Overview: guangdong prices showed a pattern of upswings and downs in 2024. At the beginning of 2024, the macro-pregnancy and post-spring inertia increased overall. But with the continued weakness of basics and poor demand performance, spot market prices continued to decline. The construction of downstream sites in the guangdong region has been suboptimal and steel prices have continued to decline. Since the fourth quarter, spot prices have been supported by a gradual recovery in downstream demand and a reduction in supply-side pressures. In the run-up between strong expectations and weak realities, 2025 entered. Will the market fully recover with the constant stimulus of macroeconomic policies? I'm going to get a quick analysis from the following。

I. Functioning characteristics of the guangdong construction steel market in 2024

In terms of prices, in the previous november, the guangdong market had been 3,560 yuan/t, a decline of 519 yuan/tonne over the same period, or 12. 7 per cent; the overall pattern of shock was low, with the highest price differential of 1060 yuan/t。

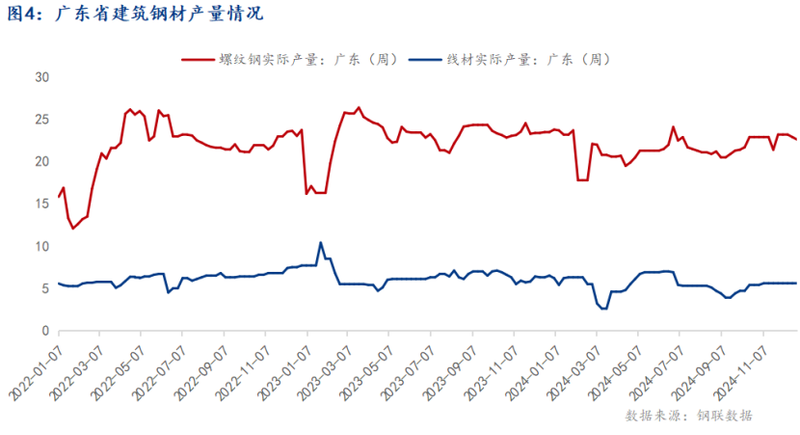

On the supply side: in 2024, the total production of steel from the two large buildings was about 45. 9 million tons, an increase of about 1. 7 million tons over the same period. Of these, the production of furnaces was approximately 26. 8 million tons, approximately 1 million tons less than the same level。

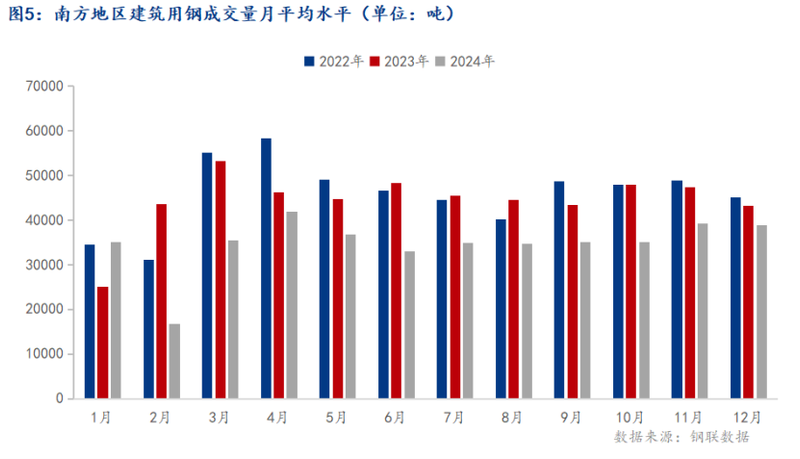

3 on the demand side: in 2024, the sample traders had a daily turnover of about 3. 53 million tons, a decrease of 22. 4 per cent over the same period; demand for construction materials in guangdong was about 28 million tons between january and october, a decrease of about 12 per cent over the same period。

In terms of stocks, the average annual stock of construction steel in the guangdong market was 476. 9 million tons in 2024, while the average annual stock of construction steel was 73. 11 million tons in 2023, down from 25. 42 million tons in the same year, a decrease of 34. 7 per cent. Its stock peaks at 78. 24 million tons, its grain value at 21. 43 million tons and its margin at approximately 568,000 tons, with a downward trend in the total stock。

Review of the operation of the guangdong building 2024

1. Price trends for construction steel in guangdong

In 2024, construction steel prices in guangdong rose year after year, with a low recovery in performance and a sharp rebound in the fourth quarter. By the end of december, the average annual price was $3688 per ton, a decrease of $391 per ton compared to 2022, or 10. 6 per cent. The highest price for the year was 4,200 yuan per ton at the beginning of january, the lowest was in late august, 3150 yuan per ton, with a volatility of 1050 yuan per ton, with price fluctuations of less than 1,200 yuan per ton in 2022 and 910 miles per ton in 2023. In contrast to the previous two years, market shocks continued to weaken after january and markets continued to fall under weak demand. Prices rebounded significantly in october with macro-strength expectations。

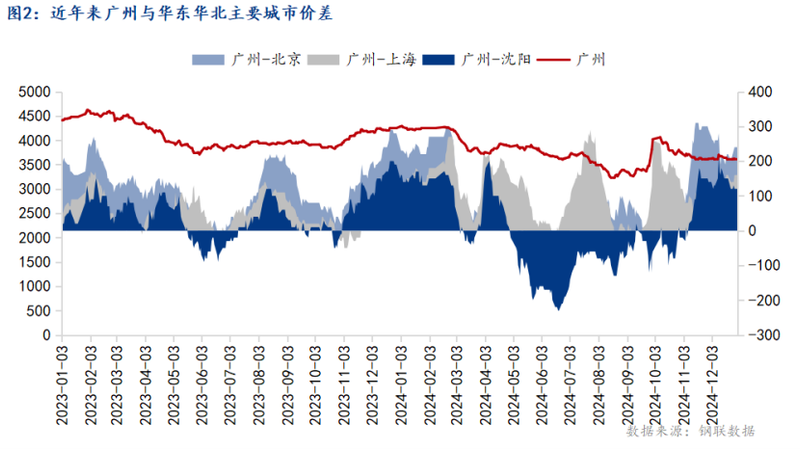

2. Comparison of guangdong and extra-regional market prices

In recent years, the resistance to local resource absorption has continued to increase as production enterprises continue to expand in both regions. As a result, the province's outer space in guangdong has become increasingly crowded. After 2023, overall demand continued to show a downward trend in 2024, leading to an imbalance between supply and demand, with guangdong's high price advantage weakened, with the difference in 2024 between beijing, shanghai and shenyang of approximately 98 yuan/t, 190 yuan/t and 3 yuan/t and the difference between beijing and shenyang continued to narrow。

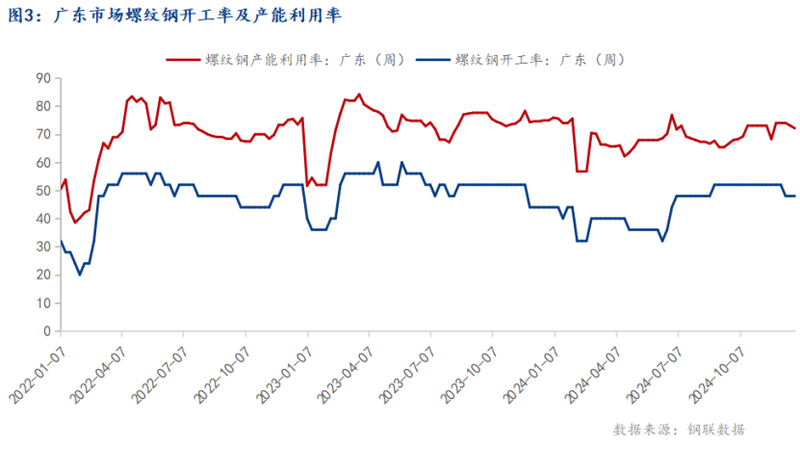

3. Construction steel production in guangdong province

The rate of start-up in the province has stabilized at over 60 per cent compared to previous years, but the rate of start-up has remained low at over 50 per cent by june, then fell below 50 per cent, at a minimum of 34. 85 per cent, again after october, and overall supply-side pressure is still fairly high. The main reasons for this are poor demand performance, persistent weakening of the prices at the end of the product, narrow corrosive spreads, the fact that the plant is largely in a deficit, low productivity motivation, combined with the impact of old and new national marking shifts, and the fact that steel plants have opted for reductions and shutdowns due to the effects of stockpiles. After october, with macro-information stimulus, steel prices rose markedly and profits recovered from steel plants, resulting in increased productivity。

Review of construction steel consumption and stocks in guangdong, 2023

The market is high and low. Okay

Owing to, inter alia, declining demand for real estate, sample traders averaged 353,000 tons a day in 2024, a decrease of 22. 4 per cent. Since 2024, demand for post-conceptual demand has declined by approximately 12 per cent from january to october, when demand for construction materials in guangdong was estimated at 28 million tons, compounded by heavy rainfall in the south。

Two, pre-inventory, low

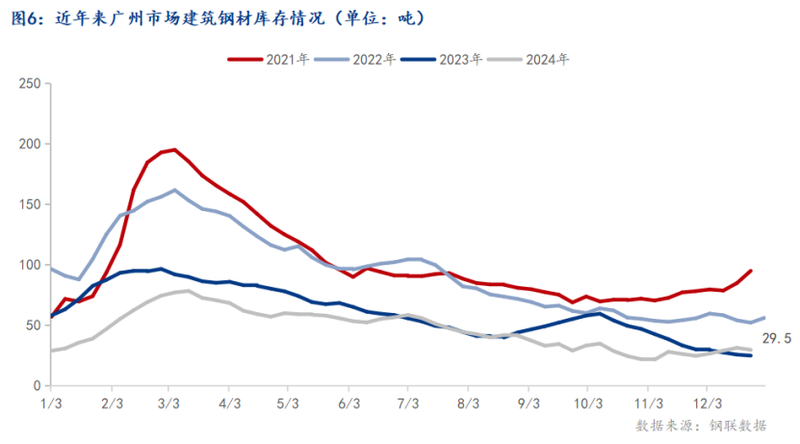

By december, 295,000 tons of social stocks of building materials in the guangzhou market had been reduced by approximately 50,000 tons from the same period last year. This year, as a whole, the second quarter has been slow and the third quarter has accelerated, mainly because of the effects of continued rainfall in the southern region in the second quarter, while steel plants have not experienced significant reductions and are not well-released; the three quarters have been replaced with old and new national standard resources, the market has accelerated the pace of delivery and the landing bank has accelerated。

Core view of the operation of the construction steel market in guangdong, 2024

On the supply side, there is still a relative imbalance between supply and demand in the province. Given the new capacity in 2024, supply pressures throughout the region remained unabated throughout the year. For the time being, however, the supply side is still disproportionately affected by cost support, and there is a balance between supply and demand in the region between initiatives such as actively organizing production controls. While the current low social reservoirs also have some support for market prices, weak demand for building steel as a result of reduced building construction is the main reason why profits from steel plants are difficult to repair。

On the demand side: the high-level meeting in december was still somewhat mood-driven at the market end, with some positive expectations for the market, both in monetary policy and in the fourth quarter of the sprint. In addition, despite a marked contraction in demand downstream throughout the year, there is still some support for spot prices and demand performance in mercosur at the end of the year。

On the price side, the price of construction steel in guangdong province as a whole showed a downward spiral throughout 2024, with lower prices rebounding since the fourth quarter but still below the same level as last year. Markets are currently largely in a weak balance. In the short term, steel prices may be weak in the basics and macros of the game (under an inter-zone shock), leading to winter reserves。