduled declaration” and “vat and surcharge tax declaration forms (applicable to general taxpayers)”. (see figures 1 and 2)

Figure 1

Figure 2

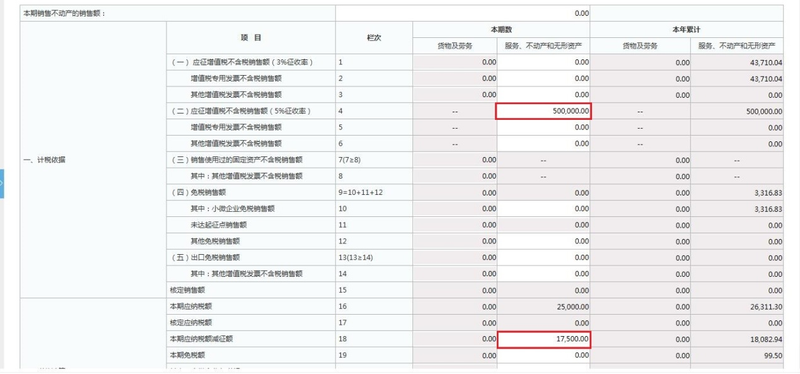

In processing the tax returns, the taxpayer fills out sales under “services, real estate and intangible assets at 5 per cent collection” (or “uninvoiced”) in “ii, summary tax collection” in the “vat and surcharge declaration form” (a breakdown of current period sales). (see figure 3)

Figure 3

Taxable deductions calculated at 3. 5 per cent of sales are taken into account in the “i, tax abatement item” - “code of nature of tax abatement” - “0001011707 |sxa0319012116|, applicable to housing rental enterprises, shall be reduced by 5 per cent to 1. 5 per cent of value added tax” and in the “vat and surcharge deductions” column. (see figure 4 and 5)

Figure 4

Figure 5

(iii) electronic tax authorities declare (small vat taxpayers):

Access to the filing interface through the electronic taxation authority by clicking on “i'm going to tax” - “tax and payment” - “closure of declarations” - “scheduled declaration” and “vat and surcharges” (applicable to small taxpayers). (see figures 6, 7)

Figure 6

Figure 7

For the current period, the amount of vat sales is reduced by 1. 5 per cent at the rate of 5 per cent and the “services, real estate, and intangible assets” is added to the “current number” of vat-exempt sales (5 per cent collection rate) in the “vat and surcharge tax declaration form (for small taxpayers). (see figure 8)

Figure 8

Taxable deductions calculated at 3. 5 per cent of sales will be taken into account in the “i, tax abatement item” - “code of nature and name of tax reduction” - “0001011707|sxa03190116|, applicable to housing rental enterprises, shall be reduced by 5 per cent to 1. 5 per cent of value added tax” and in the “vat and surcharge tax declaration (of small taxpayers)” column. (charts 9, 10)

Figure 9

Figure 10

V. Proceedings for distribution of housing

(i) the taxpayer shall file for tax relief within the prescribed filing period。

(ii) the electronic taxation authority declares:

Access to the e-tax office, click on “i'm going to tax” — “consolidated information report”, find “information report on property and behavioral tax sources”, click on “tax source collection” for property taxes, and enter the “tax collection” interface for urban land use taxes. (see figures 11, 12)

Figure 11

Figure 12

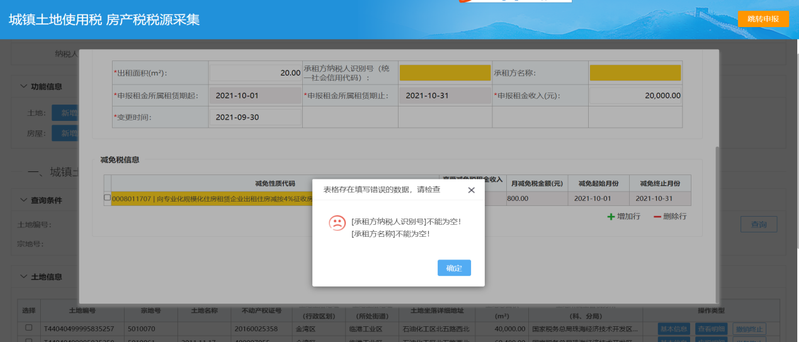

In the field of “specific sources of tax on property” the source of the house that requires the information to be collected for the relief is found, and information is maintained by clicking on “taxable details” and by clicking on “taxable information on the house (from rent)” to collect rental information. (see figures 13, 14)

Figure 13

Figure 14

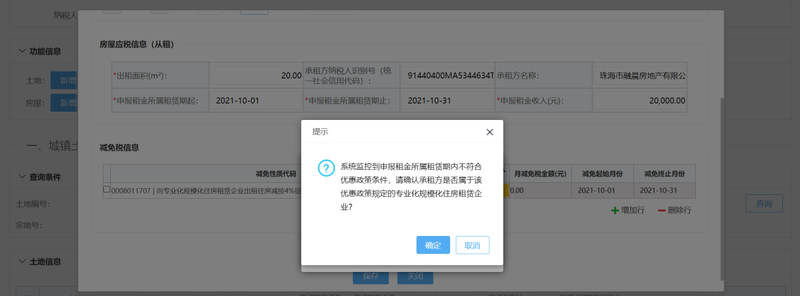

N. B. The lease information must be collected by filling in the lessee's information, otherwise the system will not be kept when the next step is chosen to apply the credit code, suggesting that “the lessee's taxpayer identification number cannot be empty and the name of the lessee cannot be empty”. (see figure 15)

Figure 15

Following the completion of the rental information collection, the corresponding relief code is selected from the drop-off box in the "code of the nature of the relief" column by clicking on "additional rows". (see annex 1, figure 16)

Figure 16

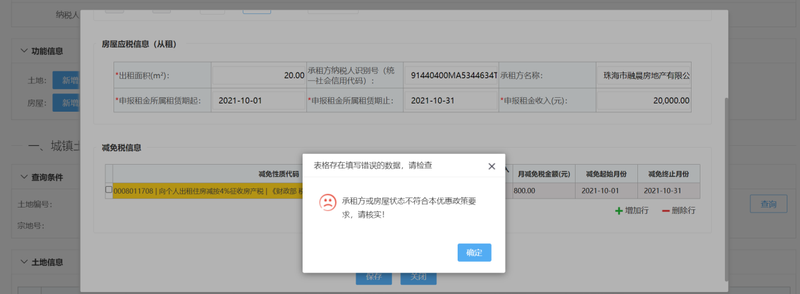

Note: to distinguish the precise statistical effects of relief, the system has four mitigation codes. The system verifies the relationship between the lessee's information, the use of the property and the code of the mitigating nature of the choice, does not match the match, and the system sends the wrong message. (see figure 17)

Figure 17

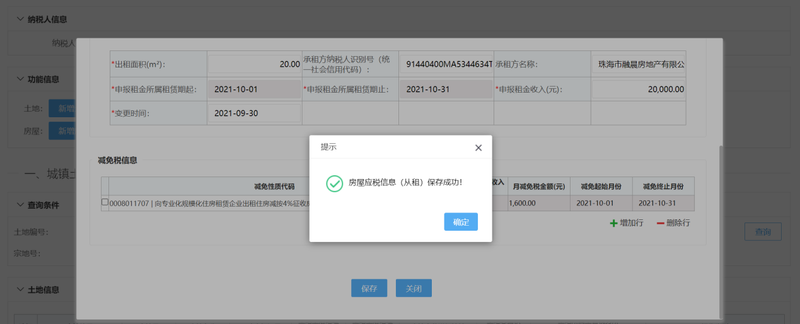

4. When the corresponding relief nature code is selected, the system displays the alert information according to the different relief nature codes. The system automatically brings “tax-exempt rental income” and “monthly tax-exempt amount” after the click has been determined. Among them, “tax-free rental income” supports manual modifications. (see figure 18)

Figure 18

Click save. System alert: “housing taxable information (from rent) is kept successfully!” (see figure 19)

Figure 19

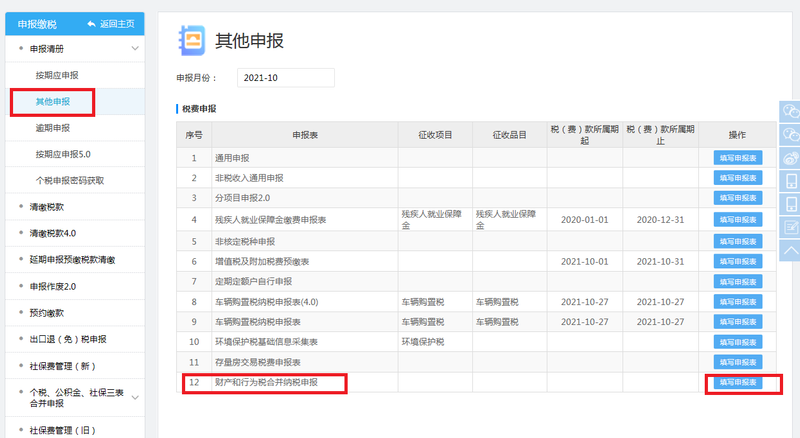

6. Property tax declaration. Clicking on “i want to collect taxes” – “tax and pay” – “other declare” — “consolidated declaration of property and conduct” — “to fill out declaration forms”, after entering the consolidated declaration form, choosing the period in which the tax is due, choosing the source of the undeclared property tax, and clicking on “next move” for the declaration. (see figures 20, 21)

Figure 20

Figure 21

Vi. Advocacy and mentoring materials

Question 22 on the tax incentives for rental housing (annex 2)

Annex 1. List of categories of lessees and uses of lessors ' properties

2. 22. Detailed information on the tax incentives for rental housing