As the two-line cities became more crowded and markets became saturated, some of the allies aimed their eyes at the three-line cities in an attempt to dig up increases through the layout of the sinking market。

According to data from the china facilitation shop development report, 2023, the number of convenience stores in the country grew from 130,000 in 2019 to 300,000 in 2022 and is rapidly sinking into cities on the 3rd and 4th line。

However, the commercial model of the convenience store is difficult to reconcile with the life habits of the three- and four-line urban consumers. The profits of the convenience stores are derived mainly from fresh food products, with the core group of guests depicting fast-paced urban white collars who quickly meet consumption needs, such as three meals a day, near the writing building。

The slow pace of cities on the 3rd and 4th line makes it difficult to cultivate the habit of eating in convenience stores. According to “bookshops”, an associate runs a convenience store in a county town in hubei province, which invests 500,000 dollars, with a daily turnover of $3,000 sufficient to secure the capital, but in fact runs for six months, with a daily turnover of only $1,000。

On short video platform, a consortium of 7-eleven guangzhou stores stated that he had invested $500,000 in option c, that the shop was located below a writing building in guangzhou, that it operated 8,500 yuan a day from monday to friday, 6,000 yuan a week, and around 240,000 a month, but that the profit of a month was less than 6,000 yuan, less the cost of branding, rent, utilities, bad goods and labour costs (6). He added, however, that since only seven months were currently available, there was much to improve and there was room for growth in future turnover。

In general, the threshold for entry into a convenience store is not only high investment costs and long cycles, but also high capacity requirements for those joining it, as well as the need for the full input of the operator, which increases investment risk。

It has become the norm for the industry to close its doors and open its doors. However, small and medium-sized entrepreneurs who expect to be able to return to their homes quickly are not friendly, and caution remains to be exercised in joining the convenience stores。

02 brand strength

Brand strength is judged primarily by brand history, the size of the shop and brand volume。

7-eleven, a 100-year-old convenience store brand, was created in 1927 by the united states southern continental ice corporation; in 1964, 7-eleven introduced a licensing system, thus opening the way for its expansion in the united states and the global market。

In 1973, yofa hall, ito, japan, signed a regional concession association agreement with the united states southern corporation and opened its first 7-eleven convenience store in tokyo, japan, in the following year; the total number of doors in 1990 was 4,000。

At the same time, southern united states companies were in trouble and applied for bankruptcy in 1991 owing to the failure of diversification and competitive pressures in large shopping malls and discount shops. The ito yohua hall had not hesitated to purchase 73 per cent of the shares and became the largest shareholder. Subsequently, in 2005, the new holding company “seven & i holdings” was established in ito yohua hall, which centrally manages the ito yogo hall, 7-eleven inc. And 7-eleven japan in the united states, and completed the acquisition of the full ownership of 7-eleven inc. In the same year, making the united states company a fully funded subsidiary。

Since then, 7-eleven has accelerated the pace of global expansion, but its story of “emerging growth” in the chinese market has been delayed。

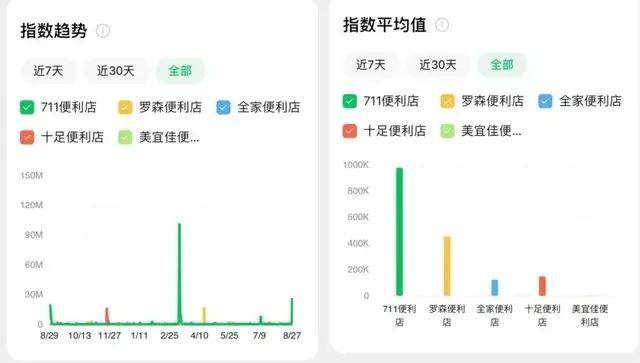

According to " top100 2023 chinese convenience store " , published in 2024 by the china chain operators association, zhongqing (china) investment ltd. Ranked seventh out of 3906 stores, behind rosen's convenience store, which also originated in japan, and rosen's investment ltd. Ranked fifth out of 6330 stores. There is a difference of almost 2,000 in the number of shops。

Figure source: china chaining association

The micro-credit index shows that 7-eleven still has the highest brand volume. This suggests that the size of the door shop and the crowding of consumers are not mutually reinforcing, but rather that the smaller the door shop, the more likely it is to generate a “scarce feeling” on the side of the consumer and trigger a desire to taste。

This data is also confirmed by the fact that 7-eleven enters a new city, and almost every time it enters a new city, it gives rise to greater attention and traffic. For example, the opening of its first shop in zhengzhou amounted to $650,000 on that day, while the opening of a cigarette shop amounted to $750,000, continuously updating the record of one-day sales at a global convenience store。

In the overall brand development, there is nothing more noteworthy than the news that 7-eleven will be acquired in recent days. Although a final decision has not yet been taken by seven & i holdings, this also reflects the significant changes that 7-eleven is undergoing. With japan’s depressed market economy, 7-eleven’s japanese operations are also caught in the bottleneck of growth。

The chinese market, 7-eleven, is also facing a critical moment. On the one hand, the market for convenience stores has become more competitive, with well-known chains of brands hitting the city slightly, and on the other hand, emerging business patterns such as catering and instant retailing have further divided the market for convenience stores。

In conclusion, while 7-eleven is in the global market, it is difficult to make a big difference in the chinese market. Currently, 7-eleven does not have much advantage over many powerful opponents. The 7-eleven brand does make a lot of noise for the allies, but there are many challenges to its current development in the chinese market。

03 operational capacity

The fact that 7-eleven has been in the national market has meant that the ownership of 7-eleven in different regions belongs to different companies。

For example, the beijing and tianjin regions belong to zhongqing (beijing) ltd., the south china region belongs to guangdong sai's convenience store ltd., the east china region belongs to the unity group, and henan's 7-eleven is owned by the three foodstuffs. Therefore, if the association wishes to contact 7-eleven, it must first find a local partner。

As can be seen from the regional collaborators, these companies are local champions, with extensive retail experience and excellent business resources。

From an operational point of view, the chairman and general manager of 7-eleven in china believed that the core competitiveness of 7-eleven lay in commodity power。

As early as 2005, the seven & i holdings group created its own brand, seven premium, as a high-end product, with the idea of creating good taste, secure, high-quality and price-competitive products。

According to the latest data, the number of commodities in seven premium has expanded to 3400, with more than 300 items sold in excess of 1 billion yen per year. As of the 2023 fiscal year, the cumulative sales of seven premium exceeded 15 trillion yen. Throughout the commodity structure, seven premium accounts for 70 per cent of sales, almost 30 per cent higher than rosen and his family, who also pursue their own brand strategy。

In the case of single-door shops, 7-eleven usually sells about 2900 skus, of which its own brand accounts for more than 68 per cent, covering a wide range of categories ranging from food to everyday goods, including, but not limited to, the own brands of seven premium and seven gold。

The flourishing of their own brands has increased the differential competitiveness of 7-eleven and has led to the emergence of convenience stores selling “marks”, laying the foundation for sales. At the same time, in terms of its own brand sales, 7-eleven is good at tapping and meeting changing consumer demands for commodities and building long-term capacity for commodity power。

In addition to her own brands, as reported by jingxie, fresh-food products, 7-eleven has been actively improving, and 7-eleven has professional subject teams in rice, sandwiches, pasta, etc., to support factories in various locations; in addition, 7-eleven has been providing marketing support on the strengthening line. At present, 7-eleven's ff-day distributions account for half of the total in the marketing system, and sales sales of top10 commodities are all differentiated ff-day foods。

Figure source: narrow front eye

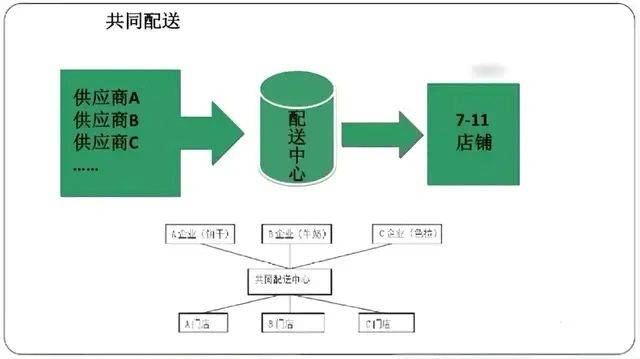

In terms of supply chain, after many iterative periods, 7-eleven is currently adopting a common distribution model, i. E., uniform acquisition and distribution in different regions. The distribution centre has a computer network distribution system linked to suppliers and 7-eleven stores。

In order to ensure that products are fresh, 7-eleven will implement the entire 7-eleven convenience store under the concept of “temperature management”. 7-eleven subdivided the product into temperature bands such as refrigerated, micro-cooled and warmer, using different distribution equipment, distribution time and distribution frequency for products of different temperature bands。

According to the data, 7-eleven operates a “three times a day” distribution system. From 3 to 7 a. M., general food produced the previous night; from 8 to 11 a. M., special foods produced the previous night, such as milk, fresh vegetables, etc.; and from 3 to 6 p. M., food produced that morning。

The frequency of distribution three times a day ensures both availability and freshness of food. Similarly, 7-eleven has mature supply chain and front-end digitized systems capable of achieving precision。

Source: food for all online

It is worth noting that, although 7-eleven operates on 24h, not all shops in the chinese market operate on a full-time basis, with different opening hours in different regions. For example, at night, there is an early closure of a door shop near a university or far from the city。

Although 7-eleven has a well-developed back-end facility, there appears to be little new movement in business innovation. And its competitors are moving a lot. For example, rosen has developed a business model for “three-tier consumer space”; family convenience stores have launched a fifth-generation shop to fully open the “five meals a day” strategy; and good germany has adopted the “one plus x” model through the establishment of a new retail business department and extended community groups to purchase tentacles, open offline no-man shops, and host vending machines。

Overall, the operational strength of 7-eleven is greater in terms of systems, products and transport, but there is a slight shortfall in business innovation。

04 brand values and consumer preferences

Based on the above-mentioned micro-credit index data, while chinese consumers are more receptive to 7-eleven, 7-eleven's own marketing performance in the domestic market is still inadequate, and brands are frequently caught up in public opinion, affecting image。

In may this year, news of the closure of two farmers' springs in 7-eleven jiangsu's stores was a source of enthusiasm; in the summer of 2022, some of the 7-eleven stores showed “she is not drunk, she has no opportunity” for the sale of drinks, and were accused by netizens of openly insulting women, causing outrage among chinese netizens, with a huge negative impact on brand names。

Although in these incidents the 7-eleven branch of the region apologized on the first schedule, the impact on brand image was irreversible。

More importantly, once the negative situation has occurred, the 7-eleven branch has tried to disassociate itself from the official relationship with the affiliated parties, claiming that these acts are only personal acts by the employees of the front shop and do not represent the position of the head office company。

The above-mentioned information reflects the shortcomings of the 7-eleven licensing system, namely the difficulty for regional partners to fully transmit the 7-eleven concept of operation and management to individual allies, and the lack of regulation and regulation of individual allies。

According to the 2023 disapproval zero satisfaction survey, published in 2023 by the eastern expiry centre, 7-eleven is in third place at 4. 33, lagging behind rosen's convenience store (4. 35, first) and the family (4. 34, second). This also shows that there is considerable room for progress in the integrated services of 7-eleven。

Taken together, 7-eleven is a more mature project for the grouping, but the investment risk is also higher, mainly because of its higher investment costs and longer return cycles, as well as the higher threshold for the grouping. Currently, chains of convenience are rich and diverse in brand names and market options, and it is recommended that a number of stakeholders be considered and approached with caution。

Moreover, although the volume and size of the country's convenience stores are increasing, there is a trend towards saturation in some regions. At the same time, the rapid development of discounts, membership and instant retailing is further eroding the market share of convenience stores. The increasing competition for convenience stores and the growing difficulty of the “crawling for steel” business are facts that require more consideration as to whether to join them。

About joining up

In 2024, there was an increase in the intensity of the feeding track. Early in march, a press release announced that the company would pursue a licensing model to further the expansion of the restaurant network, followed by the opening of the concession by another chain of brands, zhongqing qing qian, and, in april, a public announcement from guangjin, stating that the company had introduced a “0 plus fee” policy in its first year of contract, in order to relieve the initial pressure on union traders to open a shop. A chain of brands opened up the road to a fight, holding all the allies in the way。

As the business model that seems to be the easiest to start and best suited to start a business, the alliance is the preferred option for small and medium-sized entrepreneurs. A set of data is being circulated among the communities, where the rate of success of self-employed smes is less than 5 per cent, while the rate of success of unionization is over 60 per cent. However, the disparity in the comparison of data does not deny that membership remains a risk investment that goes hand in hand with a trap. There is no shortage of cases of fraud and deception behind the myth of richness of some of the allies。

For the chain of brands, each member of the consortium is also a living entrepreneur when it becomes a sample of data supporting a beautiful valuation. As a vertical media platform in china’s retail business sector, “retail business finance” will focus on the brightest successful, but it is more desirable to provide a comprehensive and intuitive reference for a wider group of small and medium-sized entrepreneurs, avoiding, as far as possible, errors in decision-making caused by inadequate knowledge。

1. 7 - eleven zhongxi, china: upholding the foundations and safeguarding consumption

[unique] `small and small' reverse rises to a higher level of immediate retail satisfaction - a 2023 zero satisfaction survey covering 16 major retail businesses

How good is the supply chain of 3. 7-eleven