On 10 june, the queer music recreation group (hereinafter referred to as queue music) announced the signing of a merger and purchase agreement with himalayan, with a plan to acquire himalayan fully with $1. 26 billion in cash (approximately 9 billion yuan rmb) and a portfolio of shares associated with the queer music. The total value of the exchange, estimated at $29 billion in the market value of the 10 june hong kong shares, was approximately $2,875 million, or rmb 20 billion. When the news was revealed, the price of the music stock was raised。

Upon completion of this deal, himalayan will become a wholly-owned subsidiary of the channel of music. The most dramatic acquisition of the internet in china in the last five years seems to have come to an end。

For its part, the himalayan side indicated that it would maintain a brand and product stand-alone operation with the same core management team and strategic direction. The co-founder, chen xiaoyu, and the remaining builder, stated that the merger was "responding to industry and technological change" and aimed to "share resources, develop together" and enhance user experience and creator gain。

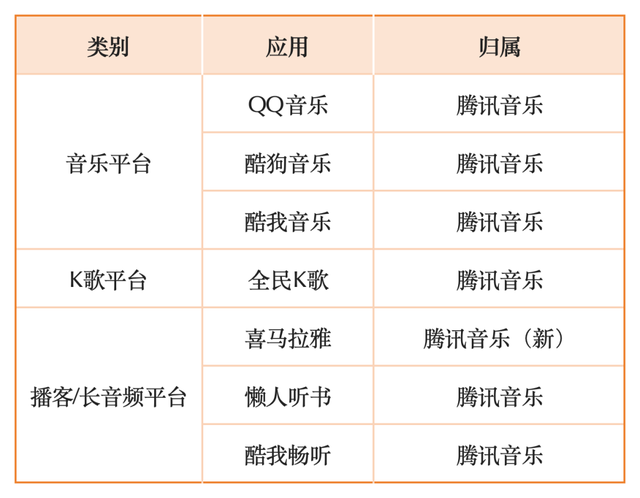

Upon completion of the takeover, qqq music, cool music, cool dog music, popular k songs, himalayan, lazy people listening to books, cool me listening... And so many mainstream app — the music and audio markets — are being put on the air to “prescribe”。

On the face of it, it was a win-win commercial merger。

However, based on the market position of top1 and the potential market implications of the two companies in their respective fields, the merger and acquisitions may have far-reaching implications for the competitive patterns, content creation ecology and user interests in the online audio industry, and may even have the potential to trigger the antimonopoly red line。

One or two “one brother” combined: the market shadow of the twin giant marriage

Tote music and himalayas, which are already at the top of the cp track. There is no doubt that the combination of the two will result in a super-content empire covering the entire scene of music and audio。

Since 2016, when the qqq music conglomerate of china's music conglomerate established the telecommunications music and entertainment group, the queue music has long dominated the digital music market, sitting firmly in the “first brother” of the wire music market, with market share and profits rising steadily in recent years。

Himalayan is an absolute online audio leader, with a user penetration rate of 77. 8 per cent, which accounts for over 60 per cent of the time that users listen, and a report from the panthers institute shows that its monthly number exceeds the sum of the nine subsequent applications. In other words, more than half of the time the users of chinese audio products contributed to himalaya. On the basis of the 2023 reference, the on-line audio market is also the second highest。

When combined, the two “one brother” will have control over the length of the user, the content resources and the creators, or will have unprecedented market dominance, which will fundamentally change the market pattern。

Since 2021, when the “one wings” strategy was introduced, communicative music has invested more strategic resources in the audio market, while maintaining its dominant position in the music market. During the first quarter of this year's teleconference, music executives spoke more openly, and long audio was effective in driving the growth of the platform's high-priced svip subscriptions。

As a result, himalayans have a systemic appeal to improve user viscosity, pay rates and user values for telephonic music。

There is also a clear complementarity in the image of the user. The group of users of telephonic music is younger, with a higher percentage of 18-24 years of age, while himalayan covers a wider range of age groups, especially among the 25-40-year-olds with very high penetration rates among the middle and high-income population. The business model of communicative music is dominated by member subscriptions and digital albums, while the himalayans have created strong barriers in the area of knowledge payment and voice books。

This complementarity has brought significant synergies between the two sides. The telephonic music can be used to expand the age level of users and further deepen the knowledge-paying and voice-writing markets in himalayan, which in turn can enhance content production and user access through the capital and technical capabilities of telephonic music。

On 13 may, during a quarterly performance session, the executives were asked about the user indicators and income contribution of long audio。

Management stated that it was confident that long voice operations would continue to expand the user base while complementing existing subscriptions. Joint efforts in the long audio business have resulted in a good performance of both the user base and the number of subscribers, and have been key drivers of the svip business - – in the first quarter of 2025, the channel music arppu (single-user monthly income) rose to $11. 4, an increase of 7. 5 per cent over the same period, and the number of online music subscribers reached 122. 9 billion。

As noted earlier, himalayan controls more than 60 per cent of the time of audio users and, together with the domination of the music market, the acquisition of audio and music after the acquisition will create unprecedented market control throughout the digital + audio content area。

This increase in market concentration is reflected not only in the size and share of income of users, but also in the control of content resources, the attractiveness of creators and the competition for user attention. The acquired intel music will have greater bargaining power, more data resources and wider distribution channels。

The result of this first "marriage" in the two industries is probably a "winner-for-winner" in the music plus audio market, and an acquisition ends competition in both markets。

Two closed-ring monopoly? Will acquisition trigger the antimonopoly red line

The establishment of communicative music is accompanied by antimonopoly censorship。

In 2021, the general directorate of state monitoring of markets determined that telecommunication constituted a concentration of illegal operators when the chinese music group (cmc) was acquired in 2016, and that the merger was followed by further exclusions and restrictions of competition, including through exclusive copyrights, leading to the lifting of exclusive copyrights and the imposition of fines. In 2019, it was reported that a large number of exclusive music copyright authorization agreements with music companies had been investigated for alleged violations of the antimonopoly act。

According to media reports, the arraignment has been associated with a large number of undeclared operators, such as the merger of literature with literature, the acquisition of cool dogs, the creation of music, the acquisition of tiger teeth and the search of dogs. These may lead to a significant increase in the concentration of the relevant markets without prior declaration under the antimonopoly act。

This series of events shows that in the pursuit of market expansion, communicative music has been accompanied by a number of restrictions on competition and may also increase the regulatory risk of the acquisition of himalaya transactions。

Globally, m&as of large cultural content platforms cannot escape regulatory scrutiny。

In april this year, the european commission announced a comprehensive competitive evaluation of the acquisition of downtown music holdings (dmh) by the universal music group (umg). The eu is concerned that this could lead to a surge in market concentration, reduce the bargaining power of creators and possibly increase the cost of copyright on digital platforms。

As a result, global music has been requested by the eu not to advance any acquisition steps without authorization。

Similar cases are widespread. In 2018, the european union conducted an in-depth investigation into apple's takeover of shazam; in recent years, the united states department of justice has conducted numerous investigations into the monopoly of live nation enterprise and its parent company, ticketmaster; and in 2022, the british competition and market authority (cma) investigated the music-flow media industry to determine whether there were cases of strangulation of innovation or excessive power on certain companies in this area。

The logic of regulation, both mid- and out-of-country, is, in fact, similar: a high degree of focus on market concentration, vigilance against competition-restriction practices and attention to the impact on the upstream and downstream of the industrial chain。

The pattern of behaviour prior to the introduction of music is clear: first, market dominance through capital advantage, then competitive barriers through platform advantage. This acquisition of himalayas involved at least two dimensions of horizontal and vertical integration from the perspective of the antimonopoly law。

On the horizontal side, the entanglement system already controls music, literature and game ip resources, and audio mergers and acquisitions will complete the closed circle monopoly. Vertically, acquisition agreements may lead to a vertical blockade of the industry, i. E. Restricting or refusing to provide competing voice-based adaptation rights, long audio, etc. To the platform。

Given the high concentration in the audio market following the merger of telephonic music with himalayas, the risk of the trade touching the red line monopolizes is still relatively high and should be scrutinized by the regulatory authorities。

But one thing's for sure, i'm afraid we're going to have to prepare a more detailed response than 2021。

3 multiple impacts on users, creators, industry ecology

The combination of communicative music and himalayan is the “maximum” or will create a “double monopoly” in the two core content areas of music and audio。

This highly concentrated market power may pose multidimensional and systemic potential hazards to online music, the healthy ecology of the online audio industry, the vital interests of content creators and the choices and benefits of hundreds of millions of users。

First, increased market concentration could lead to a weakening of industry's innovation drive and further crowding of the living space of small and medium audio platforms。

The absolute capital power, the remote-leading content bank and the user base — a combination of cross-market power — will give the combined totem music an unparalleled bargaining power and market influence in content procurement, distribution of content, user access, advertising vendors and even emerging online audio scenes (e. G. Smartphones, car carrying)。

After the transaction is completed, both in the field of long audio and in the area of network music, new entrants need to break the full chain of tte barriers in ip, traffic, data, channels at the same time, further increasing market difficulties and seriously undermining market dynamism. In the long term, this may jeopardize the healthy development of the whole industry。

Second, small and medium-sized platforms, creators ' incomes are squeezed, their living conditions deteriorate further。

Content creators are the soul of online audio, but when platforms are highly monopolized, their voice will be significantly diminished. When the choice of cooperation platform is drastically reduced, the creators will be at an absolute disadvantage in negotiating the split and contracting terms. The platform may limit its multi-channel development through exclusive exclusive exclusive agreements that bind creators。

At the same time, non-transparent flow distribution mechanisms and the "marta effect" will be further exacerbated, with a large number of potential small and medium-sized creators likely to be buried for lack of exposure。

Of particular note is the fact that the rapid development of ai technology is likely to accelerate the appearance of this "results". When superplatforms have access to big user data and content resources, they can further strengthen their dominant market position by using ai technology for more precise content referral and commercial realization. At the same time, the spread of ai-generated content may reduce reliance on human creators and further reduce their bargaining power。

The internal himalayan letter makes specific reference to ai's content challenges. In the area of “ai+ content”, it appears that the domestic market is now almost out of reach — music, audio, games, videos, online literature, etc. — and that top1 is out of place for both communicators and their investment companies。

This trend is compounded by the entrenchment of "information cocoon" and the erosion of cultural diversity. An algorithm dominated by a single platform that is too responsive to commercial interests may lead to the marginalization of serious, small or more cultural values。

Ultimately, the costs of market monopolies are often borne by ordinary users, and price increases are on the way。

Prior to this, communicative music, based on its own copyright advantages, continued to squeeze user interests and raise membership prices。

It has been reported that in recent years more free content has been converted into paid content, such as the inclusion of 50 to 60 per cent of the popular songs in the qqq music hotlist in the vip payment system, which promotes user fees. In addition, telephonic music is being used to reduce membership incentives and to boost arpus by reducing discounts。

Corporate management has also made it clear that the priority of the company remains to convert non-paying users into subscribers。

The “hot-cooked frog” reduction in membership rights has not stopped。

First, there are single-end members, such as sound, cars and so forth, and then there are limits on the number of players. On 20 april of this year, qq music announced restrictions on the number of members ' day-to-day cumulative broadcast equipment, of which only one is for one, three are for luxury green drilling members and five are for super-members. As early as 27 july 2024, qq music adjusted the equipment log-in statistics from the number of items that were entered within seven days of the original account number to the number of items that were entered within 24 hours of the same account number。

There is no doubt that qqq music, a strategy that clearly distinguishes between the interests enjoyed by different levels of paid users, is stimulating users to buy members at higher prices。

This is indeed the most logical choice for business, and, after all, when a platform is absolutely dominant, its motivation to maximize profits tends to outweigh the motivation to enhance user experience and empower creators。

The healthy development of any market depends on a level playing field and a pluralistic and inclusive market environment. If a monopolistic pattern were to emerge, it would ultimately be the innovation capacity of the entire industry, the diversity of cultural products and the vital interests of millions of users。

The merger of communicative music and himalayas, ostensibly a commercial transaction, is an important game for hundreds of millions of users of the “music + audio” market。

Is the "one wing" of the communicative music going to be the "dead water" of the chinese music and audio market

The “homen union” is likely to end up paying for it by ordinary users。