"is there a lot of people who buy increased life insurance? For two months, the bank's customer manager called me and said that the interest rate was very high and the sale would be discontinued.” in an interview with ms. Zhang, the consumer said, “i usually buy only r1, r2, and the customer manager explained several increases in life insurance, which i did not understand and which ended up not buying.”

As ms. Zhang noted, “sold hot, high-yielding, imminent fall” is the recent impression by many consumers of increased life-long insurance。

In march of this year, the former bank insurance board's personal insurance department organized an insurance industry association and over 20 life insurance companies to conduct research around the liability cost of the venture, the matching of liabilities and assets, and the impact of the reduced liability reserve on companies。

This research has led to a discussion within the industry of a downward revision of the scheduled interest rates for insurance products. A number of institutions indicated that in the future, the scheduled interest rate for newly developed products would be reduced from a maximum of 3. 5 per cent to 3. 0 per cent, and that insurance products, close to 3. 5 per cent of the scheduled interest rate, would also fall under june。

In july, economic journalists for the twenty-first century noted that, at present, high-level increases in life insurance are being discussed on social platforms, such as microcafés, little red books and others。

After the consultation, the insurance broker informed the press that “the landing was a major trend, but not precisely at the end of june. Xxxx now has only one additional life risk product on sale, and without a new replacement, the lower shelf faces a break. They are also developing new products, but it takes time to design, file and pass.”

Since last year, products such as the increase of 3. 5 per cent or more in the scheduled interest rate, such as life-long insurance, have become the “open-door red” force of insurance companies in 2022 and 2023, in the context of the downward revision of bank statements and time deposit rates。

Why is the increase in life-long risk going down in a low interest rate environment? What are the dilemmas in the process of transforming the life-risk industry behind the downward adjustment of scheduled interest rates

Net-red products at lower interest rates

“the increase in life insurance was not easy to sell when it was first introduced. These two years have suddenly become a major sales force.” one national customer manager, li yang (alias), spoke to the journalist。

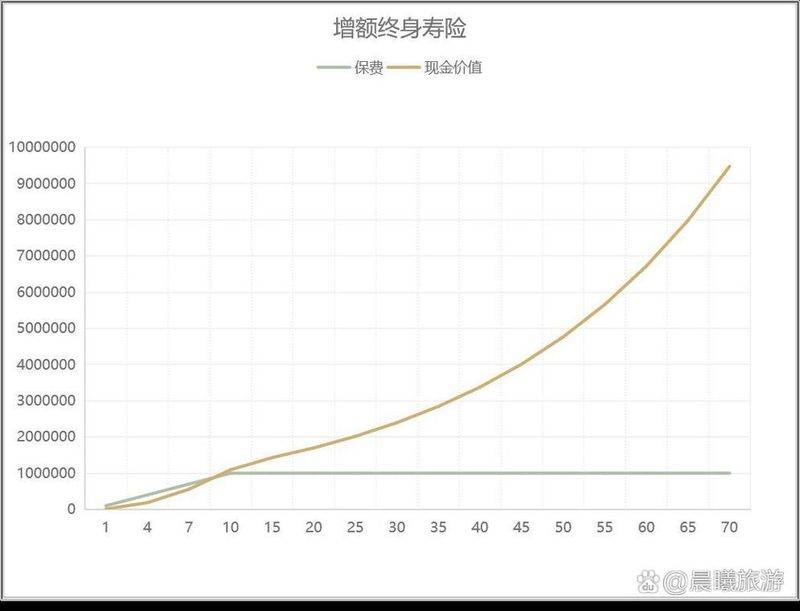

It is understood that the increase in life-life insurance was born in 2019, distinct from the traditional life-risk of fixed insurance, and that the increase in life-cover insurance will start to increase from the second insurance year, with an increase in cash value。

In the case of insurance products, the insurance is the amount to be paid by the insurance company to the beneficiary at the time of the unexpected risk, the determination of which is dependent on a number of factors, while the cash value is accumulated by the insured person's contributions under the terms of the contract, and is an asset of the insured person who can be withdrawn or paid for the premiums, loans, etc。

In short, the premium is the sum paid by the insurance company in the event of an accident; the cash value is the amount available to the insured at the time of refund, which can also be used to draw, borrow or pay future premiums, etc。

Li qiang indicated that, in his view, the core of the increase in life expectancy was the value of cash, i. E. The early “lock-in gains”。

“the growth of the margin is unattractive for consumers, and what matters is the value of the cash, that is, the gains that can be made.” "the value of the cash is written in the contract, and whatever the proceeds of the insurance company, that's all you can get

In li's view, the quality of “advanced lock-in gains” was at a disadvantage at the beginning of the roll-out of the incremental life risk product, but has now been transformed into an advantage。

In recent days, a number of banks have announced that they will adjust the interest rate for the notification and agreement deposits. Previously, in early may, the relevant supervisory authority issued a circular to adjust the ceiling on the rate of self-regulation of deposits in bank agreements and notifications。

“because the increase in the cash value of the increased life-long risk is fixed. If the future interest rate environment is upward, it may be `reduced'; the interest rate goes down and buys it is `pre-locked gain'.” “it can be said that, although there is also a trader's adjective, the increase in sales for life is a consumer's feedback on the direction of macro-market interest rates.”

Li xian's views are very representative among the sales staff of insurance products。

Journalists look at social media such as twitter, the friends circle, and red books and find that many insurance agents, brokers and financial platform client managers have similar ideas。

In the assessment of insurance products, a larger number of brokers measure the three dimensions of the value of increased life-long risk cash, the speed at which the value of cash exceeds the premium, and the ease at which insurance products are reduced。

“the three indicators correspond to interest rates, return speed and ease of access.” an insurance broker said to journalists, “many consumers now wish to buy savings and property, but also to be flexible. So we recommend products that have a low threshold of reduction and a high cash value."

In response, one insurance agent, who has worked for more than 10 years, has stated that measuring the value of an increased life-cycle risk product only in terms of the growth in cash value is a short-sighted act that can easily undermine consumer understanding of the concept of insurance。

“the charm of insurance is compound interest, which requires long-term holding.” chen suggests, “the market rate of the 3. 5 per cent increase in life risk products is substantial, but the annual cash value varies. Some products are growing faster and slower, while others are slow and faster. For example, many head agencies have added life risk "back" it's 10 years fast, but it's growing pretty fast; there's a lot of products on the market. It's only 5-7 years to return, but it's not conducive to long-term possession.”

Another insurance agent, wang, who had worked for more than 20 years, said to journalists that measuring the increase in life insurance in cash value terms alone would have meant a dilution and partialization of insurance products。

“many salespersons now sell products with vague concepts. For example, the growth rate of the premium is not an interest rate, nor is the growth rate of the cash value, and the insurance product itself does not say `interest'.” according to wang, “the bright spot of the increase in life-long insurance lies in the `double increase' in the value of the premium and the cash, which gives the insured a risk guarantee, which is the core value of the insurance product and should not be ignored”

The wang stressed that the increase in the insured value of the insured product, expressed as the interest rate, was an erroneous reading of the insured product, “which would lead many to misperceptions about the insured product and discourage longer-term sales”。

A hard-to-get insurance company

Regardless of the timing of the fall in the life-risk product, which was set at 3. 5 per cent, the maximum pricing rate for the personal risk product was reduced from 3. 5 per cent to 3. 0 per cent, which was a significant trend and was moving closer。

In this context, since march, insurance salesmen from the major social platforms have launched a dramatic wave of increased life-risk campaigns。

In mid-june, a large financial platform even reduced from $10,000 to $1,000 the start-up of a high-level life-risk product discussed in a network, making final performance punches through the phrase “exclusive welfare” “shopping cards”。

In fact, this time the regulator required personal insurance companies to reduce the scheduled interest rates, with the aim of controlling the risk of spreads and cost differentials for insurance companies。

In the short term, high-pricing interest rates contribute to increasing the competitiveness of personal risk products and accumulate large premiums for insurance companies at the end of their liability; but in the long run, insurance companies are highly likely to generate spreads and operate to the detriment of firms if they are unable to find suitable high-quality targets at the end of the investment, guaranteeing a return on investment of more than 5 per cent。

The data show that in 2022, the returns on personal risk companies were largely unsatisfactory. The annualized financial investment return on insurance funds was 3. 76 per cent and 1. 83 per cent in 2022, as disclosed by the board. According to incomplete statistics by journalists, the average total return on investment for 59 non-market venturers was only 1. 76 per cent。

In the midst of intense market competition, more than product-based interest rates, which put considerable pressure on the investment side of insurance companies, are also likely to result in cost differentials for insurance companies。

In recent years, as a result of increased competition in the market and the homogenization of personal risk products, some under-known small and medium-sized insurance companies have had to increase their advertising and visibility while maintaining pre-determined interest rates on their products, while increasing the share of commissions to boost sales。

Bank customer manager li zhong said to journalists that insurance products currently offer the highest percentage of commissions for a large number of property items sold by banks, and that small and medium-sized insurance companies offer higher rates than large insurance companies。

“we sometimes prefer to sell the products of small and medium insurance companies. Pricing rates are low, quick and easy to sell; the commissions are also higher.” li zhong stated that “the commission for bank administration is low because it is its own team. The fund commission is not very high, the large insurance companies are more capable of their own sales teams, are less dependent on us, and are paid more by small and medium-sized insurance companies.”