Buying a car is a pleasure, but for many consumers, the experience of lending to buy a car has become a nightmare. The issues that are reflected in the concentration of consumers include the fact that the interest rate of the verbal promise for sale is far from the actual implementation, that the various fees are buried in the contract, and that the deposit is paid but not returned. How much is that

Case i:

5% annual interest, 9. 8% bank first instance

Last august, the consumer liu yang-sang received an extra ride model. The sales consultant provided him with a detailed description of the loan programme: 5 per cent per annum, a principal-equity repayment, and a subsidy of $8,000 from the factory if it were to be settled once in two years without extra default。

Yoo yang sounds good. He's got a $5,999 deposit to lock the car down. He found that the interest rate was 9. 8 per cent, almost twice as much as he had said。

Instead of providing a reasonable explanation, liu yang sought to “sign the car and then deal with it”. Liu yang quit and expressly refused to make a loan at this rate and then contacted the company's client service to return the down payment. The respondent, however, replied that “the order is locked and the refund cannot be processed”。

According to liu yang, the reason for his willingness to pay was based solely on the terms of the loan as described in the sale. Now that the conditions have changed, the basis of the transaction does not exist

Case ii:

Buy 150,000 cars and carry 200,000 in debt

Another consumer, li jun, suffered even more. He was looking at a $150,000 sedan that was not well-funded, and the sales company offered him a zero down payment split. - it's $4,500 a month, three years, and no mortgage。

Lee jun found the threshold low and signed several documents with great joy. But just after the first payment, the call came. He was told that the principal amount of the loan was not 150,000 yuan, but 200,000 yuan, and that the additional 50,000 was for various purposes of “services” and “guarantees”. The monthly contribution is not 4,500 yuan, but 6,000 yuan, and is subject to a daily fine of 1 per cent of the principal。

Lee jun looked closely at the contract, noting that there were some areas that were blank and are now covered by various fee clauses. Even more alarming is the fact that the lending company is not a formal financial institution at all and does not even have a licence to operate。

Case iii:

I forgot to pay back for two days. The car was driven away

Consumer wang dong wanted to buy a new energy truck but the bank loan was not available due to several credit card delays. The staff at 4s gave him the idea of going “to rent” and “to spend $3,000 a month for three years renting the car when it is due, which is yours。

When the contract was signed, wang dong realized it wasn't that simple. In addition to monthly payments, an additional $500 per month for “management fees” and “insurance premiums” is required. The contract also states that once the car is overdue, the owner has the right to take it away。

In one instance, wang dong neglected and paid off two days later, as a result of which the car was towed from the district. You want a car? Fine. It was only then that wang dong realized that the contract he had signed was a clause against him。

Case iv:

The interest rate is $6,000. It's $14,000 a year

Zhang li bought a car in a local 4s store this year. According to the sales version, the down payment of less than $150,000, the loan of $130,000, a five-year payment and an early settlement within two years, would amount to $67,000 in interest, at a monthly rate of $2,700。

As a result, when the first monthly bill came out, zhang was stupid: the actual monthly contribution was close to $2830, with interest at 1180 and principal at 1,600. That would cost more than 14,000 per year, almost 30,000 in two years, which is exactly the same thing。

Zhang li also found the amount of the loan in the contract to be $140,000, 10,000 more than it actually was. In order to pay back in advance, the financial company offered a price of $156,000, including 10,000 that had already been repaid for four months, which could never be matched。

Set the road down:

These tricks are for people who aren't careful

A combination of complaints by journalists reveals that the consumption trap in the area of automobile finance can be broadly summarized in the following categories:

The first one: it's low on the mouth, it changes on the paper

This is the most focused issue of complaints. When the sale presented the interest rate as low, and when the consumer made a down payment and even signed a contract, it found that the actual number was much higher. There are also sales that throw out concepts such as an “annualized rate” of “consolidated rates”, which ordinary people simply cannot calculate how much they actually pay。

Second: the contract is white and the knife is later

Some unregulated distributors or intermediaries would allow consumers to sign incomplete agreements and vow to “fill the blanks back”. As a result, the blanks were filled with famous costs. When consumers find out that they want to defend their rights, there is no evidence。

Third: leases disguised as loans

The “super-low interest” programme currently being promoted by some of the market operators is in fact a financial lease route rather than a bank loan. The central difference between the two is the attribution of the vehicle: bank loans to buy the car, which are registered under the buyer's name and can be released upon payment; and financial leases, where the ownership of the vehicle is in the hands of the leasing company throughout the lease period and consumers have only the right to use it. If there is a problem with repayment, the other party may take the car and the buyer may lose the money。

Moreover, rental programmes typically bind additional expenditures such as gps service charges, platform management fees and designated insurance, all of which may add up to much higher annualized costs than promotional figures. In order to be cleared ahead of schedule, it is often subject to a substantial fee。

Number four: format clause carding

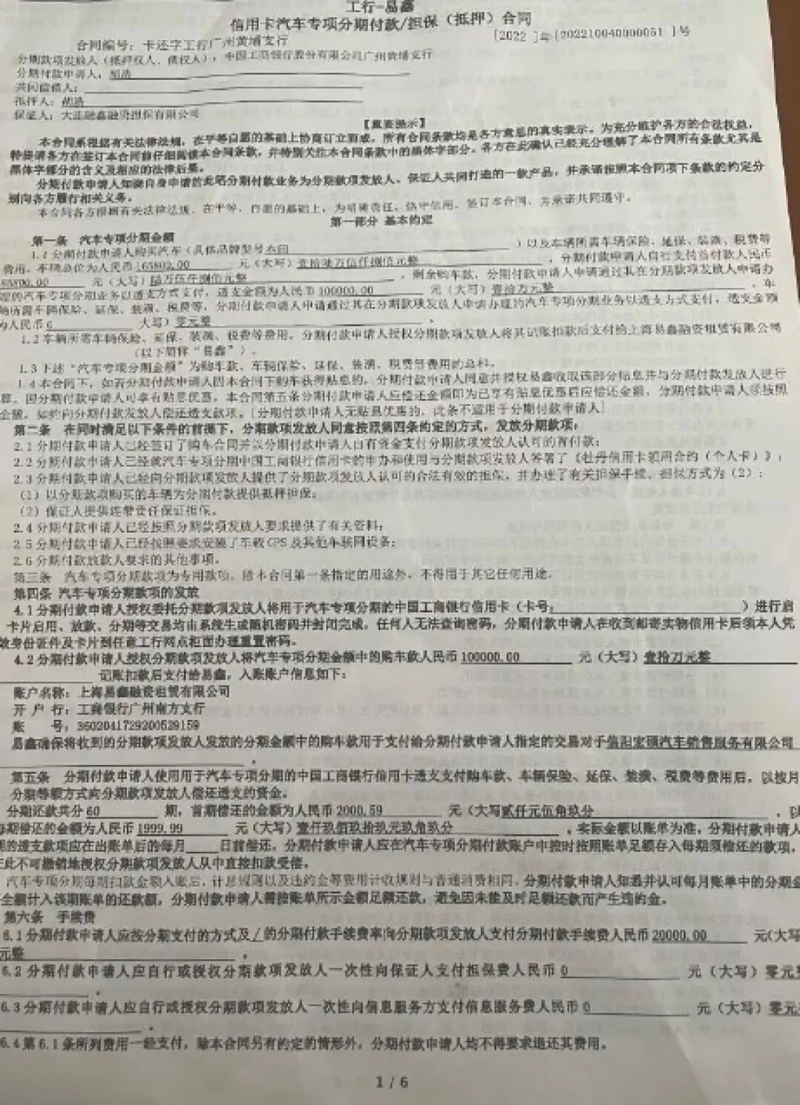

“as long as the loan approval has not been granted, the down payment has not been refunded” “a day after the expiration of the contract” “a substantial amount of compensation shall be paid in advance” ... These clearly market-oriented clauses are found in many car financial contracts. The text of the contract is numbered on dozens of pages, and there are a number of specialized terms, making it difficult for ordinary consumers to read every article before signing。

According to counsel:

False promises may touch fraud. Line

The analysis of lawyers from henan chun-joon law office shows that there has been a significant increase in recent car loan disputes for a number of reasons. The competitive nature of the car market and the shrinking of the margin of profit for distributors have given rise to the idea of “recovering” financial services; at the same time, brands have launched “zero-interest” marketing slogans to compete for sales at “super-low-interest” prices, but the implementation has been carried out in a way that allows consumers to fall into it without paying attention。

Counsel points out that, from a legal point of view, if the seller, at the time of marketing, attracts the customer to order at a significantly lower interest rate than the actual one, and subsequently to charge high fees under various titles, this practice is already suspected of constituting a civil law fraud and the parties bear the corresponding legal consequences。

Counsel has made a number of practical suggestions as to how to avoid pitfalls: do not rush to sign the contract after it has been received, every article must go through it, and where it is vaguely stated, it must be made clear on the spot; the matter of verbal consent by the salesman must be implemented in a written supplementary agreement; and the consumer has the right to claim null and void if a manifestly unfair form clause is found in the contract。

Counsel also emphasizes that such advocacy must take time and must take action within one year from the day when it becomes known that its rights have been violated, otherwise the statute of limitations for legal protection may be missed. Consumers are advised to keep the materials such as posters, chats, audio calls, original contracts, payment vouchers, etc. At first sight, and then to file complaints through the 12315 hotline, consumer associations or market regulators, in serious cases, or directly in court。

The industry reminds:

Formal channels are guaranteed and blank contracts are not touched

A senior car financier told journalists that the first choice was a bank or a car finance company with an official licence to buy a car. Such institutions are strictly regulated by the regulatory authorities and the products are relatively transparent. To check whether an institution is qualified, it can be verified on the official website of the financial supervisory authority. The risk is often higher for loan products that are tied to small sales companies or intermediaries。

It was also mentioned that publicity such as the “zero down payment” “super low” should not get hot. Under normal circumstances, bank loans for car down payment are at least 20 per cent, and programmes below this rate are likely to find money elsewhere. Prior to signing the contract, the principal, interest rates, monthly contributions and additional costs must be calculated and accounted for。

Another iron law is: never sign a contract with blank content. Some sales would say, “these columns will be filled later”, and never. All provisions must be completed on the spot and rechecked to confirm that there are no problems in order to fail. This is the most important evidence in the event of a later dispute。

If consumers choose a financial lease, it is important to understand the nature of the difference between them and ordinary loans. The vehicles were not owned by themselves during the lease period, and in the event of default the consequences could be much more serious than the overdue loan. The contract is signed with a focus on a number of issues: what exactly is included in the monthly supply, how will the default be handled, when ownership of the vehicle can be transferred, and what conditions will be met for early settlement. At the same time, as far as possible, larger and better-known leasing companies are selected, away from small institutions with questionable qualifications。

Cars are bulk consumer goods, and car-purchase loans are supposed to be convenient initiatives. In the face of a tumultuous financial programme, consumers need to be more rational and cautious in order to understand the terms of the contract in order to make their wallet less vulnerable。

(as requested, consumers are aliases)