Mankun's economics doctrine, one of the world's most classic economics introductory teaching materials, is characterized by “common, logical and realistic”, divided into microeconomics and macroeconomics, from individual decision-making to the functioning of the country's economy, creating a complete framework for economic thinking. The book focuses on the core issue of “how to use scarce resources to achieve optimal decision-making” and, through the ten economic principles, is linked to both fundamental theory and a large number of realistic cases, allowing zero-based readers to understand the core logic of economics。

I. Opening building blocks: ten economic principles

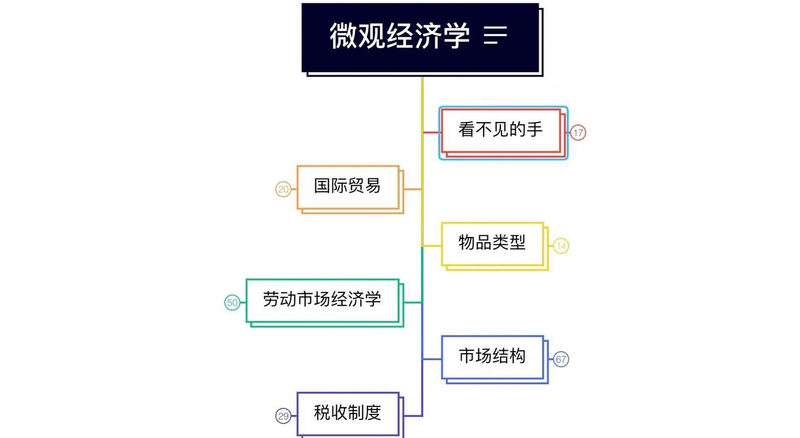

The core starting point of the whole book is the ten major economic principles of mankuntea, which, like the “justity” of economics, cut across both the micro and macro levels and provide the basis for all subsequent analyses, and can be divided into three categories of “market-run” “whole economy”:

(i) at the level of individual decision-making (3 articles), people face trade-offs: economics is essentially a research “choice”, and choice necessarily carries with it a trade-off. For example, an individual cannot buy food by buying clothes from his own income, and a state’s investment in defence reduces spending on education. The contradiction between “efficiency and equity” is typical trade-offs – efficiency seeks to maximize the use of resources, and equity seeks to balance resource allocation, which often cannot be achieved in combination. The cost of something is to get what it abandons (the opportunity cost): it is not only “the money actually spent”, but also “the best option to give up”. For example, the cost of leaving university students to start a business is not only school fees, but also high-paying jobs that may be acquired after graduation; the cost of setting up a factory with idle funds is the interest available to the bank for depositing the funds. This principle teaches readers to assess the rationality of decision-making from the point of view of giving up. Reasonable humans consider marginality: in reality, people's decisions are more of a “division” than a “extreme choice”, “marginality”, which is an “additional unit”. For example, a consumer's decision whether to buy an additional bottle of water depends on whether the “marginal gain” from the bottle is greater than the “marginal cost” (price); or whether the enterprise decides whether to hire an additional employee, depending on whether the “marginal production” (additional output) is greater than the “marginal cost” (wage). Decision-making is optimal when marginal gains are equal to marginal costs. (ii) at the operational level of the market (3 articles), people respond to incentives: incentives are “factors” for changing decision-making, including positive (incentives) and negative (punitives). For example, a government tax on cigarettes (negative incentives) increases the price of cigarettes, leading to fewer purchases by consumers; double the wages paid by enterprises to overtime workers (positive incentives) encourages employees to increase their working hours. One of the core elements of economic analysis is to predict how policy or environmental change can trigger an “incentive response”. Trade makes everyone better: trade is not a “zero-sum game” (a profit-making loss for one party), but a win-win situation through “comparative advantage”. Even if one country is more efficient (absolutely superior) in all production than another, both countries can benefit from trade – for example, the united states is good at aircraft production, china is good at garment production, the united states is focused on airplanes, china is focused on garments, and, in trade, more than “self-sufficient” products can be obtained. This rationale explains the need for globalized trade. Markets are usually a good way to organize economic activity (the “unseeable hand”): adam smith’s “unseeable hand” is a central metaphor of economics – in a market economy, individuals and enterprises make decisions for their own benefit (e. G., business for profit, consumer for effectiveness), but are led by “price signals” that inadvertently promote the overall interests of society. For example, an increase in demand for a particular commodity leads to higher prices, whereby firms proactively expand production (for profit) and ultimately meet consumer demand; falling prices lead firms to reduce production and avoid waste of resources. Manquin stressed that a market economy was more efficient in allocating resources than a planned economy. (iii) at the overall economic level (4 articles) governments sometimes improve market outcomes: “unseeable hands” are not everything, and when markets “market failures” occur, government intervention can correct problems. Common reasons for market failures include monopolization (one enterprise controls the market and raises prices to reduce production), externalities (individual behaviour affects others without compensation, such as factory pollution, which harms the health of the population), public goods (such as defence, street lights, personal use without reducing the use of others, markets are reluctant to provide). Governments could then make market outcomes more equitable and efficient through antimonopoly laws, taxation/subsidies, and the provision of public goods. The standard of living of a country depends on its ability to produce goods and services (productivity): global differences in living standards (e. G. The per capita income gap between the united states and india), the central reason being “productivity” - the quantity of goods and services that work per hour. In high-productivity countries, workers are able to produce more products, enterprises are able to generate more value and the income and consumption capacity of the population is naturally higher. This principle explains why governments focus on education (upgrading the skills of workers), science and technology (researching more efficient machines), infrastructure (reducing the cost of transport for production) - all key to increasing productivity. When the government issues too many currencies, prices rise (inflation): the essence of inflation is that “the supply of money exceeds the real demand of the economy”, leading to currency devaluation and a general rise in prices. For example, if a country increases its currency circulation by 50 per cent in a year, but the total volume of commodities increases by only 10 per cent, surplus currencies will chase a limited number of commodities, leading to an increase in prices of about 40 per cent. Manquin’s historical case, such as the post-world war ii hyperinflation in germany, shows that excessive printing of money could seriously destabilize the economy, and therefore controlling the supply of money is one of the central tasks of central banks. Society faces a short-term trade-off between inflation and unemployment (phillips curve): in the short term, there is a reverse relationship between inflation and unemployment - the government will temporarily reduce unemployment (enterprises expand production and hire more workers) by increasing the money supply (incentives to the economy), but will push up inflation; in turn, reducing the money supply (inflating inflation) will temporarily increase unemployment. This doctrine reminds policymakers that there is no perfect state of “no inflation or unemployment” and that the relationship needs to be weighed against the economic situation (e. G., economic downturns with a focus on reducing unemployment and high inflation with a focus on stabilizing prices). Microeconomics fascicle: focus on “the interaction of individual decision-making with markets”

Microeconomics is subject to “individuals, businesses, markets”, with analysis of how prices determine resource allocation, the main elements of which can be grouped into four main modules:

(i) supply and demand theory: market “core engine”

Manquin explains the supply-demand relationship in a large number of life cases (e. G. Ice cream markets, car markets): the demand curve reflects “the lower the price, the greater the consumer demand” (e. G., the lower the price of ice cream in the summer, the higher the amount of purchases); the supply curve reflects “the higher the price, the larger the enterprise's supply” (e. G., the higher the price of pork, the increased size of the farmers). The supply and demand curve intersects with “balanced prices” - at a time when market demand is equal to supply and resource allocation is temporarily balanced。

At the same time, manquin analyses “non-price factors affecting supply and demand”: for example, increased consumer income increases the demand for normal commodities (e. G. Automobiles) and technological advances increases the supply of goods (e. G. Smart phones); government policies (e. G. Restricted purchases of commodity houses) directly affect demand, and tax revenues affect the cost of enterprise supply. These analyses help readers understand the reality of “why house prices rise” and “why oil prices fluctuate”。

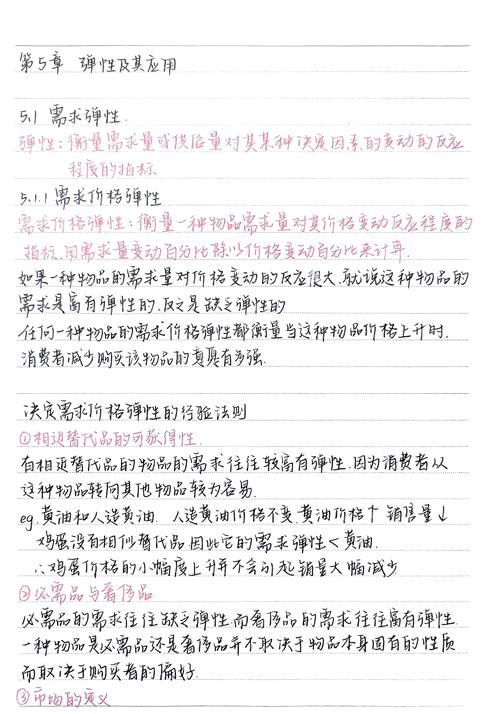

(ii) resilient theory: measure “demand/supply sensitivity to change”

“resilient” is a key tool in microeconomics to quantify “the extent to which changes in one variable affect another”, with demand price elasticity at its core - that is, “the sensitivity of demand to price changes”. For example, the demand price elasticity of medicines is low (price increases, patients still need to buy, demand changes are small) and the demand elasticity of luxury goods is high (price increases, consumers reduce purchases and demand changes are high)。

Enterprises can use flexibility to formulate pricing strategies: for less resilient commodities (e. G. Prescription drugs), price increases can increase total returns; for more resilient commodities (e. G. Sports shoes), price reductions can increase aggregate gains by increasing sales. Governments will also use flexibility to formulate tax policies - taxes on less resilient commodities (e. G. Cigarettes) can increase fiscal revenues and effectively reduce consumption (for tobacco control purposes)。

(iii) market structure: “competition and monopolies” in different markets

Mankun divides markets into four categories, analysing the logic of decision-making by enterprises in different markets:

Full competition markets: large number of enterprises, product homogeneity (e. G. Agricultural markets), enterprises are “price recipients” (which cannot be priced on their own, but sold at market-balanced prices), and in the long run, business profits are close to zero (if there is excess profits, new firms enter, and supply prices are increased). Monopolistic markets: only one enterprise, with no alternatives for products (e. G. Public utility companies), and enterprises are “price-makers” that generate excess profits through “reducing production and raising prices”, when governments need to protect consumer interests through antimonopoly laws or price controls. Monopolization of competitive markets: the number of firms, differences in products (e. G. Garment markets) and competition by firms through “brands, designs” can both generate a monopoly on profits and stimulate product innovation. Oligarchic markets: a small number of firms control markets (e. G. Automobiles, mobile phone industries), there is a “strategy interaction” between firms - one company lowers prices and others follows, which may eventually lead to “price wars” (e. G., competition for value for money in mobile phones). (iv) balance between welfare economics and market failures: “equitable and efficient”

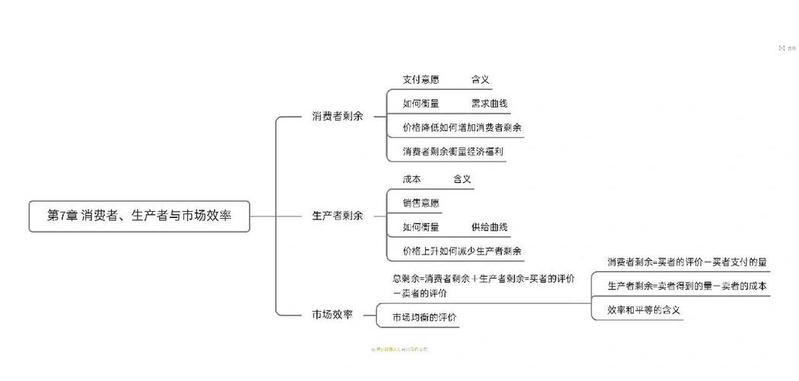

The ultimate goal of microeconomics is to assess whether “market outcomes are fair and efficient”:

Macroeconomics fascicle: focus on “national economic performance and policy regulation”

Macroeconomics is targeted at “the economy as a whole”, with the analysis of the three core issues of “economic growth, inflation, unemployment” and how the government regulates the economy through policy, with three main modules:

(i) macroeconomic indicators: tools for measuring “economic health”

The analysis of the economy begins with a clear definition of “how to measure the economy”, with manquin focusing on three core indicators:

Gross domestic product (GDP): measuring the market value of all final goods and services produced by a country over a period of time (usually one year) is a central indicator of “economic aggregates”. Mankun stressed that GDP only calculates “end product” (e. G. Bread, not flour for bread production) and avoids double counting; at the same time, GDP does not include “non-market activities” (e. G. Domestic work) and “underground economy” (e. G. Black market transactions) and is therefore not a perfect measure of welfare (e. G. GDP growth may be associated with environmental pollution, and the well-being of the population may not increase). Consumer price index (cpi): measuring “changes in the price level of a basket of goods and services purchased by ordinary consumers” is a central indicator of inflation. Mankun explained how cpi was calculated (fixed commodity baskets, prices, comparison period), as well as possible deviations in cpi (e. G. Commodity substitution deviations - consumers turn to low-priced goods when prices rise, but cpi still relies on fixed baskets, resulting in overestimation of inflation). Unemployment rate: measured “the proportion of people who are not working in the labour force but are looking for work”. Mankun distinguishes between “compromising unemployment” (e. G. University graduates seeking work, short-term unemployment), “structural unemployment” (e. G., workers' skills out-of-date as a result of industrial decline, long-term unemployment) and “cyclical unemployment” (e. G., job losses due to job layoffs in an economic downturn), with different types of unemployment being addressed by different policies (e. G., friction unemployment requires improved information on the job market and structural unemployment requires vocational training). (ii) economic growth and volatility: “long-term trends and short-term fluctuations”

The two central issues in macroeconomics are “long-term economic growth” and “short-term economic volatility”:

Long-term economic growth: the core driving force is “productivity growth” (article 8 of the ten principles above), and mankun analyses in detail the factors affecting productivity: material capital (machines, factories), human capital (worker education and skills), natural resources (land, minerals) and technological know-how (production technology). Governments can promote long-term economic growth through policies such as “encouraging savings and investment” (encouraging physical capital), “education for all” (upgrading human capital), “protecting intellectual property” (encouraging technological innovation). For example, japan's rapid economic rise after the second world war, through intensive investment in education and technology, is a typical case of productivity growth. Short-term economic fluctuations (economic cycles): the economy is not growing at a flat pace, but is going through a cycle of “recession (decreased GDP, rising unemployment)” - recovery – boom – overheating.” mankun explains the causes of volatility by using the “total demand - total supply model” (ad-as model): changes in aggregate demand (consumption, investment, government purchase, net exports) or total supply (enterprise production capacity) can lead to economic deviation from long-term trends. For example, in the aftermath of the 2008 financial crisis, us consumers reduced their consumption, firms reduced their investment, and aggregate demand declined, leading to economic recession; and the 2020 epidemic led to business lockouts and a decline in aggregate supply, leading to economic volatility. (iii) macroeconomic policy: governments “regulating the hands of the economy”

When economic fluctuations occur, governments can regulate through fiscal policy and monetary policy, which is the “centre of practice” of macroeconomics:

Fiscal policy: the government regulates the economy through “taxes” and “government expenditures”. In times of economic recession, governments can adopt “extensive fiscal policies” - increased government spending (e. G. Building infrastructure, creating jobs), reduced tax revenues (making more money consumed and invested by residents and businesses) and boosted aggregate demand to stimulate economic recovery; and “restrictive fiscal policies” when the economy is overheated and inflation is high - reduced spending, increased taxes, curbed aggregate demand and stabilized prices. Monetary policy: the economy is regulated by central banks (such as the united states federal reserve, the people's bank of china) through “regulating the supply of money” or “interest rates”. In times of economic recession, central banks adopt “extensive monetary policy” - lower interest rates (lower costs of enterprise loans and willingness to expand investment; lower income from residential savings, more likely to consume); increased currency supply (infusion of currency into markets); and, when inflation is high, “restrictive monetary policy” - higher interest rates, sales of state debt (recovering market currency), lower monetary supply and curb inflation。

Mankun stressed that policy regulation was not “one-size-fits-all”, that there was a “temporal effect” (which took time to implement and could miss the best of times to produce results) and a “side-effect” (such as expansionary policies that could push inflation higher) and that policy formulation needed to be carefully weighed。

Core book values: building “economic thinking”

Manquin’s economics doctrine does not simply teach theory, but rather helps readers to develop a “economics look at the world” way of thinking – to understand the nature of decision-making from “trade-offs” to “opportunity costs” to assess the legitimacy of choices, to analyse market changes from “supply and elasticity” to “policy instruments” to see government behaviour. The book contains a large number of practical cases (e. G., health reform in the united states, economic growth in china, global trade frictions) that allow abstract theory to come to the ground, both as a learning system for teaching materials and as an entry point for a zero-basic reader, as “essential tools” for understanding the functioning of the modern economy。