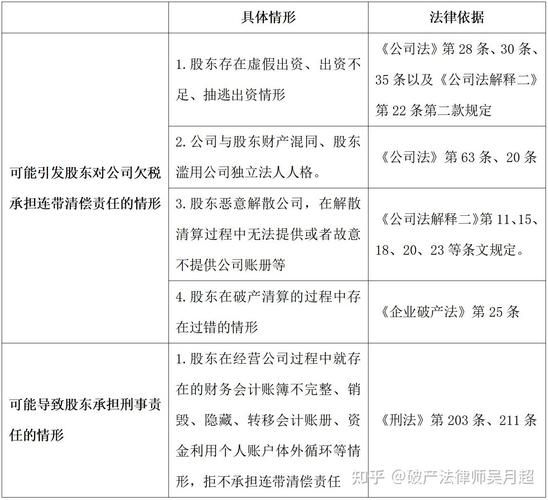

On 1 july 2024, the new companies act was formally introduced, making it clear that registered capital would be paid in five years. This has left a large number of entrepreneurs anxious, and with the proliferation of advertisements such as tremors, micro-credentials and other platforms, such as “intellectual property rights paybacks” (iprs) have claimed to be cost-effective and efficient in solving the problem of paying off. Are these ads a shortcut or a legal trap? Recently, late in the evening, journalists interviewed jiang yang, a member of the insolvency reform research group of the association of insolvency representatives of shenzhen city, to bring to light, in the context of genuine bankruptcy cases, the risk behind the commission。

“this type of advertising is largely unreliable and essentially a legal trap designed for shareholders.” chiang yang's soldiers opened the door and spoke openly of the danger of paying for it. In a recent bankruptcy case, mr. B.'s encounter was extremely alarming。

Mr. B, a shareholder of company a, spent much more money than he had pledged during his operation, but failed to do so owing to financial irregularities and lack of legal awareness. Following the introduction of the new companies act, the pressure to pay was sharply increased, and mr. B. Moved on to the ad of the “presidency to pay a dragon”, paying the chargÉ d'affaires to purchase a number of new and useful patents unrelated to the company's business, followed by an overvalued valuation report from the evaluation agency arranged by the other party, paying the price of these “shell patents” and completing the business register with a “cash payment”。

The seemingly smooth operation exposes the problem once the company is insolvent. The insolvency representative verified that the patent in question had never been produced and had no real value and that the evaluation report was clearly overvalued, and concluded that mr. B constituted a false contribution and required that it be fully replenished within the amount of interest paid on capital. Mr. B was even more regretful that his previous excess investment in real money and silver was not deemed to have been paid for failing to comply with the legal formalities. In the end, not only did he spend his office fees and assessment fees, but he also had to pay an additional amount of money to make up for his contributions, which had long been lost in the agency in which he was based。

In response to the advertising of “legal compliance with intellectual property rights”, chiang yang stated that intellectual property financing itself was permitted by the companies act, but that it was necessary to meet three rigid conditions: intellectual property rights were relevant to the company's main business and had practical value for use, priced by a fair assessment by a legitimate body of qualifications, completion of transfer of rights and full set of business and financial procedures, and it was not appropriate to finance all or most of them with intangible assets。

For the most part, the demarches on the market deviate from compliance requirements: the provision of shell patents that are not business-related, the search for agency-based high valuations, the mere production of surface business materials and the evasion of statutory conditions throughout. “in liquidation, the administrator checks the details of the patent's commission, assesses the qualifications, etc., and, if a forgery is discovered, the shareholders are deemed to have made false contributions and face supplementary contributions, administrative penalties and even criminal liability.” zhang yang warned that intellectual property financing should be available only when companies have high-value intellectual property rights that are highly relevant to the industry and can be evaluated. Among the many projects in which the chiangyang team of lawyers acted as insolvency representatives were the prosecution of false contributions by shareholders, the court ruled that the shareholders were liable for their contributions, and the directors of the companies were jointly and severally liable for their contributions。

Shareholders must therefore be sobered that legal “payment” is not a formality, and that the use of high-value, low-value intangible assets for high-value, non-utilised, or all or most intangible assets for high-value financing is clearly not justified and will appear under the magnifying lens of liquidation. The essence of these advertisements is to cover up substantive violations with formal compliance, and ultimately the shareholders themselves。

What should be done if the insolvency representative has erred in the collection trap, or if the insolvency representative has failed to do so in large quantities? Zhang yang indicated that it was crucial to commission professional lawyers with experience in bankruptcy and corporate law to prove to the court that funds had actually been made available through improved formalities and sufficient evidence, and that his team had already won many such cases. “the possibility of avoiding risks is greater when the company is in the ordinary course of business, so that it does not wait until it becomes insolvent.”

“the shortcuts are often the most expensive.” at the end of the interview, chiang yang gave advice to the owner: either the shareholders had gone through the legal formalities with monetary funds and did not run away from the funds; or the funds had been properly financed with intangible assets in strict compliance with the legal procedures. The bulk of the paid-in advertising on social platforms is fake, only to the extent that it is a formal “payment” that accumulates not only risks, but also potential future civil, administrative and even criminal liability. There are no shortcuts to compliance, and only by relying on professional strength can legal risks be truly avoided and business interests protected。

Shenzhen evening journalist, romin