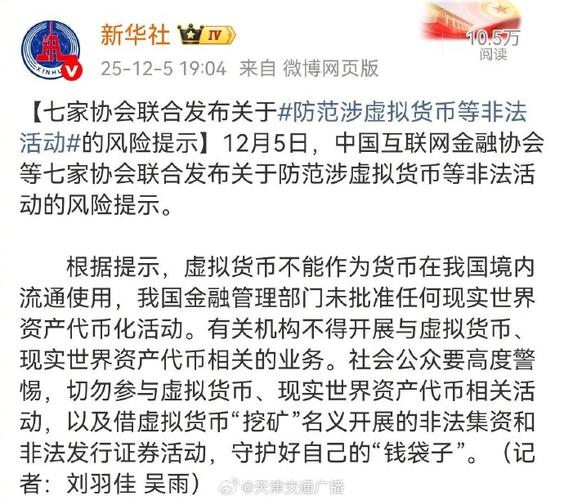

When virtual monetary concepts, such as stabilization currency and rwa tokens, are rapidly warming in the name of “financial innovation”, a regulatory action that covers the entire financial chain should be heard. On 5 december, the china internet finance association, in association with six authoritative associations, including banking and securities, made simultaneous statements to define the red line for the regulation of virtual currency-related operations with a “total ban” attitude. This joint action, which cuts across banking, securities, payments and internet finance, is not only a precise blow to the recent illegal activities of virtual currency, but also a chain-wide regulatory network that provides a firm line of defence for financial market stability。

Multiple traps behind concepts: real harm mapping of virtual currency

The harm caused by virtual currency-related activities has long gone beyond mere investment risks to reach the “high-risk areas” of illicit fund-raising, the distribution of fraud and money-laundering offences. The chinese internet finance association, the china banking association, the china securities association, the china securities and investment fund industry association, the china futures association, the china association of listed companies and the seven china payments clearing-house association risk tips were precise in identifying the nature of three types of high-frequency risk carriers, and the judicial case revealed the harsh truth behind their “fiscal myth”。

The “smuggling harvest” of air coins is the most hidden. By way of example, it claims that “cell phones can be mined” with “zero-cost high returns” and actually induces participants to “head up” through multi-level distribution systems, inviting numbers to “drilling” at a rate directly linked to activity, creating a typical distribution pattern. In july 2025, the pi network core team was exposed to the sale of 12 million zirconium coins for $8 billion, while a number of related cases have been investigated in the country, involving more than $200 million in the gang of jiangsu. Such tokens are not supported by substantive technology, are not clearly applied, operate in a totally non-transparent manner, and so-called “values” are maintained by false propaganda and, once the financial chain is broken, the investors are left with nothing。

The stability currency hides the risk of “illegal financial access”. Despite its claim that it is “linked to the legal currency” in order to maintain price stability, the seven associations have made it clear that the currency of stability currently fails to meet the regulatory requirements of customer identification, money-laundering, etc., and has become a tool for money-laundering, fund-raising fraud and the illegal cross-border transfer of funds. This characteristic became a “money handler” for a criminal group. In the 2020 guics virtual currency case, the principal of the crime was the transfer of the proceeds of crime through a virtual currency, resulting in the loss of more than rmb 1. 7 billion to over 29,000 investors, who were sentenced to life imprisonment for the crime of pooled fraud and money-laundering。

The emerging rwa token (real-world asset monetization) is not a “coercive haven”. Such activities, which are financed through monetization interests, run the risk of false assets, business failures and speculation, and have never been approved by our financial authorities. Some outlaws have packaged poor assets into “high-yielding coins” and sold them through offshore platforms, using asymmetric information for fraud, which is often difficult to trace。

At the level of the financial order, the anonymity of virtual currency, its cross-border nature and its severe impact on monetary sovereignty and financial regulation. Its price is out of the reach of the real economy, with a 30 per cent decline in a single month in 2023, which is highly likely to trigger speculative bubbles; at the same time, “mining” activities are energy-intensive and wasteful, and run counter to the “bicarbon” goal, and enterprises may also gain credit support by illegal means, crowding out the real economy's financial resources。

The whole chain is closed: the red line is the line of responsibility of each industry

This time, the seven associations made a joint statement, not as a stand-alone risk alert, but as a continuation and refinement of policies such as the 2017 proclamation on the protection against the risks of the financing of derivatives, and the 2021 circular on the further prevention and handling of the risks of firing virtual currency transactions, resulting in a complete chain of regulation of “law-administrative regulation-industry self-regulation”. At the core of the breakthrough was the identification of specific “impermissible” borders for different industry institutions and the achievement of regulatory neutrality。

Banks and payment agencies become the first level of “money control”. The bulletin explicitly requires such institutions to refrain from providing any financial services such as account opening, transfer of funds, credit support for virtual currency transactions, and to enhance customer due diligence and timely reporting of suspicious transactions involving virtual currency. This directly cut off the flow of funds for virtual currency transactions — previously, in the fraud of the obit virtual currency exchange platform, criminal groups had used third-party payment channels to transfer funds, making it difficult to recover the $460 million involved, and new regulatory requirements would deter such loopholes from the source。

Institutions such as securities, funds, futures etc. Are prohibited from “bridging”. The bulletin prohibits such institutions from providing services such as distribution, trading and marketing services for virtual currency and related financial products, blocking the path of virtual currency penetration into formal financial markets. In recent years, attempts have been made by some agencies to participate in a disguised manner in the name of “block chain funds”, “digital asset management”, and the ban has put an end to this kind of “painting”。

Internet platforms assume responsibility for “flow control”. As a central vehicle for information dissemination and technical support, the internet platform is required not to provide marketing campaigns, technical interfaces, etc. For virtual currency transactions, and to conduct a comprehensive inventory of non-compliance information within the platform. It solves the problem of virtual currency fraud, online transmission. - the frauds such as the money and the gucs spread through social platforms and short video channels, and the strengthening of the platform's oversight will significantly reduce its dissemination space。

It is worth noting that the scope of supervision has been extended to “operations in the territory of offshore agencies”. The bulletin makes it clear that the offshore virtual money service providers will be held liable under the law for their internal activities, their internal staff and their facilitators. This responds to the tendency of some institutions to “negatively circumvent regulation by using offshore licences” and to create “integrated internal and external” systems of control。

In-depth comments: the financial security logic behind joint regulation

Ho shihong, president of the chinese financial network and president of the china institute for the development of a culture of financial security, stated that the seven associations' cross-cutting joint voice was an accurate response to the virtual currency's “cross-industry risk” and that behind it was the core logic of our country's financial security — to work together to regulate the problem of breaking risks across borders, to strengthen market expectations and to provide a comprehensive warning to safeguard public property。

In terms of regulatory synergies, virtual currency risk has long breached a single industry: money flows depend on bank payment channels, propaganda for proliferation is based on internet platforms, and some of the scams are disguised as “financial products” involving securities. Previously, there might have been a “regulatory gap” in single-industry regulation, while the parallel operation of banks, securities, internet finance and others had resulted in a chain-wide control of “money-flow-products” and avoided a “one-size-fits-all” fragmentation dilemma. This synergetic model provides a replicable sample for addressing cross-cutting financial risks。

In terms of market orientation, a clear attitude of “total prohibition” has broken the “compulsory illusion” of some investors. In recent years, the concept of unlawful elements has been constantly retrofitting, from “block chain innovation” to “digitization of rwa assets”, with “policy acquiescence” to mislead the public. The ban, jointly endorsed by the seven associations, sends a clear signal that “virtual currency-related operations have no room for compliance”, helps to correct market perception deviations and discourage speculation。

For the public, the alert provided a clear “risk identification guide”. In combination with bulletins and judicial cases, virtual currency scams often have three main features: a revenue trap that promises “stable profits” “zero-cost high returns”; a marketing model requiring “collective commission”; and a packaging package under the guise of “outside compliance” “technology innovation”. The public needs to bear in mind that civil legal acts relating to virtual currency are null and void, that the loss of participation in the transaction is self-individing, and that a distance from the various related activities is the only option for safeguarding property。

In terms of industry development, the ban does not negate technological innovation, but rather defines the “boundary for innovation”. While technologies such as block chains have their own application value, the speculative properties of virtual currency and regulatory circumvention are at odds with financial stability objectives. The regulation clarified the principle that technological innovation cannot go beyond the legal bottom line and led industries to apply technology to compliance areas such as supply chain finance, cross-border payments, and to achieve “de-foaming” healthy development。

As the virtual currency concept continues to evolve, regulation will continue to evolve dynamically. The joint action of the seven associations is both a risk alert and a regulatory statement - - any attempt to carry out illegal activities in the name of virtual currency would face a double blow between industry-wide control and legal accountability. For market subjects, fear of the red line is a prerequisite for survival; for the public, rational identification of risk is property security. Only by working together can the breeding ground for illegal virtual currency activities be completely eliminated and the stability and security of financial markets protected。