Summary

Basel iii is in the countdown phase of domestic implementation. This paper explores new requirements for business risk management in commercial banks, such as basel iii, provides an analysis of the reform elements and progress in implementing the market risk management framework and the counterparty credit risk management framework, and makes recommendations on how commercial banks can effectively upgrade their financial market operations risk management based on regulatory compliance。

Keyword

Basel iii financial market operations risk management credit valuation adjustment

In february 2023, the bank of the people's republic of china, the bank of the bank, published the commercial bank's capital management scheme, hereinafter referred to as the consultation draft, which is open to public consultation. The revised commercial bank capital management scheme (hereinafter referred to as “the new regulations”) is to be implemented from 1 january 2024, which means that basel iii is in the countdown phase of domestic implementation。

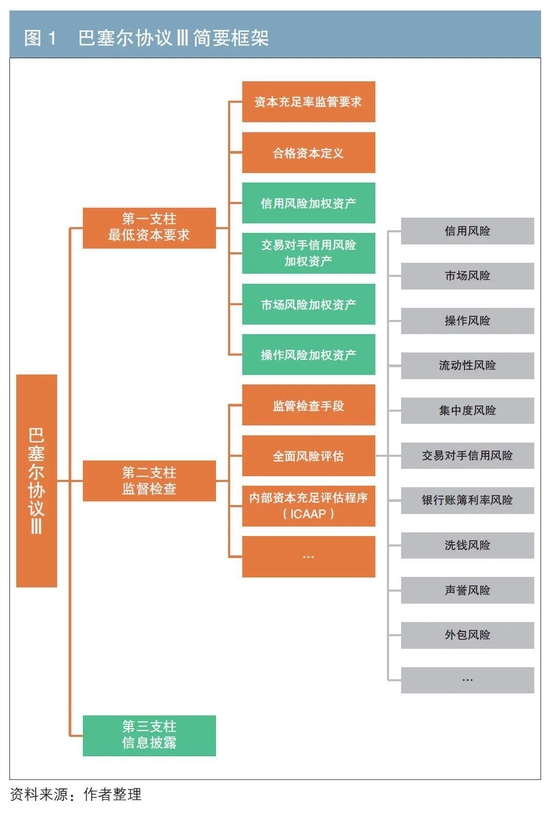

Following the 2008 international financial crisis, basel ii was widely stigmatized. The basel committee on banking supervision (bcbs) initiated reforms with the issuance in 2010 of the initial version of basel iii to raise the capital adequacy requirement for commercial banks, to strictly define the element of capital adequacy - qualified capital, and to increase the regulatory requirements for leverage and liquidity risk indicators. Since then, bcbs has issued a number of standard documents that have substantially revised the measurement rules for risk-weighted assets, the denominator of the capital adequacy rate. At present, the revision of basel iii has been largely completed and a large and rigorous regulatory system has been developed, with a brief framework as shown in figure 1. The green part of the figure is the main building block of basel iii reform after 2012 and the main thrust of this revision of the exposure draft。

The main types of risk for commercial bank financial market operations include market risk, counterparty credit risk, issuer credit risk, liquidity risk, operational risk, money-laundering risk and science and technology outsourcing risk. Financial market operations were the “severe-hit region” of the 2008 international financial crisis, thus becoming a focus area for basel iii reform. The authors will analyse market risk and counterparty credit risk management frameworks in the context of the focus of basel iii reforms after 2012。

Market risk management framework

(i) elements of reform

Among the basel iii modules, market risk management framework reforms were the most time-consuming and varied. There are a number of problems with the original framework, such as unclear book classification criteria, deficiencies in both methods of measuring market risk — insensitive standard methods, and inadequate coverage of internal model-based risks (royo et al., 2019). In 2019, after nearly 10 years of revision, the bcbs formally issued the minimum capital requirements for market risk, proposing specific solutions to past problems, including, inter alia, raising risk management implementation requirements, improving internal control mechanisms such as book segregation, trading desk management and information delivery and disclosure, requiring increased operational penetration and overall timeliness of data at the group level, and strengthening the central position of the standard approach, not only to harmonize regulatory scales, enhance comparability of risk indicators, but also to increase risk sensitivity, comprehensive and precise coverage of credit margin risk, default risk and residual risk; and enhancing the robustness of the internal model, replacing the risk value (var) model by using the expected tail loss model. In order to limit bank capital arbitrage through internal modelling, the new framework requires the trading counter to have independent accounting, a clear trading strategy and budgetary targets, and a sound risk management framework. The external market data used by the model should meet the requirements of dynamism and should not be treated with due diligence; the results of the model measurements would be subject to continuous return testing and loss attribution testing, compared with actual market changes, and those that did not pass the tests would be returned to standard methods。

(ii) progress in domestic implementation

In 2019, the bank formally launched the revision of the commercial bank capital management scheme (pilot) and conducted numerous policy briefings, revision studies and quantitative measurements in the industry. During this period, a number of large and medium-sized banks in the country also initiated implementation preparations. At the beginning of 2023, the implementation of the market risk measurement system for some banks was nearing completion. At this stage, domestic front banks are mainly using the new standard approach as a compliance programme, and new internal models are still being observed and studied. It is known to the authors that the implementation of the new internal model is more difficult and that, in addition to the considerable development resources required for system-building, there are other obstacles, such as difficulties in obtaining external market data that meet the new requirements, the difficulty of passing back tests and the fact that the management of the trading counter involves organizational restructuring. In addition, part of the domestic banking sector has a low share of financial market operations and the capital savings effect of implementing the new internal model is not evident。

Counterpart credit risk management framework

(i) overview of risk types

Counterpart credit risk is the risk that the institution entering into the financial contract will fail to meet its contractual obligations. This risk arises mainly from derivatives and securities finance (including buybacks and securities lending, etc.) and is generally referred to as “performance risk”. Counterpart credit risk can be broken down into default risk and cva risk. Among them, the cva risk refers to the risk of a trade loss due to a change in the credit position of the counterparty。

Unlike the general credit risk, the counterparty's credit risk is characterized by open orientation, uncertain opening size, and is more contagious and destructive (zongji, 2015). During the financial crisis, the default of a large number of complex derivatives triggered a market chain reaction, events such as the bankruptcy of the lehman brothers and the united states international group (aig) operation crisis, all closely linked to the cva risk of the counterparty。

(ii) elements of reform

In response to weaknesses in derivatives operations, in september 2009, the pittsburgh summit of the group of twenty (g20) launched a reform plan aimed at reducing systemic risks to derivatives, promoting the central liquidation of off-site derivatives through a central counterparty. In conjunction with this reform, on the one hand, in september 2013, the joint international organization of securities commissions (iosco) issued the guarantee requirements for the disaggregated settlement of derivatives, which require a step-by-step bond exchange based on the size of the institution's transaction in respect of derivatives settled by a non-central counterparty, while on the other hand, the bcbs continues to advance the reform of the framework for measuring the credit risk of the counterparty。

In march 2014, the bcbs issued the standard law on the measurement of credit exposures of counterpartants (hereinafter referred to as the “sa-ccr approach”), replacing the current risk exposure and standard approach under the basel ii framework, which is more relevant to the nature of the risk: the first is the recognition of risk hedging, measured separately according to the portfolio of eligible netting agreements and the combination of non-qualified netting agreements, and the classification of derivatives in the calculation of total additional risk exposures, taking into account possible offsets of risk exposures between positions; the second is the encouragement of the exchange of collateral and the design of different replacement cost measurement rules for the availability of qualifying bonds; and the third is the full consideration of stress scenarios, with the parameters of the sa-ccr methodology being carefully calibrated based on empirical data during the international financial crisis to fully capture fluctuations in market risk factors during stress periods。

In july 2020, the bcbs issued the final version of the credit valuation adjustment risk framework, which updates the market risk regulatory framework in tandem with the existing gaps. The first is to reduce reliance on external ratings, taking fully into account the impact of the trade of the counterparty, credit risk hedge instruments, etc. On risk levels; the second is to take into account the impact of market risk factors on the cva risk and increase risk sensitivity; and the third is to remodel the cva risk model and calibrate the corresponding parameters in the light of the latest market environment. The new framework includes the foundation and standard method, which measures cva based on market risk sensitivity indicators and requires a dedicated cva trading counter with higher implementation requirements; the foundation does not need to measure the corresponding risk sensitivity and is further divided into simplified and complete versions depending on whether credit risk hedges are considered。

(iii) progress in domestic implementation

In the area of risk exposure measurement, in january 2018, the former silver college introduced the rules for the measurement of the risk of default assets of counterpartants to derivative instruments. 1) the formal introduction of the sa-ccr method, which requires commercial banks with a nominal principal value of 500 billion yuan on derivatives or more than 30 per cent of total assets. The consultation draft did not significantly adjust the sa-ccr methodology. However, taking into account the regulatory requirements for enhanced derivative management in recent years, as well as the internal management needs of banks, some banks have optimized the credit risk measurement system for their trading counterparts in preparation for the implementation of basel iii, facilitating its interface with other measurement modules。

In cva measurement, the exposure draft does not introduce more complex standard methods, but only basic law rules. Currently, there are no cva trading counters in our commercial banks and the credit derivatives market is not sufficiently active to provide a qualified credit risk hedge tool. As a result, most banks are still targeting compliance at this stage of preparation with the simplified version of the basic law。

Issues of concern in the implementation of the new provisions

Basel iii's provisions on market risk and on counterparty credit risk place greater demands on the level of precision, quality of basic data, complexity of models and system function. Royo et al. (2019) analysed the difficulties in implementing the new regulations, including the high impact on venture capital, the need for clear book classification criteria, the pre- and back-office gain/loss ratio, the complexity of measuring and validating, and the difficulty of data governance and system development。

In response, the exposure draft adopted a differentiated regulatory concept, requiring only medium- and large-sized banks meeting certain standards to implement the new standard law on market risk and the sa-ccr approach for counterparty credit risk, with most small and medium-sized banks being able to measure using simplified methods to reduce their compliance costs. At the same time, market risk and counterparty credit risk capital are generally low in terms of capital adequacy disclosed by domestic banks, at a combined rate of 1 per cent to 2 per cent, and the implementation of the new regulations will not have a significant impact on the capital adequacy of domestic banks. However, as a very quantitative segment, the implementation of the new rules on market and counterparty credit risk remains difficult and requires significant human and resource investment. The following difficulties remain in the implementation process。

One is that implementation of the new standard law on market risk requires adequate modelling procedures. The market risk model includes both risk measurement models, such as the var model, the es model, and other types such as the valuation model of financial instruments and the market data construction support model. Among them, the valuation model for financial instruments includes a cash-flow model for the valuation of linear products, a black-schuls model for the valuation of options, etc. The market data tectonic support model includes a plug-in model for risk factor curves, curve tectonics, etc. While the new standard method of market risk does not use the var model, the es model, its sensitivity measurement still requires the application of the valuation model of financial instruments and the market data architecture support model. Thus, the new standard approach is essentially a quasi-model approach, and a robust model management system is the basis for accurately measuring capital requirements. Commercial banks implementing the new standard law need to be fully aware of the importance of model management and build scientific and rigorous model validation procedures。

Second is the significant increase in the importance of static data management. Following the implementation of the new regulations, in addition to external market data (including interest rates, exchange rates, commodity and stock prices, etc.), the measurement of capital will require the application of a large volume of static data (including industry types, ratings of issuers and counterparties of financial products, rating of bonds, priority levels, rating of securitized products, priority levels, lower asset types, location of shares, etc.). To ensure accuracy of measurement, commercial banks should build sound static data management platforms. A well-developed data cleansing, mapping and data integrity check mechanism should be built for measurement using external data sources. Where data are entered manually, complete entry processes and management specifications should be established to minimize operational risks and improve the accuracy and timeliness of data entry。

Thirdly, there are challenges to the management and application of information systems. At present, market risk measurement is carried out by large, medium-sized and large-scale external banking systems in the country, which are more difficult to implement and manage. In implementing the system, commercial banks should pay high attention to the accuracy and smoothness of the data interface between the risk measurement system and the business system and the downstream reporting system, and should conduct full testing and up-line exercises to ensure smooth operation of the whole-line system. Commercial banks should also ensure that human and resource resources are invested in day-to-day operations, that new systems are better understood, that systems are better controlled and that the frequency of production failures is reduced。

Thinking of further upgrading of bank management

As the preparations for the implementation of basel iii advance, in addition to completing the “necessary answer” of regulatory compliance, our banking industry should study in depth how basel iii can be used as an opportunity to effectively enhance the level of risk management in its financial markets. Here are some of the thoughts of the writer。

One is to optimize the system of risk preference indicators. According to the definition of the china banking association, the risk preference indicator refers to the level and nature of the risk that banks are willing to assume in pursuit of their own values, in accordance with the business development strategy and the expectations of stakeholders. The new standard approach to market risk is based on sensitivity indicators, which introduce a large number of risk factors and risk indicators, such as credit margin factors (cs01) and curvature, which further reinforce the relevance of risk indicators to capital indicators. Commercial banks can use this to optimize the risk preference indicator transfer system, from capital to business, to provide sound guidance on the organization of business structures and the development of business scales. Accordingly, commercial banks also need to set target thresholds that meet risk tolerance levels and invest reasonable resources in indicators monitoring, etc。

The second is effective monitoring to help single-client exposure. There is a degree of secrecy about the credit risk of the counterparty, which is given relatively low priority by domestic counterparts. In the case of the general back-to-back counter-consumer derivatives, price movements appear to have no impact on book profits, while the customer's performance risk exposure is embedded. In the event of large fluctuations in markets and delays in flatting, openings may expand rapidly and customers may refuse to meet their insurance obligations. Currently, the sa-ccr methodology has not been widely applied by national counterparts in areas such as internal derivative line management and quota control. In fact, the risk exposures calculated on the basis of the sa-ccr methodology are characterized by careful estimates, and the effects of surveillance are better than those of direct use of valuations and can serve as an improvement direction for open-access monitoring. At the same time, ad hoc stress tests could be conducted to inform the assessment of the ability of clients to absorb business losses under extreme conditions and to set up an overall prudent and differentiated bond collection programme。

Third, there is enhanced tracking and monitoring of business sector transaction strategies. The new basel iii provisions clarify the regulatory framework for the trading counter in a chapter form, which, while not required to meet standards at the level of implementation of the new standard law, could provide a useful basis for fine-tuning the management of the trading counter. Commercial banks can combo the strategic information of the trading counters, display the position, position and time series of changes in the structure of the front-office assets in visual graphics at the strategic, group and institutional levels, and monitor key indicators of the portfolio of assets to ensure that transaction execution is consistent with strategic objectives. Of course, the strategic tracking and monitoring involved prior, ongoing and ex post full business processes, with an incomplete focus at different stages, and faced many challenges, such as strategic tracking indicator selection, indicator threshold setting, strategic tracking and monitoring, and effective integration of results with the front desk review, which required further in-depth study。