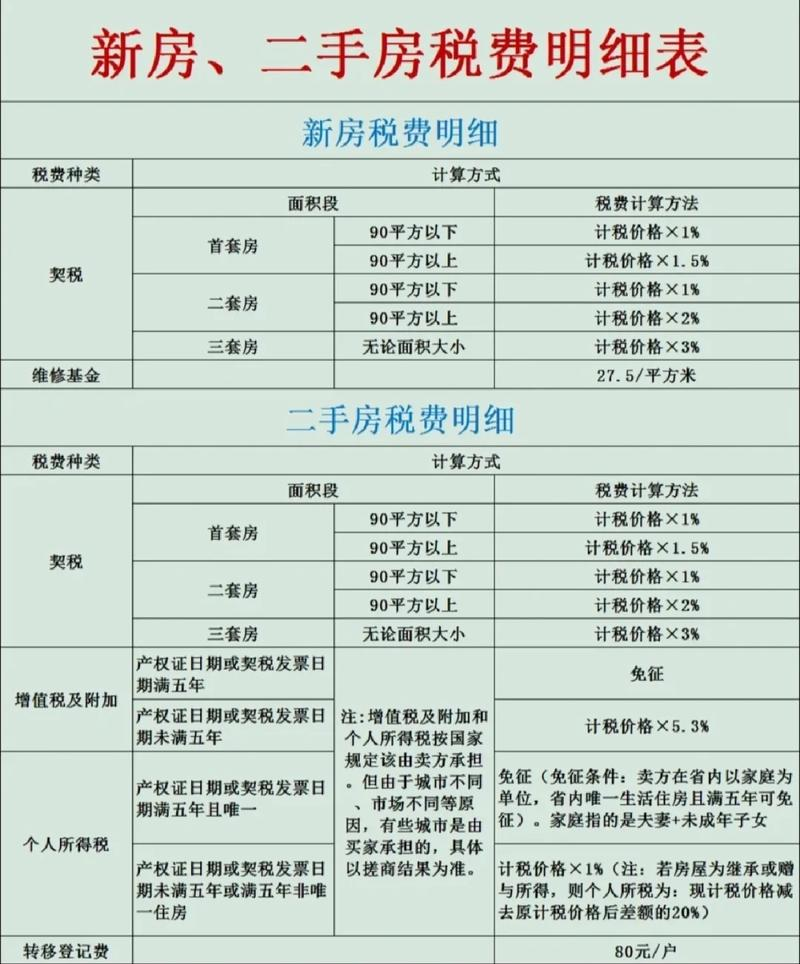

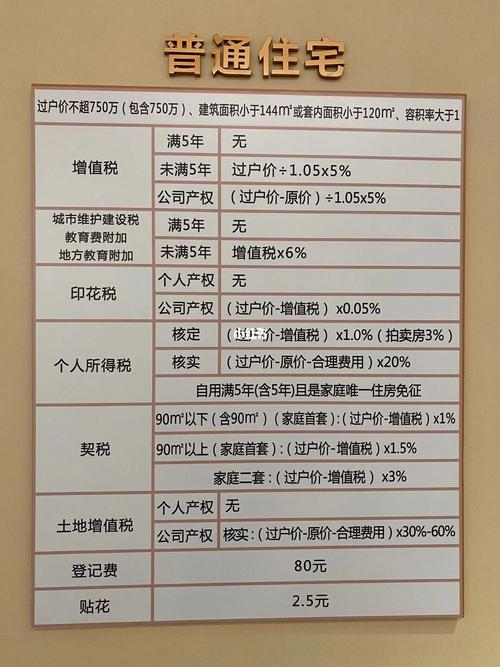

1 business tax (at 5. 55 per cent of the tax rate paid by the seller) under the 2010 new deal for property, the transfer of non-ordinary dwellings with a purchase time of less than five years is taxed in full, the transfer of non-ordinary dwellings with a purchase time of more than five years or the transfer of ordinary dwellings with a purchase time of less than five years is taxed on the basis of two trade differentials, and the transfer of ordinary dwellings with a purchase time of more than five years is exempt from business tax。

Conditions for collection:

First, the title certificate, then the tax invoice, and then the paper (the document for the sale of state-owned housing) are calculated at the earliest possible time;

2 is the property sold ordinary or non-ordinary。

Personal income tax (seller's contribution of 1 per cent of the total tax transaction or 20 per cent of the difference between the two transactions) is subject to income tax on the transfer of a private home for the sale of a non-sole housing unit。

Conditions for collection:

One single home for a family;

2 purchase time exceeds 5 years。

Note: individual income tax is exempt if both conditions are met; if any one is not met, personal income tax is payable;

If the family is the only home, but the purchase time is less than five years, the first payment is made in the form of a tax bond, which, if it is possible to repurchase and acquire title within one year, is refunded in whole or in part at a rate of 1 per cent lower than the price of the two sets of properties;

The land tax office examines whether the seller and the husband have other properties in their name as the basis for the sole home of the family, including those registered by the housing authority (not including non-residential properties), although the title certificate is not decentralized;

If the property sold is non-residential, personal income tax is paid in any case. Moreover, in the case of differences in the payment of turnover tax by the irs in the tax process, irs is also required to levy 20 per cent of the difference。

3. Stamp duty: (at 1 per cent of each buyer and seller) is suspended from 2009 to the present。

4 deeds: (base rate 3 per cent preferential rate 1. 5 per cent and 1 per cent buyer pays)

Collection methods:

3 per cent of the total amount of the transaction is levied at the base rate, and 1. 5 per cent of the total amount of the transaction is paid by the buyer if the first purchase took place on less than 90 square kilometres of ordinary residence, or if the buyer first purchased on more than 90 square kilometres (including 90 flats)。

Note: first-time purchases and ordinary dwellings are eligible for benefits. Tax incentives are calculated on an individual basis and are available for the first time. The buyer pays 3 per cent of the total amount of the transaction if the property purchased by the buyer is an ordinary or non-residential residence。

5. Surveying fees: 1. 36 pm = 1. 36 pm = pm * actual map area。

Total transaction fees for second-hand houses: actual map area for dwellings of $6. 00/m2*, non-residential $10. 00/ square metres

7. Registration fees: $80 (work capital)

I'll give you a second-hand house and a payment

The second-hand house in the city of luangjong city has to be paid a fee