"clerator lee, the theoretical cost of this product is $120, we're selling $150, we're having a 20% maori rate." the boss looks at the offer and has full confidence。

"but the boss..." you're going to stop saying, "well, actually, this product is actually losing money this month."

This is a classic conversation between the financials of numerous manufacturing enterprises and the owners. What's the problem? The theoretical costs are enormous, and the real costs are so strong

Today, we are here to open the veil between the theoretical costs and the actual costs and see how far the gap between ideals and reality is。

I. Theoretical cost: the “ideal country” of finance

The theoretical cost, also known as standard or target cost, is the level of cost expected by the enterprise in its ideal state。

The formula is simple:

"theory cost = material quota + working-hour standard x wage rate + cost standard"

For example: the theoretical cost of a certain component

- materials: 5 kg steel x 10 yuan/kg = 50 yuan

- manual: 2 hours x 30 yuan/h = 60 yuan

- manufacturing costs: 2 hours x 20 dollars/h = 40 dollars

- theoretical cost: 50 + 60 + 40 = 150 yuan

Characteristics of theoretical costs:

Based on standard processes and quotas

Ignore anomalies and waste

Simple calculation, easy pricing

It's a cost-control “stamp”

But the problem is that actual production can take 5. 5 kg of materials, take 2. 5 hours, produce waste... Theoretical costs are like diet targets, but reality is cruel。

Ii. Actual costs: realistic “bonesy beauty”

The actual cost is the real cost incurred in the production process and the true data that are accounted for at the end of the financial month。

The same part, the actual cost could be:

- materials: actual consumption of 5. 5 kg x $10 = $55 (0. 5 kg wasted)

- manual: actual 2. 5 hours x $30 = 75 (low efficiency)

- cost: actual share of $50 (additional cost of equipment failure)

- actual cost: 55 + 75 + 50 = 180

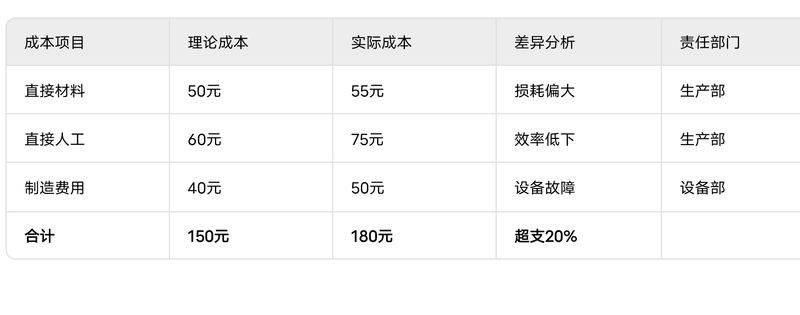

Look, there's a gap: 150 in theory, vs, 180 in real

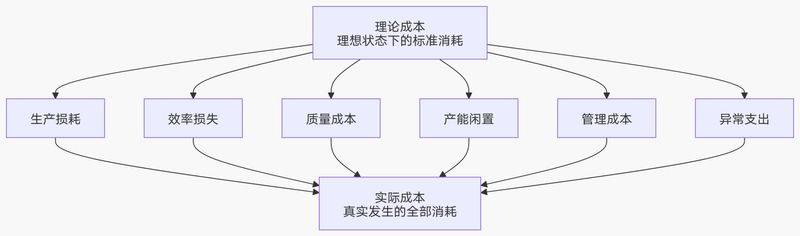

Where does the gap come from? Six “cost killers”

The figure below provides a clear picture of how theoretical costs are being “added” to actual costs at various stages of real production:

Here's a detailed analysis of each of the cost killers:

1. Production losses (material differences)

- theory: 5 kg steel

- actual: 5. 5 kg spent on material loss, operational error, process waste

- gap: +5

Loss of efficiency (manual difference)

- theory: two hours

- actual: 2. 5 hours for start-up operations, ageing equipment, waiting materials

- gap: +15

3. Quality costs (hidden deepest)

- return cost: bad re-processing

- loss of scrap: unrecoverable direct end of life

- client complaints: return of goods, compensation, loss of reputation

4. Capacity idle (fixed cost-sharing)

Fixed costs such as depreciation of equipment, rental of plant, etc., increase the cost-sharing of unit products if the capacity is underutilized。

5. Management costs (vulnerable to neglect)

Poor production plans, delays in the distribution of materials and inadequate personnel management are quietly increasing costs。

6. Unusual expenditure (accidents)

Maintenance of equipment in case of emergency, overtime, etc。

Iv. Theoretical cost vs actual costs: data comparison tables

Let's see the gap more intuitively through a specific data comparison:

V. How to close the gap? Four masters of finance

1. Establishment of a standard cost system

- establishment of reasonable material quotas and working hours standards

- regular updating of standards to ensure their sophistication

- make standard costs the basis for evaluation

2. Implementation of variance analysis

- monthly analysis of actual versus standard costs

- identification of causes of discrepancies and identification of responsible departments

- establishing and tracking improvements

3. Advance production

- reducing seven major wastees (overproduction, stockpiles, handling, waiting, etc.)

- implementation of 5s management to improve efficiency

- introduction of continuous improvement mechanisms

4. Enhanced performance appraisal

- include cost indicators in sector and individual performance assessments nuclear

- establishment of cost-saving incentive mechanisms

- develop awareness of full-time costs

Vi. Cost reports to the boss should be written like this

Traditional reports:

“boss, the actual cost of a products this month is $180, which is $30 over the standard.”

Improved cost analysis report:

“boss, the actual cost of product a is $180 this month, which is $30 over the standard, mainly due to:

1. Material depletion increased by $5 (17 per cent) due to new staff not operating with proficiency

Reduced manual efficiency by $15 (50 per cent) due to equipment failure

3. The manufacturing cost overrun of $10 (33 per cent) resulted from recommended measures for emergency maintenance:

- strengthening the training of new staff (ministry of production)

- preparation of a preventive maintenance plan for equipment (ministry of equipment)

- it's expected to drop by $20 next month."

Summary: theories are compasses, actually voyages

Theoretically, cost is the orientation of cost management and the actual cost is the barometer of business performance。

Smart finance does not complain about gaps, but:

- prognose with theoretical costs

It's a real cost analysis

- improve with variance analysis - promote efficiency gains in business reduction

The highest level of cost management is not clear accounting, but rather accounting-driven business improvements that allow theoretical costs to be unlimitedly close to actual costs and maximize business profits。

Ladies and gentlemen, is there a big difference between the theoretical and actual costs of your company? How do you analyze it? Welcome to the comment section to share your experience