At present, the chinese economy has entered an era driven by “modern services” and “large markets for domestic unification”. In terms of the structure of the economy, the sectors of imports, outward investment, services, etc., are well over-represented in the size of the economy, both export and import substitution sectors. According to rough estimates based on data on employed persons in 2025, the share of employment in services alone is nearly 50 per cent, while the share of the beneficiary group is over 60 per cent of total employment, added to other sectors that favour currency appreciation, while the share of employment in the traditional manufacturing sector, which is directly dependent on exports and facing strong import competition, is less than 40 per cent. There is a pattern between six and four and between three. Under this structure, the moderate appreciation of the renminbi can bring about net gains by reducing import costs, boosting the real purchasing power of the population and promoting the development of services, with relatively manageable pressures on the export sector. Even without taking into account internal preferences in the export sector, macroeconomic gains such as modest domestic demand boosted by the renminbi's appreciation, lower production costs, wealth effects for the population and increased welfare effects are significantly greater than the pressures on sectors such as exports and have a more positive impact on the overall economy。

Export structure “shock relief”

Even within the export sector, there are structural differences in the real impact of the renminbi appreciation. In general, traditional labour-intensive industries such as textiles, clothing, boots and toys are extremely sensitive to exchange rate fluctuations because of their high product homogeneity, low technical barriers and availability of alternatives, and their international competitiveness is highly dependent on price advantages. The renminbi's appreciation will reduce its modest profit space directly, and there is real pressure in the short term to lose orders to low-cost areas such as south-east asia。

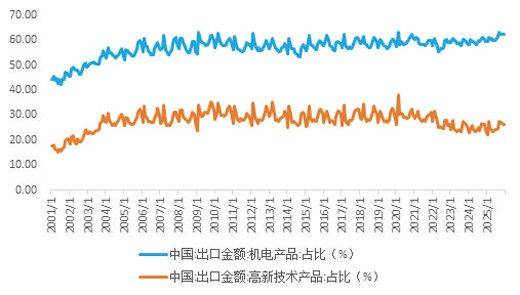

However, the situation is quite different for high- and middle-end manufacturing industries. With the acceleration of technological innovation and industrial upgrading in china, the share of electrical and electrical products, new energy vehicles, ships, high-end equipment and high-technology products in total exports has surpassed historical levels and has become a “blast rock” for chinese exports. According to data from the general customs administration, in 2025, more than 60 per cent of all exports were made up of electromechanical products and more than one quarter of all exports were made up of high-technology products. These products build unique non-price competitive advantages based on chain efficiency, barriers to technological innovation and brand premiums. The dependence of global buyers on china's supply chain has shifted from mere “low-cost procurement” to “high reliability and technological synergy”, leading to a significant reduction in the price elasticity of its export demand and a lower sensitivity to exchange rate fluctuations。

Increasing share of exports of electromechanical and high-technology products

Even if the moderate appreciation of the renminbi results in a corresponding increase in foreign currency prices, overseas clients often have to accept price adjustments or cost-sharing because of difficulties in finding alternative suppliers of the same size, quality and delivery capacity in a short period of time. Added to the growing number of firms in the middle and high-end manufacturing industries, there has been a marked improvement in profitability, effectively segregating exchange rate risk through global layout, cross-border renminbi settlements and financial derivative hedges. Thus, the optimization of the export structure provides, in essence, a growing “shock-mitigator” for the renminbi exchange rate. Not only has the moderate appreciation of the renminbi not triggered a collapse in exports, it has forced inefficient production capacity, boosted the concentration of resources into high-value-added chains, contributed to the growth of medium- and high-technology-intensive export industries, and accelerated china’s structural leap from a “trade power” to a “trade power.”。

Exchange rate non-export critical

Exchange rates are only one of many variables affecting exports and are not decisive. The rise and decline of export trade ultimately depends on the combined effects of global demand trends, domestic foreign trade policies, the development of domestic high-technology technologies, core manufacturing competitiveness, the integrity of industrial chains, and the structure of export commodities. Exchange rate fluctuations can only be a complement to regulation, making it difficult to dominate export trends, and possibly even a gradual reverse。

From china's development experience over the past two decades, there is no strong trend correlation between the rise in devaluation and exports. For example, in the first decade of accession to the world trade organization (wto), the renminbi showed rapid appreciation, but china's exports continued to grow at an average annual rate of 21 per cent, indicating that the renminbi's appreciation did not have a significant impact on export growth. After that, between 2011 and 2020, the exchange rate of the renminbi was relatively stable, but export growth slowed. After 2020, china's foreign trade showed a more pronounced competitive advantage and resilience in the whole industrial chain, and the impact of exchange rate fluctuations on exports declined further. Even against the backdrop of the strengthening of the renminbi in 2021, chinese exports continued to grow by about 30 per cent over the same period, with a trade surplus of $67. 64 billion, significantly exceeding market expectations。

There is no strong correlation between the rise/depreciation of the renminbi and exports

After the second term of office of united states president trump in 2025, trade protection measures such as “reciprocal tariffs” “pentanyl tariffs” were imposed on china, but chinese exports continued to achieve the more than expected “reversion”. In dollar terms, china's exports grew by 5. 4 per cent cumulatively in 2025, significantly exceeding market expectations; however, between the beginning of 2025 and mid-april 2026, the offshore renminbi appreciated by nearly 7. 0 per cent against the united states dollar, while the median exchange rate of the renminbi appreciated by some 4. 6 per cent against the united states dollar. There are two specific and direct reasons behind this “reverse”: the increasing diversification of export markets, with a sharp increase in the share of the south countries of asean, africa and latin america and a decline in the share of the united states and europe to about 25 per cent; and the higher value-added electromechanical and high-technology products, which account for about two thirds of total exports and are increasingly becoming “combating stones” for china's exports. In the future, as china accelerates its science, technology and innovation and industrial upgrading, the science and technology content and international competitiveness of exported commodities will increase, and more and more enterprises will have the capacity to use derivative instruments to avoid exchange rate risks, and exports will be further weakened by exchange rate fluctuations。

It's not necessarily good to lose value

In turn, the devaluation of the currency may not be conducive to stimulating exports and boosting the economy. The traditional “j-curve effect” and the “marshall-lerner terms” lead to the conclusion that “depreciated exports are good” based on the implicit premise that a country's exports are almost non-dependent on imported inputs, assuming that they depend solely on its own domestic factors (labour, land, indigenous raw materials, etc.), and that imports are used only for final domestic consumption and do not interfere in the production chain. Under this closed production scenario, the devaluation of the currency would translate directly into a decline in the price of foreign currency for export products and an increase in the price of consumer goods imported, with the effect of export expansion and import contraction. In other words, the result of the devaluation of the currency is simply equated with “lower export costs” and “higher import thresholds”。

However, in light of the current deep division of labour in global value chains (gvcs), modern export industries are highly dependent on global resource allocation and intermediate imports (e. G. Spare parts, raw materials, technology authorizations, etc.). The wto global value chain development report shows that gvc trade (which involved two cross-border trades) accounted for 46. 3 per cent of global trade in 2023. The organization for economic cooperation and development (oecd) trade value added assessment (tiva) statistics also show that, although the backward participation of chinese exports (i. E. The share of imported inputs used in exports) declined significantly from 28. 2 per cent in 2000, it still stood at 16. 2 per cent by 2020. As a result, the relevant assumptions of the traditional theory are no longer valid。

Gvc trade as a share of global trade, 2018-2023

On the contrary, the depreciation of the currency may also have a “cost offset” effect — a sharp rise in the cost of imported parts and components, leading to a substantial increase in the cost of production of the final product, thereby offsetting the price advantage of exchange rate depreciation. Not only are exporters unable to increase competitiveness through reduced prices, but they may even lose their original advantage because of the high cost of imported raw materials or spare parts, as has been the case in recent years in countries such as japan, korea and turkey. At this time, devaluation not only does not lead to export expansion and domestic economic prosperity, but also exacerbates the pressure on manufacturing operations, worsens the terms of trade and ultimately reverses economic growth。

In the first quarter of 2026, china's imports grew significantly by 22. 7 per cent, significantly exceeding the 14. 7 per cent increase in exports during the same period, particularly in march, when the rate of import surged further to 27. 8 per cent. In terms of categories of imported commodities, imports of raw materials such as iron ore, copper ore, crude oil and high-technology intermediates, represented by high-end integrated circuits, show relatively rapid growth. Against the backdrop of escalating geo-conflicts in the middle east and shocks to global supply chains, the continued devaluation of the renminbi would entail higher import costs for the firms concerned; on the other hand, moderate appreciation of the renminbi would help to smooth down the associated import costs。

Global lessons learned

From global experience, there is no simple linear causal link between exchange rate movements and macroeconomic performance. It has been amply demonstrated that devaluation does not necessarily boost the economy, and that a disorderly collapse may accelerate the outbreak of the crisis; a moderate and orderly appreciation of the currency, against the background of macro-conditions, can well go hand in hand with steady economic growth. The ultimate effect depends on the drivers of devaluation or appreciation, the magnitude and the resilience of the domestic economic structure。

In negative cases, some emerging market countries are caught in a vicious cycle of hyperinflation, debt default, and economic collapse as a result of a lack of foreign exchange reserves, high external debt, a single economic structure, and a cumulative capital flight shock. For example, during the asian financial crisis in 1997, the sharp devaluation of currencies such as the thai baht led to the collapse of businesses, bank failures and a deep economic recession in the short term; in recent years, turkey and iran's domestic currency have continued to collapse, leading to soaring import costs, a sharp increase in the external debt burden, high inflation, a significant contraction in the purchasing power of residents and a prolonged stagnation。

Conversely, there are few cases of steady economic growth in the context of currency appreciation, often driven by industrial upgrading and domestic demand, as evidenced by countries such as germany and singapore in the late mid-century. Despite the appreciation pressures of mark and new zealand dollars, these countries have succeeded in transforming cost pressures into technological innovation engines, with strong high-end manufacturing and modern services core competitiveness, to drive industries up to high value added; at the same time, currency appreciation has reduced import costs and increased the real purchasing power of the population, thereby effectively stimulating domestic demand consumption and services development. In addition, strong currencies can increase international investor confidence, attract long-term stable capital inflows and provide ample financial support for economic transformation. For example, between 1950 and 1973, the united states dollar and the deutsche mark (dm) moved from 1. 2. 2 to 1. 1. 37, with the german mark appreciated by 67 per cent, while the economy of the federal republic of germany remained at an average annual rate of 5 to 7 per cent during the period; singapore, aided by the appreciation of the current currency, achieved a per capita GDP leap of between us$ 10,000 and us$ 20,000 over a period of five years (1989-1994) and more smoothly achieved a sustained leap of us$ 95,000 per capita GDP over the next 30 years。

Accompanying appreciation

The chinese economy is in a growth pattern that is driven by technological progress, industrial upgrading, foreign capital inflows and domestic demand, and the renminbi is supposed to enter a period of moderate appreciation under two-way fluctuations. Technological innovation has contributed to a significant leap in the productivity of new quality, leading to a sustained increase in the technical content and value added of export products and to the optimal upgrading of the structure of the export sector. The appreciation of the renminbi has reduced the cost of imports and increased the real purchasing power of the inhabitants of the country, thereby effectively stimulating domestic demand and consumption for development. At the same time, the moderate appreciation of the renminbi has helped to raise the international value of the renminbi's assets, attract sustained inflows of external capital and give impetus to domestic industrial transformation and domestic demand development. Thus, industrial transformation, domestic demand development and foreign capital inflows resulting from a reasonable appreciation of the renminbi are urgently needed for china’s economic development。

From a national strategic perspective, building a financial power is an important task facing china in the “155” and longer term. The construction of a financial power requires not only the development of a modern financial system with chinese characteristics, based on the renminbi, but also a reasonable level of currency exchange。

From the history of the development of international financial centres, it would not have been possible to form a world-class international financial centre if the currency had not remained strong over a considerable period of history. The rmb exchange rate level should be based on a demand-for-supply relationship, while it is also necessary for the monetary authorities of a country to choose favourable exchange-rate policy objectives for achieving economic and financial development。

Over the past decade, the renminbi has objectively been justified by a moderate appreciation, both in terms of the level of economic growth, balance of payments and inflation levels, and has been subject only to continued pressure from the united states, with the exchange rate coming under greater pressure. In the coming period, the renminbi has shown a moderate and gradual appreciation, both logical and significant。

Policy support for transformation

The government can play an active lead role as a “night watchman”. It is undeniable that, in the process of appreciation of the renminbi, part of the transition to a more slow upgrading of traditional manufacturing industries, particularly small and medium-sized enterprises in related industries, will inevitably be affected. Such enterprises, which generally suffer from low profitability, weak risk resistance, lack of experience in exchange-rate management and a single source of financing, are highly vulnerable to loss of profit margins, loss of overseas orders and even business difficulties, thus affecting industry stability and employment。

In response to the above, in the context of the appreciation of the renminbi, the relevant authorities and local governments could establish a regularized monitoring mechanism, conduct dynamic monitoring, field research and precision assessments of the affordability of enterprises in a timely manner, and establish a “last kilometre” of policy to minimize the negative effects of appreciation. On the one hand, financial institutions can be combined to provide specialized training and home-to-door guidance to encourage and direct exporting enterprises to use foreign exchange finance instruments such as forward closings, foreign currency swaps, export bonds, insurance financing and formal financial derivatives for exchange rate risk management, to help enterprises to pre-lock exchange rate risks, stabilize operating costs and address individual concerns. On the other hand, targeted financial support, tax relief, fiscal subsidies, export rebates and other relief initiatives, such as those targeting labour-intensive industries, msmes and hard-to-reach workers affected by exchange rate movements, can optimize credit approval processes, reduce financing costs and effectively ease corporate financial pressures, thereby stabilizing business expectations and market owners ' confidence and facilitating the steady transformation of traditional manufacturing industries。

In sum, the moderate appreciation of the renminbi, driven by the basics of supply and demand in the market, rather than by the malicious exploitation of speculative capital, is a corollary of china’s economy’s progress to a high-quality stage of development and the construction of a financial power, a sign of its maturity in internationalization and one of the best solutions to the former chinese economic performance. The moderate appreciation of the renminbi needs not to be overly worrying, let alone “upgrade” changes, but rather to be objective and rational in order to channel market expectations from a symmetrical and confident strategic fixation, to boost the smooth transition of chinese exports from “exchange-rate-sensitive” to “value-driven” growth, to accelerate progress in science and technology and industrial transformation, and to strengthen domestic demand and consumption。

(senior research fellow, international financial research institute, forum of chief economists, liu tao; director, international financial research institute, forum of chief economists, changping department)