From august onwards, the federación (guangzhou, journalist guan wanyi) raised cement prices many times. According to analysts, the current gradual trend towards a boom in demand for cement and a reduction in supply under the influence of overlapping and dual-control policies have contributed to the current price increases in cement prices in many places, including two wide and cloudy areas. In addition, it was analysed that many factors, such as current costs and energy controls, or profiting from head-to-head enterprises could accelerate the business shuffle。

In the secondary market, there was a marked rise in cement blocks on nearly 10 trading days. Cement blocks of co-flowing cement increased by nearly 14 per cent; the tower group (002233. Sz) increased by over 40 per cent, the top cement (000672. Sz) by over 30 per cent, conch cement (600585. Sh), 10,000 youths (000789. Sz) by over 20 per cent。

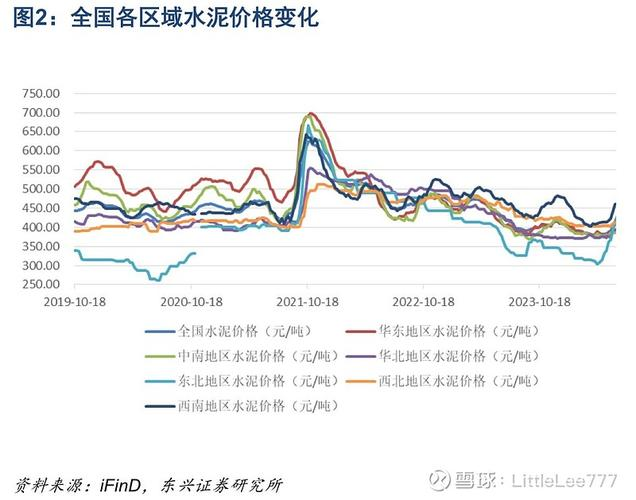

The price of cement is rising in two large clouds

Cement prices have recently increased in guangdong, guangxi and yunju, in the range of $50 per ton-80 per ton per ton per ton, and cumulatively in the range of $130 per ton to $230 per ton in august-september. According to industry sources, there have been recent reports that bulk cement in guangdong is still subject to price adjustment。

On 13 september, the 100-year construction network cement price index increased by $20 per ton, by 4. 11 per cent and by 10. 81 per cent over the same period。

In response, china's cement network analyst wei yu indicated that the current boom in demand for cement and the reduction in supply under the influence of overlapping and double-control policies contributed to the current price increase in cement prices in two wide, cloudy areas. However, the 100-year construction network cement senior analyst jiang yuanlin said to journalists that there was currently no significant increase in demand at the market level, that the downstream market was less receptive to price increases and that there was an overall lack of market value。

The cement industry has been known to have strong regional attributes. The price hikes in the two large, cloudy areas were more affected by the “two-control policy”. In august, nine provinces (districts) of guangdong, guangxi and yunnan, among others, provided a first-level warning on the control of total energy consumption in the issuance by the national commission for development and development (cnd) of the “brueboard of energy consumption by regions in the first half of 2021”。

Subsequently, several provinces responded quickly. In the recent past, the guangxi region has imposed production restrictions on local cement enterprises as a result of increased energy consumption controls, with the cement sector producing no more than 40 per cent of the average monthly production in the first half of 2021 and electricity loads in september, no more than 40 per cent of the average monthly load in the first half of the year. In september 2021, local cement production was reduced by more than 80 per cent on the august basis, with all cement enterprises peaking for no less than 40 days in october-december, according to the yunnan commission's energy limitation notice。

For its part, the tower group indicated that, in the current environment of dual-control energy consumption in guangdong and guangxi, the cement supply end was tightened and the company's cement stock was declining in an orderly manner. Traditionally, companies have been organizing their production in strict compliance with government requirements and adapting marketing strategies to market demand and supply. There have been no significant changes in the business environment, internal or external, as disclosed. The recent continued increase in cement prices will have some but little impact on company performance。

Young people said to journalists that jiangxi did not have a limited production policy and that the company was in full production. Because of the strong regional distribution of cement, the market is currently dominated by the jiangxi region and the border areas of some of the surrounding provinces. In the event of a large “price reversal” between the surrounding region and the company's main market, adjustments to the marketing structure may be considered in due course。

After the fourth of july, or the heights are stabilizing

According to a reporter from a cement company in guangdong, “some parts of guangdong are currently targeting the size of the enterprise to limit energy consumption. In this way, the production capacity of large plants is relatively high and the energy available is relatively high. If prices rise, there will be advantages for large firms. In addition, this may result in small enterprises being limited in capacity and losing some of their advantages in the face of larger priority projects.”

Jiang also indicated that many factors, such as current costs and energy controls, or profiting from head-of-the-art enterprises, accelerated the business shuffle。

It is noteworthy that, according to the semi-annual reporting data previously disclosed by cement enterprises, there are several enterprises that have not been profitable. According to wei yu, the main reason for this is the marked increase in the price of power coal since this year, the increase in production costs for enterprises, the sharper fall in cement prices between mid-may and the late july season, and the phased losses experienced by enterprises in some areas, which have now largely recovered to the level of the cost line as cement prices have increased since august。

In response to the cement forecast for the second half of the year, wei indicated that, in the current situation, the dual-control policy in several provinces was expected to reduce the overall supply of cement markets in the second half of the year. The demand for downstream real estate and infrastructure is relatively rigid. Depending on supply and demand, prices may rise considerably. The profits of most cement enterprises are expected to pick up in the fourth quarter, but, given the high level of production restrictions in some areas, the reduction will have a somewhat negative impact on the increase in profits。

According to jiang yuanlin, “the needs for the second half of the year are expected to remain essentially the same as last year. It is also expected that demand will be contained within a range of limits and that the level of supply and demand will be stabilized through the current dual-control policy of the state. As for prices, the current prices (both wide and cloudy) are expected to remain stable for some time, and i think they are expected to stabilize after the national day. Higher prices are more likely to stabilize. From an enterprise point of view, this year's cost rise is evident, and current prices are still under some pressure for the enterprise. In general, however, the second half is better than the first half of the year in terms of long-term industry patterns.”