We often say that business is about money, good people, middle people, good people. Then it seems equally important for training schools to manage money. Too many small partners think this is a matter for the boss, so it is not very well understood. Today, let us look at some of the issues that must be addressed by training institutions in the financial management of money。

How educational training institutions manage their own financial-pedagogical management systems

When it comes to finance, many people have the stereotyped impression that finance is the irregularity of telling themselves in a serious manner which documents are filled out, which amounts cannot be reimbursed for non-conformity, which items are not priced in three, which stocks need to be used quickly and cannot be purchased ..

The above impressions are, in fact, stereotyped because each of us is exposed to different financial needs. In fact, finance is very important in an enterprise, not the big logistics that everyone remembers. They control costs, carry out pre-counts, report taxes, remind us of the risks we can see. Today's talk is not about reimbursement, filling out forms, but about the health of school operations。

Misuse of arrears to calculate profits

Training institutions and many enterprises are very different in their calculation of income, and the costs charged by training institutions are not hand-in-hand, hand-in-hand, non-negative merchandise transactions, but pre-paid by clients, and those that have not yet incurred the expense of the hours spent are, by implication, arrears. The real income of the training institution is not those arrears, but the time spent on the course. It is therefore not correct to use a cash flow statement to confirm how much money and profits are currently in their schools。

Reference may be made to previous articles

Real profits are calculated on the basis of the cost and time already incurred. The failure of many small training institutions during the epidemic was due mostly to late-stage problems caused by the misappropriation of arrears as net income. If, of course, it was not a body that operated in good faith, but rather an institution that sought to be listed and put on the market, it would be quite different。

Misuse of flow accounts as management statements

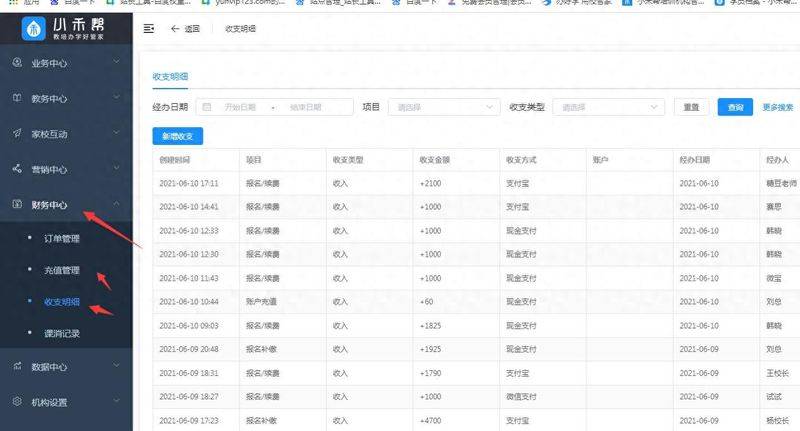

Did your school's finances give you a weekly, monthly, quarterly check? Did those detailed loans, mortgages, make you uninterested, go straight to the aggregate, look at the sum of the cash flows and the sum of the costs, and turn it off in a hurry

Of course, this is not a financial complaint, and many schools are not accountants, but tellers. They have exhausted their schooling, accumulated their jobs, produced a floodbook, and you have not raised any objections. So it can only happen year after year as described above。

Indeed, the role of finance in management is enormous and they can provide a very good job guidance to department managers in marketing or operating. If you can ask your finances to classify those flow statements according to the purpose for which the budget line is used, the accounts, analysis are very relevant for the operation of the school. In the analysis of the market accounts, when the finance indicates that the cost of welfare activities by the manager of the ministry of markets in the last quarter was significantly reduced relative to the budget and was diverted to the next line, we find that the transfer of clients to the school has declined, while the extension points under the line have decreased their capacity (thus increasing the number of points)。

The flow of water could not be used as a management statement, and financial disclosure without analysis was not good。

Red cannot be separated

Some schools run over the course of the year, and several shareholders stretch their necks and wait for a split. It's been a year of hard work, and it's hard for the profit-making people to look at the books, and they can't keep a single score. There is no way to finance it, but listen to everyone. Everyone is more powerful than himself, so don't say anything, and i will do what you say。

It is important at this point to remind shareholders that 10-15 per cent of a company's profits are absolutely non-distributable, and that it is necessary to expand, renovate, and encounter some unresisting accidents. It's terrible to have a red fraction。

Neglect of inventory management

It's a school that has stocks, market materials, office materials, cleaning materials, teaching aids, books..

Small partners in business management have natural leakages in warehouse management and a massive desire to do things that can lead to large-scale purchases of materials. Financial failure to manage and alert would result in considerable waste。

How can stockpiles be reduced? You don't have to talk like a housekeeper, first, to make sure that your warehouse is not too big (this is important); secondly, to add your stock to the operator's appraisal target by calculating it separately at 20 per cent per year. For example, when you buy $100 at the end of the first year, you are charged directly to the operating management forms for $20 for no reason, and at the end of the second year you lose another $20 until it's over. Each year after the accounts, the operator is asked to explain why the output was so depleted and how it was circumvented。

I don't know

Some schools, with large amounts of cash lying on their permanent accounts, lie so quietly. Nor was there any awareness on the part of the finance staff to remind their bosses whether to use the cash for short-term security purposes. Everything's waiting for the boss to ask, to warn. It is also a waste of resources. Of course, there can be no too much greed, no stability in everything, no risk of investing, as the laws of the country permit。

So, finance needs to be supported by an effective tool

How educational training institutions manage their own financial-pedagogical management systems

Xiaowei school management system