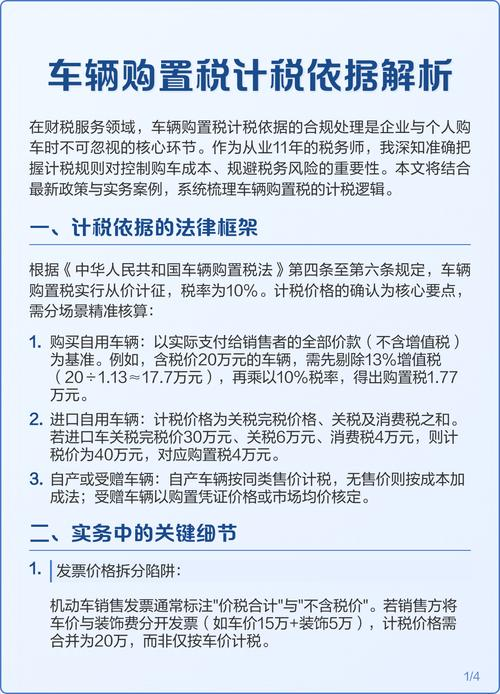

Q: what is the calculation of the taxable tax on the acquisition of vehicles?

Response: taxable amounts for vehicle acquisition tax are calculated on the basis of taxable vehicle prices multiplied by tax rates. The formula is:

Taxable = taxable price x 10 per cent

The taxable price is determined in accordance with the following provisions:

(i) the taxable price of the taxpayer's own taxable vehicle, the full price actually paid by the taxpayer to the seller, excluding vat

For example, li qun purchased a sedan, the “total price tax” on the unified invoice for the sale of motor vehicles was $226,000, the “tax-free price” was $200,000, the “value added tax” was $26,000, the total price actually paid by the taxpayer to the seller in this case was $200,000 and the tax payable was 20 x 10 per cent = $20,000。

(ii) the taxable price of the taxpayer's own vehicle imported for tax purposes, plus customs duties and excise duties for the price of customs duties

For example, an enterprise buys a car for its own use from abroad, pays customs duties of 75,000 yuan for customs imports, pays excise taxes of 125,000 yuan, and the customs import duty contribution notes a tariff completion price of 300,000 yuan. When the enterprise taxed the vehicle acquisition tax, the vehicle acquisition tax price of the imported vehicle = the tariff value (0. 3 million yuan) + customs duty (755,000 yuan) + excise tax (125,000 yuan) = 500,000 yuan and the vehicle acquisition tax payable is 500,000 yuan x 10 per cent = 50,000 yuan。

(iii) the tax price of the taxpayer's own taxable vehicle is determined on the basis of the sale price of the taxpayer's own taxable vehicle, excluding vat

(iv) the taxpayer obtains, by gift, award or otherwise, the taxable price of his own vehicle, which is determined on the basis of the price specified in the certificate at the time of acquisition of the taxable vehicle, excluding vat tax。

Source: platform for tax service 12366