Background to the implementation of basel iii

Basel iii is about to be implemented domestically, and commercial banking financial market operations face a new set of risk management challenges. The paper examines in depth the new requirements for commercial banks under the new regulations and provides a detailed analysis of the reform elements and progress in implementing the market risk management framework and the counterparty credit risk management framework. On this basis, the paper presents concrete proposals on how commercial banks can effectively upgrade the level of risk management in their financial markets while ensuring regulatory compliance。

History and evolution of the agreement

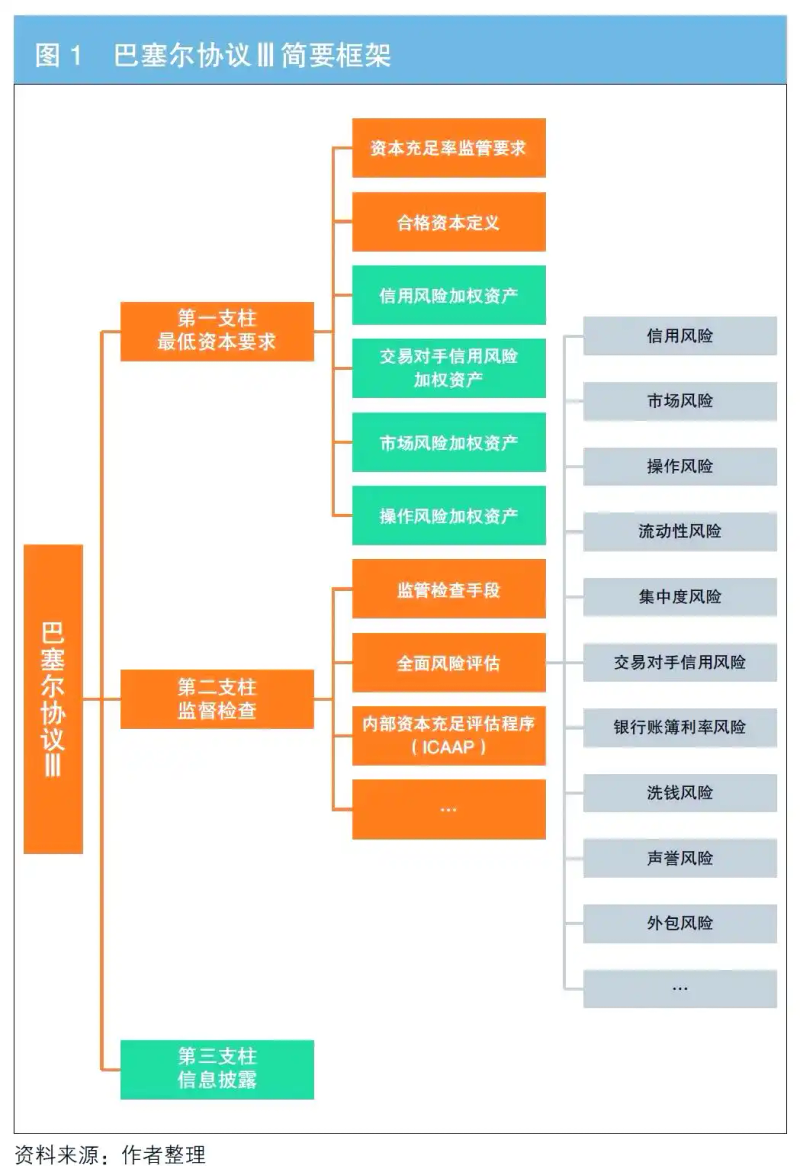

In february 2023, the bank issued the commercial bank capital management scheme (advisory draft), a new regulation that became operational on 1 january 2024, marking an already tense countdown in the domestic implementation of basel iii. Following the 2008 international financial crisis, basel ii was widely criticized for its shortcomings. To address this problem, the basel committee on banking supervision (bcbs) moved rapidly to reform and launched the initial version of basel iii in 2010. The reform aims to improve the capital adequacy standards of commercial banks, define qualified capital and strengthen the regulation of leverage and liquidity risk. Since then, bcbs has issued several standard documents that have significantly revised the measurement rules for risk-weighted assets. The revision of basel iii has now been largely completed and a comprehensive and rigorous regulatory system has been established. Its framework chart provides a clear picture of the main developments in basel iii reform since 2012, which are also at the heart of the revision of the present exposure draft。

Progress in domestic implementation

Commercial bank financial market operations face a wide range of risks, notably market risk and counterparty credit risk, which were exposed to the international financial crisis in 2008 and are therefore a key focus of basel iii reform. Domestic implementation of basel iii has progressed significantly, and the collaboration between the bank and the bank of the people's republic of china has marked the country's attention and positive preparations for this agreement。

01 reform of the risk management framework

Reform of the market risk management framework

In response to market risk, the bcbs modified the market risk management approach, in particular the reform of the market risk management framework, which was the longest-consuming and most varied of the basel iii modules. The lack of clarity and weaknesses in the original framework were revealed during the financial crisis, such as the vague book classification criteria and the inadequacy of both methods of measuring market risk. In response to these problems, after almost a decade of effort, the bcbs finally released the market risk minimum capital requirements in 2019, proposing concrete solutions. These programmes include, inter alia, upgrading risk management implementation requirements, improving internal control mechanisms such as book classification, trading desk management, and information delivery and disclosure; strengthening the centrality of standard law, harmonizing regulatory measures and increasing risk sensitivity; and enhancing the robustness of internal modeling, replacing the var risk value model with the expected tail loss (es) model to more accurately map tail risks。

Reform of the counterparty credit risk management framework

In the case of counterparty credit risk, the sa-ccr approach was introduced, improving the accuracy of risk measurement. Counterpart credit risk refers to the risk of failure by financial contracting institutions to fulfil their contractual obligations, arising mainly from derivatives and securities financing operations. This risk is often referred to as “performance risk” and can be further broken down into default risk and credit valuation adjustment (cva) risk. The cva risk is the risk of a transaction loss due to a deterioration in the credit position of the counterparty. Unlike general credit risk, counterparty credit risk is open, uncertain in orientation and size, and highly contagious. In the context of the financial crisis, defaults on complex derivatives triggered a chain reaction in markets, such as the bankruptcy of lehman brothers and the business crisis of the united states international group (aig), which were closely linked to the cva risk of the counterparty. In response to systemic risks in derivatives operations, the group of twenty (g-20) presented a reform plan at the pittsburgh summit in september 2009 aimed at reducing systemic risks in derivatives。

Domestic implementation challenges and recommendations

Implementation challenges

The new regulations are more demanding for managing the credit risk of the market and the counterparty, covering a number of aspects such as management precision, the quality of basic data, the complexity of models and systemic performance. In their analysis, scholars such as royo (2019) pointed out that the implementation of the new regulations faced many difficulties, including significant venture capital impact, unclear book classification criteria, back-to-back gains and losses over difficulties, complex measurement and validation, and challenges to data governance and system building。

Specific recommendations to enhance risk management

Improving the system of risk-based indicators, strengthening client exposure and transaction strategy controls and improving the overall risk-management capacity of banks. First, the system of risk preference indicators should be improved. According to the definition of the china banking association, the risk preference indicator is the level and nature of the risk that banks are willing to take in pursuit of value, based on business development strategies and stakeholder expectations. The new standard approach introduces risk factors and indicators such as credit margin factors, curvatures and strengthens the link between risk indicators and capital indicators。

Second, it strengthens single-client privy surveillance. The credit risk of the counterparty is potentially high and needs to be given greater attention by the domestic banking sector. For example, in the back-to-back counter derivative business, price changes on the subject, while not directly affecting book profits, exposed the customer to performance risk exposure。

Thirdly, the continuous tracking and monitoring of the business sector's trading strategy is enhanced. The new basel iii regulation details the regulatory framework for the trading counter in a specific form, which, although not a standard requirement of the new standard law, provides a useful reference for the fine-tuning of the management of the trading counter. Commercial banks can systematically combo the strategic information of the trading counters, display the position, position and structural changes of the front-office assets through visual graphics, and monitor key indicators of the portfolio of assets to ensure that transaction execution is consistent with established strategies. It is worth noting that strategic tracking and monitoring involve a whole process before, during and after events, with a different focus at all stages, and face challenges such as strategy tracking indicator selection, indicator threshold setting and how to effectively integrate tracking and monitoring results into the front desk examination, which require further in-depth study。