Although the time available for the 2018 primary accounting examination was limited, efforts were made to make full use of the time available for the preparatory examination. In preparation for the basics of the economic law, the editor-in-chief is short-lived and complex, and only by keeping his usual mind calm and prepared for the examination will he see victory。

Contents navigator

Unit internal control systems (2)

Chapter

This knowledge point belongs to the legal system of accounting under chapter ii of the fundamentals of economic law

[knowledge point] unit internal control system (2)

Unit internal control systems (2)

3. Enterprise internal controls

(1) control of incompatible job separation

1. Enterprises are required to analyse and streamline the incompatible functions involved in business processes in a comprehensive and systematic manner and to implement the corresponding separation measures to form a work mechanism that is functional, accountable and mutually regulated。

Incompatible functions include:

(a) authorization to approve and operate;

(b) operations and accounting records;

(c) custody of accounting records and property;

(d) operations and inspection;

(e) authorization to authorize and supervise inspections。

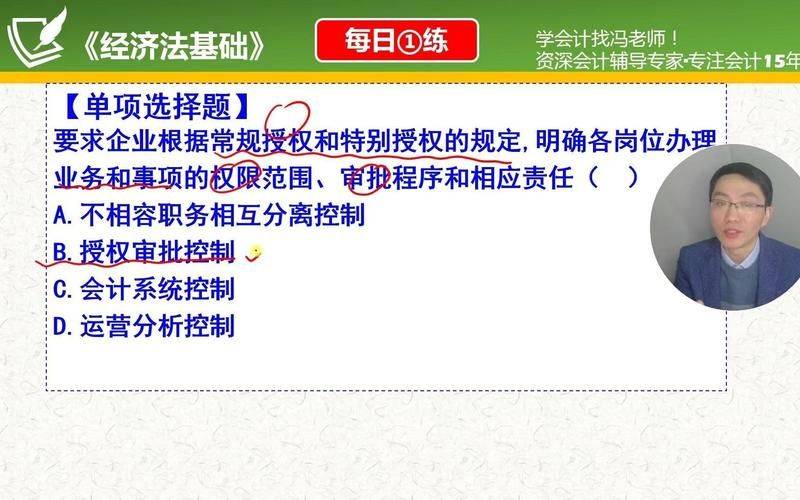

(2) authorisation of approval controls

Enterprises are required to specify the scope of their competence, approval procedures and corresponding responsibilities for the operation of their posts, in accordance with the provisions of the regular and special delegation of authority。

(3) control of the accounting system

Enterprises are required to strictly enforce a uniform national accounting standards system, strengthen the accounting base, clarify the procedures for processing accounting certificates, books of account and financial accounting reports and ensure the integrity of accounting information。

(4) control of property protection

Enterprises are required to establish systems for the day-to-day management and periodic inventory of property and to ensure the security of property by means of such measures as property records, physical custody, periodic inventory and reconciliation of accounts。

(5) budgetary control

Enterprises are required to implement a comprehensive budget management system, clarify the responsibilities of the responsible units in budget management, regulate the preparation, validation, issuance and execution of budgets and strengthen budgetary constraints。

(6) operational analytical control

Businesses are required to establish a business situation analysis system, and managers should use a combination of production, purchase and sale, investment, financing, finance, etc., and conduct regular business situation analyses, identify problems, identify causes in a timely manner and improve through factor analysis, comparative analysis, trend analysis, etc。

(7) performance appraisal control

Enterprises are required to establish and implement a performance appraisal system, a system of scientific evaluation indicators, periodic appraisal and objective evaluation of the performance of the responsible units within the enterprise and of all employees, using the results of the appraisal as the basis for determining the remuneration of employees and for promotion, merit, demotion, reassignment, dismissal, etc。

Take the 2018 primary accounting examination seriously and learn as much as possible to practice and not waste time. People who appreciate time and learn are the happiest to obtain a synthesis of basic knowledge points on economic law in primary accounting。