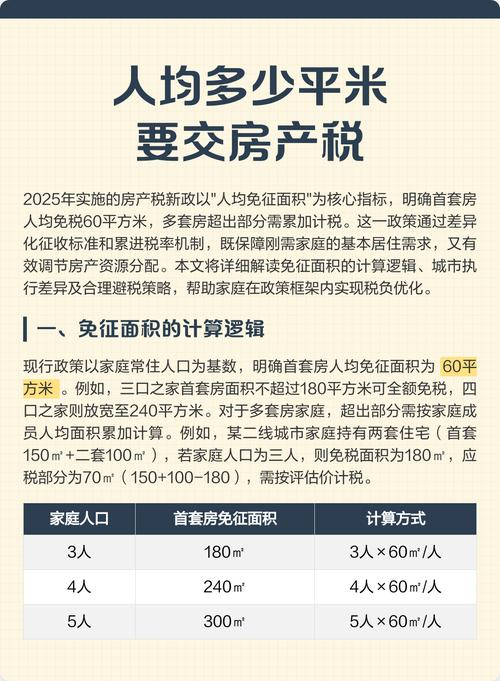

The introduction of real estate taxes must be based on an objective assessment of the value of the house, a clear delineation of land titles and entitlements to house occupancy and the establishment of an accurate housing information system。

The social welfare institute recently published the china housing development (medium 2016) report, which states that first-line cities and some hot-spot second-line cities need to increase their supply, implement rehousing on the basis of commercial rehousing, and introduce a system of parking and land auctions. At the same time, the report recommends seizing the current opportunity to introduce real estate taxes in first-line and hot-spot second-line cities。

Speeding up the pace of real estate tax legislation, which was presented at the 18th plenum iii, is still in the drafting stage. Although it has been more than five years since shanghai and chongqing introduced a real estate tax, it has not proved to be as effective as expected in terms of increasing market supply, flatting housing prices and adding stable taxes to the local level, in some areas with tax costs or even equivalent tax revenues。

This is due, on the one hand, to the fact that the high and low housing prices are clearly linked to the land system, the household registry system, the availability of money up to regional differences, and that the mere imposition of a single tax does not allow the price of housing to be delinked from these macro factors, leading to the price of housing and market supply, and, on the other hand, to the fact that a legal property tax on property is still subject to further explanation in order to be complete. In the case of land ownership, the purchase is in fact the ownership of the house and the tenancy of the land and does not have full property rights. In policy terms, unlike the shanghai-chongqing pilot introduction of a “property tax”, it was included in the legislative plan. This also means that future real estate taxes will be levied not only on the value of houses but also on land. There is, however, no clearer legal expression of the right to land rental, as consumers have paid land concessions at the time of purchase, which can be considered as rents for land use rights, and other taxes related to the area of the purchase of land also include the payment of land rents. The imposition of a real estate tax of a full property nature after the payment of the rent of incomplete title is tantamount to double taxation. To avoid this challenge, jurisprudence must be more comfortable。

From this point of view, the introduction of real estate taxes must be based on an objective assessment of the value of the house, a clear delineation of land ownership rights and interests in the occupation of the house, and an accurate housing information system, in order to truly achieve the objectives of taxing the law, regulating the gap, paying taxes, etc., and obtaining as much understanding and approval as possible from the general public to local governments。

It may be argued that the conditions for the introduction of real estate taxes are premature in terms of current hardware and software preparations. This is why the real estate tax, although classified as a category i legislative item, is not formally on the agenda. Indeed, in the light of the current economic situation and regulatory requirements, the introduction of real estate taxes also requires caution. The fact that real estate goes to stock requires that the market maintain a certain level of trading activity, and that real estate taxes are introduced when conditions are not ripe, may reverse market expectations and make it more difficult to remove stocks. Moreover, the introduction of real estate taxes in first-line and hot-spot second-line cities, for reasons such as development disparities, does not lead to crowding out effects that shift home buyers to heavily stocked third-line cities. Nor would it be better to use administrative leverage than to flatten the prices of first- and second-line urban housing. If developers were to turn to cities on the 3rd and 4th lines in order to circumvent risk demand, this would only result in a higher stock of cities on the 3rd and 4rd lines and more expensive houses, blocking the way to the city for new citizens。

The idea of a real estate tax can be heard from time to time, however well-founded it may be, it must not be forgotten that the real estate tax is designed to adjust the land system, fiscal relations and social distribution in the mainland, rather than to become a temporary market regulation tool。