The question of the enterprise internal control examination is shared by members and can be read online, and more of the related question of the enterprise internal control examination (8-page collection) is available online in the library。

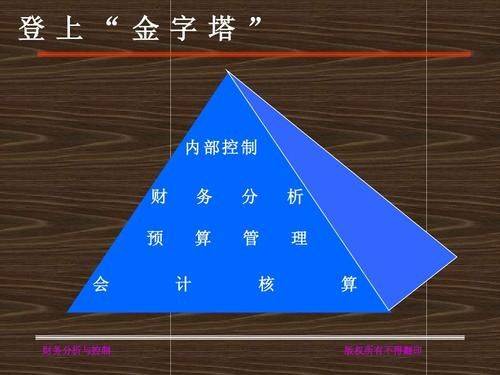

Chapter 5-6, chapter v, option 1. The purpose of an information system is (a) a to provide information services to the organization in support of management decision-making activity b, and (c) to perform periodic accounting assurance of compliance with accounting information systems. A. Inaccuracy in the following statement of accounting informatization and control in the statement of a. C. D. 5. Below is that computer information technology is used as a substitute for manual financial information processing, and that alternative manual analysis and judgement of accounting information b. Enterprise cashiers can act as computerized system administrators and review vouchers. C. Enterprises should establish an information-based accounting file management system d. Informatization accounting files, in the form of accounting data stored in magnetic or cd-rom media and computer-printed books, including billing, accounting books, financial statements, etc., what is an internal member perception and information-breaking and understanding process. (c) what form can be adopted for the communication with investors and creditors in the external communication of the business process d-recommended business process d-wide training, as part of the process of implementation of the project, as part of the process of organizing business and technical cadres to work with service providers to achieve technology interface and knowledge transfer as soon as possible, as part of the enterprise-infomatization implementation step (d)a improvement of performance evaluation mechanism b to enhance application of c-recommended business process d? Answer: (a) a: shareholders ' conference b: clients ' colloquium c: routine session d: business fair. Which aspects of the enterprise are not critical for adequate internal communication? (d)a: control environment b: control operation c: risk assessment d: control activities. Which of the following 10 are not external (c) a, communication with investors and creditors b, communication with customers, suppliers c, communication with employees of the enterprise d, communication with regulators 1 has an interaction between internal controls and accounting information, and checks on each other. The corporate risk of jointly securing the performance of the commissioning agent contract 2 is mainly strategic. 3. Systemic planning of the general principles of enterprise information development. Step-by-step inputs. Communication refers to processes within the enterprise (membership perception) and (information communication and understanding). Adequate internal communication plays a crucial role in business (control environment), control operations, risk assessment, etc. 1. What are the plans for the development of a business information package? Answer: (1) a highly unified consensus is formed. (2) establish clear implementation objectives. (3) identify the integration of enterprise business processes with information systems. (4) establishment of a system of rigorous regulation and enforcement (5) establishment of a complete, accurate and unified base database2 good internal controls, including communication on both sides? And say that external communication should focus on four aspects? Response: what should be the focus of internal controls, including internal and external communications: communication with investors and creditors2 and with customers, suppliers3 and regulators4 and intermediaries3? Communication with investors and debtors. Communication with clients, suppliers. Communication with regulators. Communication with intermediaries. The term explains what business information means when information systems identify, measure and report. Sourced from within the enterprise, including information obtained on industries, the economy, and management of internal production operations, finance, etc. 2 what constitutes an enterprise's financial risk is the objectively present opportunity or likelihood that an enterprise will suffer loss as a result of a combination of unpredictable or unforeseeable factors in its financial management activities. 3 communication mechanism: the process of communicating and understanding the ideas and information of the members within the enterprise, including downward and upward horizontal communication within the enterprise. In an effective manner and to some extent, the information is transmitted in a timely manner to those who need to use it to fulfil their control and other responsibilities. 4 external communication: enterprises establish good external communication channels, document recommendations from external parties, complaints and other information received, and process and provide feedback in a timely manner. Chapter vi, option 1. Self-evaluation of internal controls is based mainly on three approaches: seminars, and management analysis (d). A. Public opinion b. Book access c. Leading oversight of the audit process under the d questionnaire b. Audit preparedness and audit plan b. Internal control environment and business process analysis c. Audit testing d. Identification and evaluation of which of the following models found in the audit report e. Audit was that internal audit could not directly serve operational decision-making (b). A. Board leadership model b. Managing model c. Managing model 4 for the overall operations of the company and the implementation of the internal control system is (c). In terms of specific monitoring, the following areas do not require attention: (d) a selection of subjects for evaluation; (c) selection of monitoring methods and frequency; (d) reporting of monitoring results; (e) what should enterprises do with significant internal deficiencies or risks identified during supervision and inspection? (d) a. Information feedback on which of the following items is not part of the internal control gap reporting system (c) a. Oversight inspection activities b. Reporting to the board of directors should be done in a timely manner b. Reporting to the board of auditors c. Reporting to managers should be done in a timely manner d. Information feedback on which of the following items is not part of the internal control deficiency reporting system (c) a. Improving the reporting mechanism c. Leadership to strengthen management d. Monitoring the implementation of corrective measures8 the following is not correct (b): an enterprise should develop a system of significant and extraordinary incident reporting (b) that reports problems or deficiencies in internal controls identified in its work to the relevant head of the organization; the relevant unit should report in a timely manner to its superiors in writing d. The emerging risks of periodic or irregular returns by the internal control department9 are not internal control deficiencies reporting systems (d) a, oversight inspection b, improvement of reporting mechanism c, oversight of deficiencies and problems identified by corrective measures 10, and should be corrected in a timely manner, a process that is monitored by (a). The way in which finance section b, division c, division of sales, administration d, fills in control is mainly continuous, specialized, etc.,2 (audit testing) is an important way of conducting internal control audits. 3 significant deficiencies refer to internal control weaknesses identified (real and reliable) that could significantly affect financial reporting and assets (security integrity). The source of information on internal deficiencies (both inside and outside the enterprise) should be (sensitized smell), timely detection and reporting by the enterprise to ensure that (management and internal control) can be effectively overhauled, and an improved internal control system that is concisely focused on 1 specific oversight control, which refers to the occasional and targeted oversight controls undertaken by the enterprise with respect to one or some aspects of the establishment and implementation of internal controls; and what are the aspects of specific controls that require attention? 1. Selected evaluation subjects. 2. Determine the scope and frequency of surveillance. 3. Selection of monitoring methods. 4. Conduct monitoring processes. How can the quality of internal controls be ensured and improved? Response 1: strengthen organizational assurance of internal audit; continuously improve the quality of internal audit staff; carefully prepare for audit; pay attention to audit methods, techniques, rational use of tools5; strengthen audit norms and draft management terminology to explain 1. What is oversight control? Response: refers to the process by which an enterprise monitors and evaluates the soundness, reasonableness and effectiveness of its internal controls, resulting in a written inspection report and corresponding processing. 2. How is special surveillance conducted? Answer: (1) selection of evaluation themes (2) determination of the scope and frequency of controls (3) selection of monitoring methods (4) what is the definition of conducting internal audits of the control process? The internal audit of an enterprise is an independent and objective monitoring, evaluation and consulting activity within the enterprise. Its purpose is to detect and prevent errors and fraud and to increase the efficiency of the operation of the enterprise and add value to the enterprise。response: deficiencies in internal controls refer to deficiencies in the design of internal controls that are not effective against errors and fraud, or weaknesses and deviations in the functioning of internal controls that cannot be detected and corrected even in cases of errors and fraud