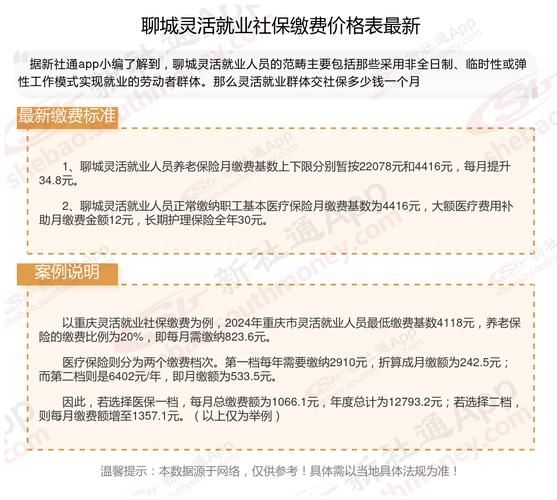

It is believed that many companies have recently been notified by the tax authorities that they are seeking to improve the rate of social security coverage, and that the owners are in a state of anxiety about paying their contributions. In the face of the trend towards compliance with the “social security pay-as-you-go” policy, companies are not only paid back, but also face delays and fines when they are subject to tax scrutiny. Chongqing and mao's team of lawyers, li yong, combined their long-standing experience as legal advisers and the laws and regulations in force, have put together five strategies, and the real way forward is to bring down the base of contributions by changing the wage composition and working patterns within a legal framework。

I. Remuneration benefit: the contribution base for social security is based on “total wages”. According to the regulation of the national statistical office on the composition of wages and the letter from the social insurance centre [2006] the large number of benefits and expenses is explicitly excluded from the total wage. Businesses can comply with lower base levels if they change their distribution patterns。

The heating allowance, summer cooling, childcare allowance, one-child allowance are paid directly in cash or in reimbursement, and are not included in the total wage。

For communication and transportation costs read actual cost invoices are issued for work-related communications and transportation, which are not included in the total salary. If changed to a fixed monthly salary payment, it may be considered a wage。

Travel allowance, overtime allowance. An employee who is on mission or does have to eat outside the home, the allowance paid within the prescribed criteria is not taxed or included in the social security base。

Workers ' hardship allowance, family visit expenses。

Staff training, mission building, union statutory benefits (in kind, non-cash shopping cards)

Financial compensation for termination of employment contract, lump sum compensation for injury at work, etc。

Labour protection items, clothing and labour insurance items。

Ii. Optimization of the employment model: to change the nature of labour relations by using the core logic of non- or low-payment of social security contributions, some of them using only employment injury insurance or even non-payment。

Over-age workers. Persons who have reached the statutory retirement age may not be covered by social insurance other than employment injury insurance。

If you are working with a full-time student, you are exempt from social insurance。

Part-time employment. On average, they work less than four hours a day and less than 24 hours a week. For this type of work, an enterprise is required to pay work injury insurance and no other insurance such as old-age pension, medical care, etc。

Services are outsourced to individual households. For example, cleaning, security, design, etc., are awarded to individuals who are registered as individual business owners and are charged for settlement services. This is an operational cooperation between the two main bodies, which has no labour relationship and is completely exempt from social security coverage。

Labour dispatch。

Iii. Rigorous reduction: social security is still due, but the state subsidizes the money directly to enterprises and even to pay tax relief. It's the real money-saving。

Recruitment of persons in difficult employment situations. Women 40 and men over 50 were identified as having difficulties with employment. An enterprise may apply for a full social security subsidy of up to three to five years after recruitment, equivalent to a significant reduction in user costs。

If, for two years after graduation, “deficit students, veterans, etc. Who have not been employed and who have paid social security contributions for a period of more than one year, “retired graduates” “retired students” are entitled to a flat reduction in value-added tax, city construction tax, education fee supplement, enterprise income tax and social security subsidy。

Iv. Coincidentally use the core logic of enterprise annuities and supplementary medical insurance: to provide forward benefits to employees, both of which are explicitly excluded from the current gross wage and do not push the social security base。

Design enterprise annuity. The contribution portion of the enterprise (8 per cent of the total wage of the employee per year) is included in the personal account of the employee, but this amount is not included in the total wage of the employee and does not affect the social security base at all. Staff welfare is strong and business costs have fallen。

Re-establishment of the remuneration structure: the core logic of “move” wages: the social security base is declared at the average wage of the previous year, so that income can be “smoothed” legally。

High transport subsidies are replaced by “private car usage”. The fixed vehicle replacement for employees was replaced by a vehicle rental agreement between the company and the staff to pay for the rental of the vehicle at market prices and an agreement for the cost of fuel, road and bridge to be reported for sale。

Equity incentive. Reductions in monthly wages, allocation of equity share are in return for investment and are not included in social security. It should be noted, however, that there is a tax on the share。

The minimum contributory wage is shown in the wage scale, and other expenses are legally reimbursed。