“99 yuan package mail” “cross-border direct mail includes a tax price” — every time a net purchase is made, do you wonder: is there a tax in the price other than the value of the commodity itself? In fact, whether it's for snacks, electricity hoarding in kyoto or make-up by skycat international, tax revenues are already “invisible” in the amount of payments. Today, it is being broken down in plain language: where does the tax on internet purchases lie, how does it count, and where it is tax-free。

I. Domestic internet purchases: tax collections in “prices”, paid by businesses on your behalf

You usually buy domestic goods on a pedestal and kyoto platform, and you pay value added tax - this is the central tax on the flow of domestic goods and the most hidden “hidden tax”。

A key rule is first understood: vat is “off-the-shelf tax”, but merchants will include it in the final sale price. For example, you spend $100 on a case of milk, which appears to be paid in full, with about $11. 5 of value added tax (calculating logic: 100 ÷ (1+13%) x 13%, and 13% of value added tax on goods in general). The tax is not on a separate payment page, but is regularly reported to the tax authorities after it is collected by the merchants, which is equivalent to the indirect payment of taxes on goods。

Vat rates vary between commodities, and daily consumption is common:

- general goods such as food, clothing and electricity: 13%

- living services such as catering, accommodation, etc. (e. G. Takeout): 6%

- cultural products such as books and newspapers: 9%

For consumers, the tax is not to be calculated and paid separately, but it is to know that the price at which you see it is already the sum of the original commodity price plus value added tax. In the case of small businesses (small-scale taxpayers), according to the ministry of finance's general tax administration bulletin no. 19 of 2023, there were also concessions by the end of 2027 — goods subject to a 3 per cent collection rate are now taxed at 1 per cent, and vat is also exempt from monthly sales of up to 100,000 (within 300,000 quarterly), which is one of the reasons why many low-value small goods remain profitable。

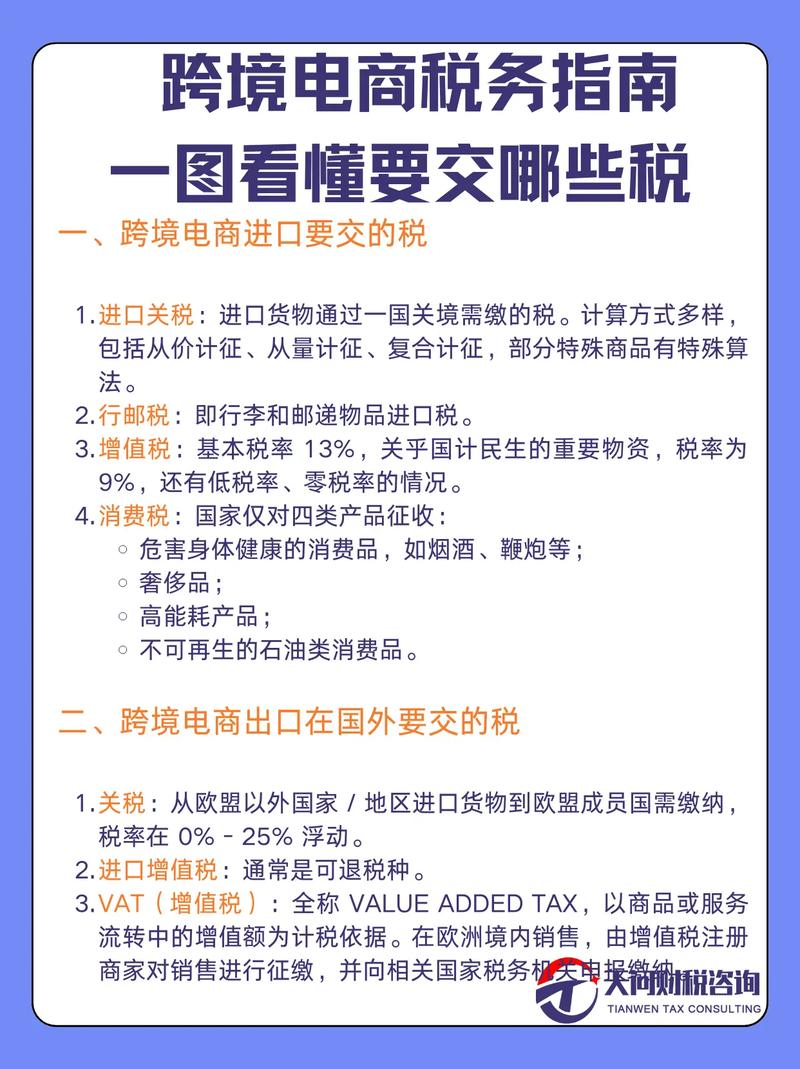

Cross-border internet purchases: the tax is clearly “listed” and there are limits to the amount

If imported goods are purchased from platforms such as skycat international and the kaura sea buy, the tax will not be “hidden” — usually a separate “tax and fee” item will be shown on the order page and will be paid directly by you. The core of this tax is the combined tax rate for cross-border electric operators (including tariffs, import chain value added tax, some goods including excise tax) and not a simple supercharge, but a preferential tax set by the state (below the general trade rate)。

The “tax exemption” for cross-border net purchases is to be firmly recorded

In order to facilitate individuals ' cross-border purchases, the state has established clear transaction limits (financial duties (2018) 49):

- single transaction limit: $5,000 (not exceeding $5,000 for one purchase, taxed at the combined rate of cross-border electrician)

- annual transaction limit: $26,000 (total value of imported goods purchased on all cross-border electrician platforms within a year, not exceeding $26,000)

If a single purchase exceeds $5,000, but does not exceed the annual limit of $26,000, and only one item of the order can be purchased from a cross-border electricity provider, subject to full taxation at the general trade rate; if the total amount is over $26,000 per year, the tax burden will increase significantly as a general trade method。

2. What are the taxes and fees? Two common examples

Cross-border net purchases are taxed at the “cross-border utility combined rate”, which is easier to calculate, with different rates for different commodity categories, depending on the latest customs standards:

- example 1: purchase of japanese skins (us$ 500 at tax price and us$ 23. 05 per cent at the combined rate of cross-border electric generators)

Actual taxes = 500 x 23. 05 = $115. 25 (final payment = $500 + 115. 25 = $615. 25)

- example 2: purchase of french perfume (1,000 yuan at tax price and 47 per cent at the combined rate of cross-border electric generators)

Actual taxes = 1000 x 47% = $470 (final payment = 1000 + 470 = $1470)

Can refunds be made? Yes

If the cross-border goods purchased are not returned satisfactorily, the amount of the tax paid will not be collected and your annual transaction amount will be restored if the goods are returned within 30 days of the release of the order and the goods are returned to the original customs control site within 45 days (official gazette no. 45 of 2020 of the customs administration). If you want to check your tax records, you can also find them through the “hand over customs” app or the china single window for international trade。

There are two other special cases: exemption from taxation and “no separate collection of taxes”

In addition to cross-border electrical power platforms, the direct return of goods from overseas mail (e. G., gifts from relatives and friends) is subject to tax (official gazette no. 43 of 2010): customs will, in accordance with the law, determine the price of the goods, then calculate the import duty, which is waived for less than 50 yuan (including 50 yuan); and the full amount of more than 50 yuan is payable and is not charged directly at the individual declared price. For example, the post-validation tax on goods sent by mail amounts to $45, which is not paid; if it is $60, it is paid in full。

Live delivery: tax collection at “off-the-shelf” lee

The logic of taxation is the same as that of regular internet purchases in the current popular live broadcast of goods, whether they are domestic or imported: value-added tax on domestically produced goods is included in the price mark, and taxes on imports are separately identified. It should be noted that the electronics platform transmits to the tax authorities information on the identity and income of merchants, anchors, and ensures that the tax is paid in accordance with the law (official gazette no. 194 of 2018 of the customs administration), so that there is no “deficit” in the formal broadcast of goods。

Iv. These networks buy faulty tax areas. Don't step on them

“pay mail = tax exemption”? Wrong! The chartered mail is only the merchants bear the freight, and the value added tax on the goods themselves is still included in the sale price and will not be exempted from the chartered mail。

“cross-border goods over $5,000 are also worth the money”? No! After the single limit of $5,000, the tax would have to be based on the general trade rate, the tax burden would have increased significantly and there might be “an additional $100 for the purchase of goods and several hundred more for the payment of taxes”。

“personal declaration of a low price by mail is exempt”? No, the customs service will determine the tax price in accordance with the law, and concealment of a failure or false declaration may lead to the seizure of the goods。