The first edition of the isp advisory report on the strategic study of market performance patterns and prospects for the potassium hydroxide industry in china, 2025-2031

Summary of the report:

In the first half of 2025, china's potassium hydroxide industry was characterized by “cost-driven price increases, increased supply- and demand-side conflicts, and policy shifts”. On the price side, the domestic price of potassium hydroxide at the end of june amounted to $707 per ton, an increase of 6. 12 per cent over the same period, mainly affected by the sharp rise in the price of potassium chloride for raw materials, which increased by 60 per cent to $3,000-3300 per ton for domestic production and 62 per cent to $3250-3,600 per ton for imports, an increase of 28 per cent over the same period. Potassium chloride, which accounts for more than 50 per cent of production costs, is transported directly downstream by price fluctuations and, although the fall in electricity costs has been moderated by coal prices, the price advantage of concentrated capacity in the north-west still underpins the overall cost curve of the industry. The conflict between supply and demand is particularly acute. In june, the start-up rate in the industry fell to 59. 78 per cent, a decrease of 12. 58 percentage points over the same period, but stock levels rose by 33. 74 per cent to 2. 9 million tons, highlighting weak market demand. There has been a marked decline in demand in the traditional chemical sector, and growth in new and emerging areas, such as new energy sources and medicines, has not been fully offset, resulting in fewer business orders and backlogs. During the same period, import and export data contracted significantly: 4,441 tons in may, a decrease of 74. 31 per cent over the same period; exports of 274,000 tons, a decrease of 23. 48 per cent, and the global slowdown in economic growth further inhibited demand. Policy end speeds up the business shuffle. The system of indicators for the evaluation of cleaner production in the potassium hydroxide industry is being strictly implemented, requiring enterprises to consume less than 1. 2 tonnes of coal/tonne in aggregate for their products, facilitating the withdrawal of backward production capacity and forcing firms to move towards high-end greening. Against this background, leading firms seek breakthroughs through technological upgrading (e. G., national production of electronic-grade products exceeding 70 per cent) and internationalization (construction of plants in south-east asia), while smes face greater survival pressures and are expected to increase industry concentration further。

Current state of industry development:

As the world's largest producer and consumer, china's market for potassium hydroxide has continued to expand and industrial chain structures have been optimized. At the end of june 2025, the price of potassium hydroxide in china was $707 per ton, an increase of 6. 12 per cent over the same period. The price of potassium chloride continued to climb in 2025 and became the main driver of the price increase for potassium hydroxide. The data show that the price of 60 per cent of potassium chloride from domestic production increased to 3,000 to 3300 yuan/t, and that 62 per cent of imports of potassium russian amounted to 3250 to 3,600 yuan/t, a 28 per cent increase over the same period. Potassium chloride accounts for more than 50 per cent of the cost of potassium hydroxide production and is directly transported downstream by price fluctuations. At the same time, while the cost of electricity has been moderated by the fall in coal prices, the north-west is concentrated in capacity and the price advantage still supports the overall cost curve of the industry。

Challenges to industry development:

Increased cost transfer pressure

In 2025, the potassium hydroxide industry faced double pressure at the cost end. With regard to raw materials, the price of potassium chloride rose by 28 per cent in comparison with the same year, the price of potassium chloride exceeded 3,000 yuan per ton by 60 per cent of the national production, and the price of russian potassium imported by 62 per cent amounted to 3250-3,600 yuan per ton, directly increasing the cost of manufacturing by more than 50 per cent of the cost of production. While the cost of electricity has slowed down somewhat as a result of the fall in coal prices, the price advantage of concentrated capacity in the north-west of the region only partially offsets the pressure on raw materials. Data show that the price of potassium hydroxide increased by 6. 12 to $707 per ton at the end of june。

2. Structural imbalances in supply and demand, and stock backlogs highlight weak demand

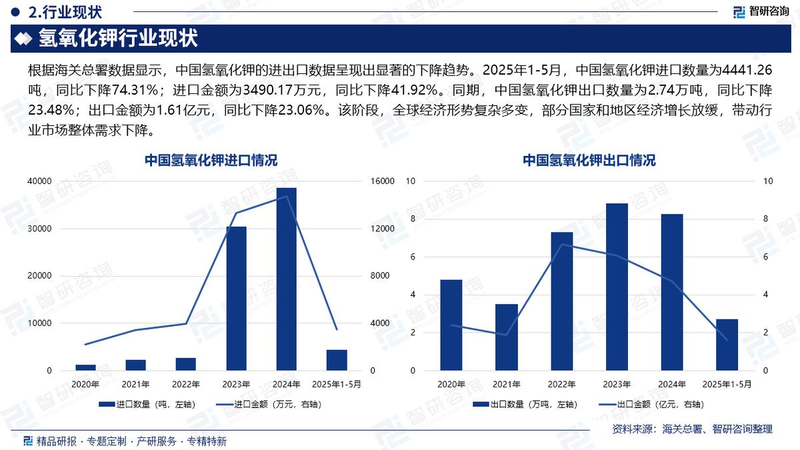

In june 2025, the start-up rate in the industry fell by 12. 58 percentage points to 59. 78 per cent, but the stock volume rose by 33. 74 per cent to 2. 9 million tons, creating an anomaly of “cut-off”. On the demand side, the traditional chemical sector has been affected by the global economic slowdown, and growth in new and emerging areas, such as new energy sources and medicine, has not fully filled the gap; on the supply side, cleaner production policies have pushed out of production capacity, but high-end production has lagged behind, leading to mismatches between supply and demand. Import and export data further confirm weak demand: imports fell by 74. 31 per cent from may to may, exports by 23. 48 per cent and global markets shrunk simultaneously, exacerbating industry difficulties。

3. Policy pushover

The system of indicators for the evaluation of cleaner production in the potassium hydroxide industry is strictly implemented, requiring integrated energy consumption of less than 1. 2 tonnes of coal/tonne per unit product by enterprises, thus facilitating the transition to high-end and greening industries. However, technological upgrading requires substantial capital inputs, such as retrofitting of production lines for electronic-grade products, construction of photovoltaic systems, financing difficulties for smes, and high technical barriers。

4. Inadequate expansion of emerging markets and exposure to risks of traditional channel dependence

Despite significant growth in demand in the new energy sector (e. G. Lithium cell electrolytes, photovoltaic silicon tablet cleaning), the development of new applications by potassium hydroxide enterprises is lagging behind. The decline in demand in traditional chemical and light industries has led to fewer orders, while high market access thresholds in high-value-added areas, such as medicine and food, require long-term processes such as certification and the development of suitable products. Some enterprises, lacking a diversified market layout, over-reliance on a single customer or region, are less resilient to risk when demand fluctuates, and there is an urgent need to open new growth points through technological innovation and outreach。

Based on this, and based on the deep market insight of the research teams in the potassium hydroxide industry under the umbrella of the advisory institute of thought, and taking into account years of research data and first-line operational needs, the advisory institute launched the report on the strategic study of market performance patterns and prospects for the potassium hydroxide industry in china, 2025-2031. Based on a new perspective on potassium hydroxide, the report focuses on the core issues of the industry — changing trends (how to change), user needs (what to want), investment choices (where to go), operating methods (how to go) and practice cases (see below) — and looks forward to working with industry partners to develop new patterns and opportunities for the industry to promote the development of the potassium hydroxide industry. In the field of potassium hydroxide in deep-farming china for more than 10 years, ziro is willing to work with industry enterprises to provide effective information, professional advice and customized solutions to help sustain the potassium hydroxide industry。

Relevant information in the report:

Based on the most up-to-date and complete chinese industrial chain data, the report on the strategic study of market performance and prospects for the potassium hydroxide industry in china, 2025-2031 integrates authoritative official statistics, in-depth business research, capital market insight and global information, and is validated through rigorous smart processing and exclusive algorithms to ensure that analytical findings are highly reliable, transparent and traceable。

For 15 years, isp has been specialized in industry consulting and is a specialized service in the field of industrial consulting in china. Companies branded “information-driven industrial development, enabling firms to invest in decision-making”. Professional industrial advisory services are provided to enterprises. The main services include quality studies, tailor-made, monthly topics, market status certificates, specialized new declarations, researchable reports, business plans, industrial plans, etc. Regular reports and customized data are provided, including weekly/monthly/quarterly/annual reports, covering policy monitoring, business dynamics, industry data, business ranking, product price changes, investment finance overviews, market opportunities and risk analysis。