With february coming to an end, the screwdriver market has largely returned to pre-coup demand levels and futures and spot prices have increased significantly. Although prices then fell faster, overall the upward trend remained unchanged. The issue of demand remains a general concern, so what is the price trend in march? How long can market warming last? This paper will provide an analysis of the market situation and historical data。

From experience in 2024, extreme cold weather, which began one week before the spring holidays, not only blocked transport in some areas but also extended beyond the festival, affecting the start of work on the site. Moreover, market sentiment does not have high expectations for the latter. But this year has been different, with firstly, colder than last year, and secondly, markets' expectations for the post-markets far stronger than they were for the same period last year, and more optimistic. A simple analysis of data and the external environment follows。

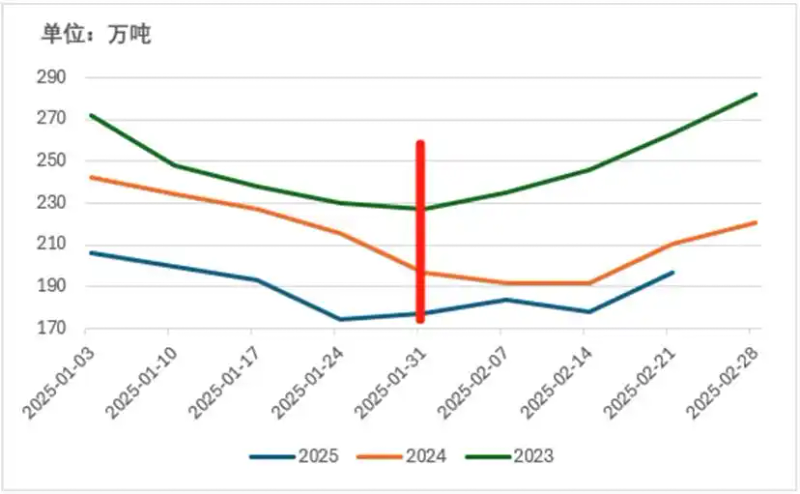

In terms of supply, the weekly production of screwd steel in february decreased significantly compared to the same period in 2024. The slight increase in production during the last week before the festival, but very few, and the decline in the co-production ratio are mainly due to weak policy incentives in the market, coupled with the poor level of winter storage and the expected disruption of some steel plants during the spring season, and the gradual erosion of incentives for steel production. The recovery from the festival was slightly better than the same period in 2024. See figure below:

The chart above records the movement around the week of spring holidays. As can be seen from the figure, the week of spring break marked with red line marks shows a slow recovery in actual production during the previous two years. In 2023, production recovered faster than in the first four weeks of spring holidays. In 2024, production fell by two weeks after the week of spring holidays, affected by extreme cold weather. Based on current data, it is highly likely that this year's production will return to the same levels in the period preceding the festival within four weeks. As at 21 february, production stood at 1. 9691 million tons, compared to 2. 0601 million tons on 3 january。

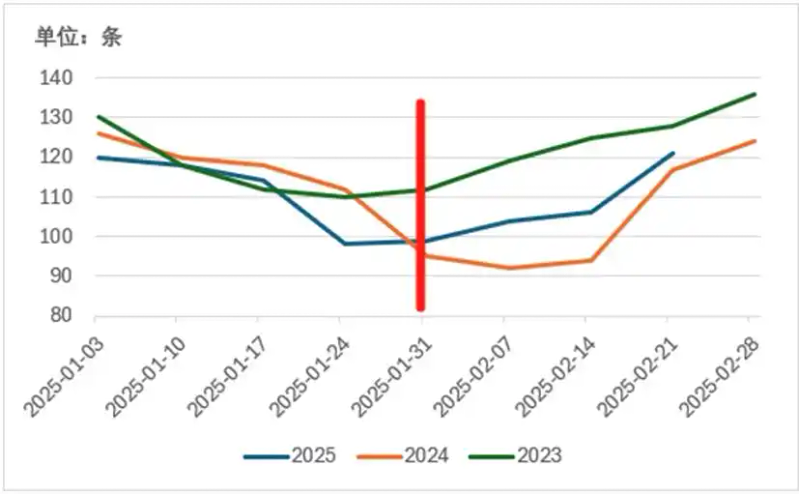

The actual number of construction lines opened in february by steel and steel enterprises (137 enterprises nationwide as a percentage of 64. 56 per cent) decreased significantly compared to the same period last month. According to the data, construction of the post-mortem production line is in better condition and 121 items have been opened, one more than the 120 at the beginning of january. The objective reflection of this year's rapid recovery in steel production was driven by prices. See figure below:

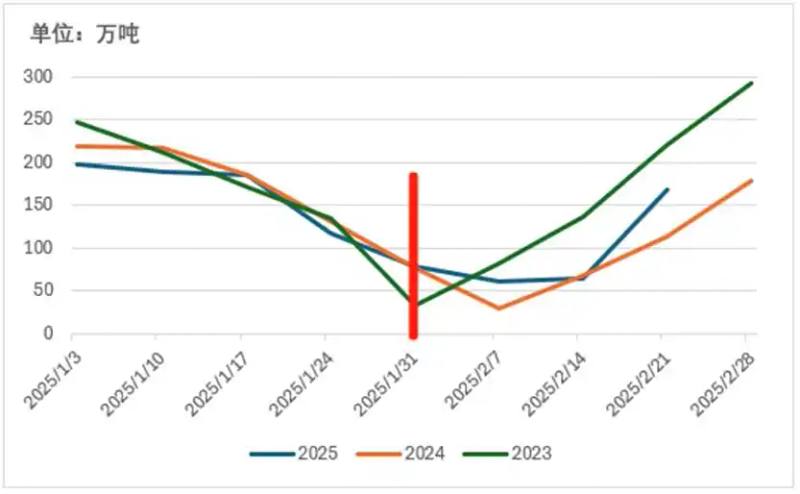

On the demand side, market demand continued to decline in january compared to december, with the overall decline being more pronounced. Consumption data show that the turnover of screwd steel for 1-4 weeks was 1. 97. 26 million tons, 1. 9005 million tons, 1,85. 15 million tons and 1169. 1 million tons, respectively. It is worth noting that demand fell significantly during the leave period, with demand falling by 54. 38 million to 774. 8 million tons in the same period in 2024 and demand falling by 1,004 million to 3276 million tons in the same period in 2023. Looking back at production data, it can be seen that during the spring season of 2023, while demand declined significantly, recovery was fast, leading to faster recovery. In 2024, demand continued to decline one week after the festival, resulting in successive price declines between mid-february and early april due to slower recovery. According to the data, while demand recovered slowly in 2025, even slower than during the same period in 2024, the momentum of growth subsequently prevailed. See figure below:

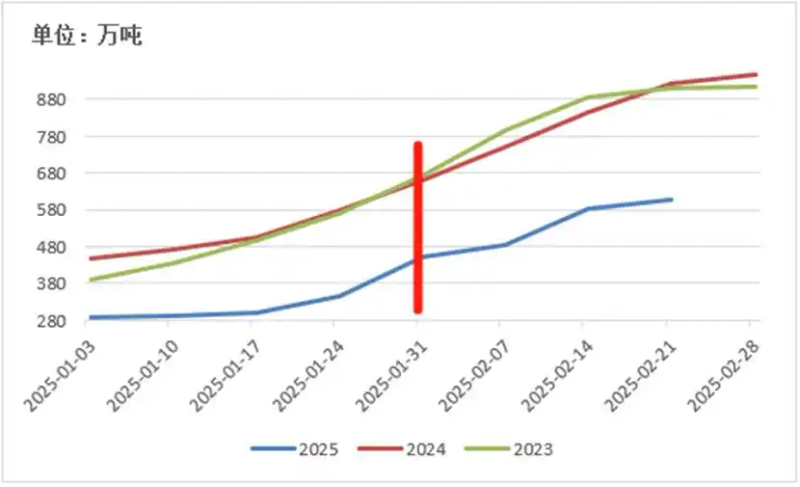

In summary, after spring holidays, the production of screwd steel recovered faster, the production line started more actively, the demand recovered more explosive and the stock level was generally normal. There are two main reasons for the better recovery. First, the recent re-entry of construction units in the downstream market head is better than last year, which continues to increase market prices. As at 18 february, the funding level for the sample construction site was 55. 38 per cent, an increase of 1. 11 percentage points over last year's post-coup period, of which the funding level for non-housing projects was 57. 05 per cent, an increase of 1. 41 percentage points; the funding rate for housing projects was 47. 23 per cent, a decrease of 0. 15 percentage points from last year's post-coup. Moreover, faster growth in downstream demand has greatly enhanced market expectations and has somewhat supported prices。

Individuals believe that, at the domestic level, in addition to the relatively rapid growth in real downstream consumption data, the convening of the major conference in march has significantly raised market expectations. Among the important meetings to be held in march are the fourteenth session of the national political consultative council, which was held three times on 4 march, and the fourteenth session of the national people's congress, which was held on 5 march, and the expected reaction of the market to the conference's policy on the real estate sector at the end of february and early march. Moreover, the recent explosion in deepseek has also marked china’s full-blown technological superiority over the west, resulting in the announcement last weekend by morgan stanley, a leading investment advisory body, of a multi-china asset, knowing that last september 24 was far more crazy than usual, but morgan stanley did not mean a real look at the multi-china market. This time, foreign investment, represented by morgan stanley, looks at multi-china assets in a comprehensive manner, also heralding a turning point in the chinese economy。

From overseas, trump’s successor to the us president increased china’s tariffs by only 10%, while most policies focused on matters such as its domestic strategy against democrats and ending the russian-uu conflict. While a few countries outside the united states impose tariffs on our steel products in the short term will affect price trends, in the long run the impact will be more limited. In terms of general trends, trump will continue to pursue a weak dollar policy based on a fundamental policy of returning manufacturing to the united states, resulting in a fall in the dollar index and higher prices for large commodities. Moreover, the relative improvement in the environment abroad has contributed to domestic financial sentiment and increased financial activity。

In the light of current price trends, screwd steel prices are subject to a combination of factors and are more affected by events. For example, as a result of tariffs imposed by a small number of countries on our steel products, futures prices, after having experienced a sharper fall, are expected to be rapidly withdrawn from exports within the window (8 march) before they are then imposed, and guangdong province is the first province to issue specific bond funds to buy stock of land boosting terminal needs. There are also rumours that crude steel production will be reduced by 50 million tons this year and 20 million tons next year. The anecdotal has also contributed somewhat to the price rise of screwd steel futures。

As a result of the overall optimistic and price-resilient bias of the current screw steel market as a whole, combined with policy expectations for the upcoming major conferences and expectations for a warmer demand downstream, prices in the chain steel market are expected to rise further in march, with the market generally seen as largely dominated, but attention should be paid to the price pressure of the black swan incident。