New second house trading tax rules 2026

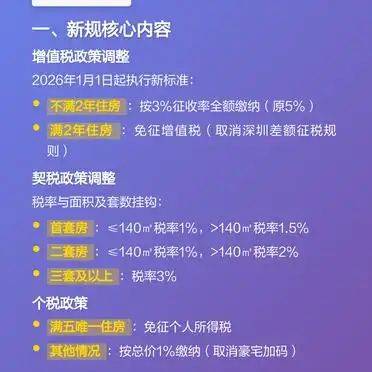

I. The new core context

Vat policy adjustments

Since 1 january 2026, the vat policy for the sale of housing by individuals has implemented new standards:

Housing under 2 years: full vat at 3% rate (previously 5%)

2. Housing up to 2 years: vat exemption (elimination of shenzhen's original rule of tax on non-ordinary housing differences)

Tax adjustments

Tax rates are linked to the size and number of homes purchased:

1. First flat: 1 per cent of area 140 m2 tax and 1. 5 per cent of area > 140 m2 tax

2. Two housing units: 1 per cent of the 140 m2 tax and 2 per cent of the 140 m2 tax

Three sets and above: 3 per cent tax

Tax policy

1. Single housing of five: exemption from personal income tax

2. Other cases: 1 per cent of the total price (no more house plus code)

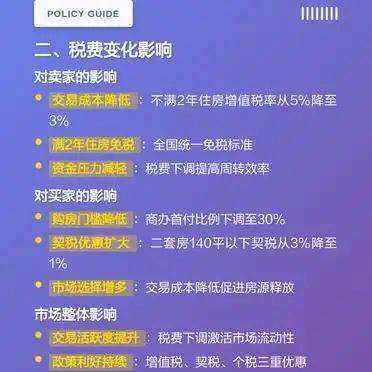

Impact of tax and tax changes

Impact on sellers

1. Reduction in transaction costs: the value added rate for housing has been reduced from 5 per cent to 3 per cent for less than 2 years, equivalent to a direct discount of 60 per cent

2. Up to 2 years of housing tax exemption: elimination of tax rules on former differences and national harmonization of tax exemptions

Reduced financial pressure: lower taxes and fees directly reduce sales costs and improve liquidity efficiency

Impact on buyers

1. Lower threshold for house purchases: lower down to 30 per cent for first-instance commercial products and significantly lower threshold for purchases

2. Expansion of tax concessions: reduction of the tax rate of up to 140 flats for two apartments from 3 per cent to 1 per cent and significant reduction in expenditure on home purchases

3. Increased market choices: reduced transaction costs to facilitate the release of housing sources and increase market choice space

Overall market impact

1. Increase in transaction activity: lower taxes and fees directly reduce transaction costs and activate market liquidity

2. Policy gains are good: value added tax, tax dues, triple tax preferences form policy combinations

3. Anticipated improvements in markets: policy adjustments have given positive signals and increased market confidence

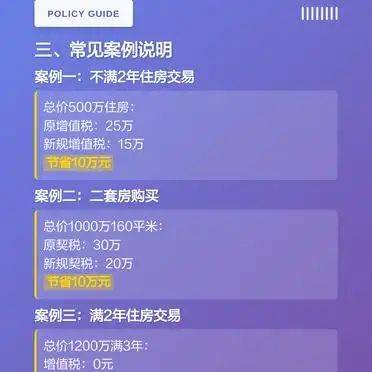

Iii. Description of common cases

Case i: housing transactions for less than two years

A total cost of 5 million housing units, holding less than 2 years:

Original vat: 5 million x 5 per cent = 250,000

New vat: 5 million x 3 per cent = 150,000

$100,000 in savings

Case ii: purchase of two suites

A total cost of 10 million two rooms covering 160 m2:

Original tax: 10 million x 3 per cent = 300,000

New deed tax: 10 million x 2 per cent = 200,000

$100,000 in savings

For a total cost of 12 million dwellings, held for three years:

Value added tax: zero (exempted)

Tax: 0 yuan (1 per cent tax on non-exclusive housing)