Overview: in june, against the backdrop of a gradual adjustment of the domestic macroeconomic phase and the complex and volatile international situation, the domestic sector was characterized by a slow season, with a small 2. 5 per cent increase in the actual purchases of steel from sample firms. In july, macroeconomic policies continued to work, the weather effects of the rainy season in the south were gradually reduced and terminal needs are expected to remain resilient as the availability of funds for some sites improves。

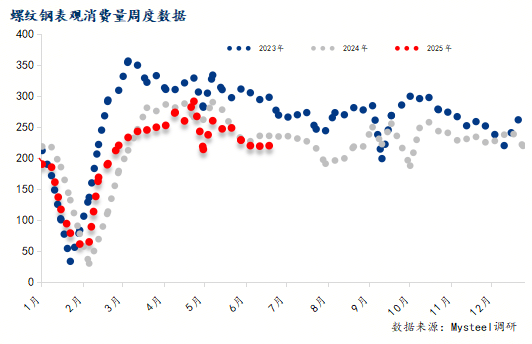

Looking at the full sample caliber data, in june 2024 the market averaged 2,324. 5 million tons per week of surface consumption and the highest monthly value was 2,358,000 tons. In june 2025, the average weekly value was approximately 22,02. 25 million tons, with a peak of 2,290. 3 million tons per week of surface consumption, which was 4. 49 per cent lower than the same period last year, with a narrow reduction. The overall demand performance in the market in june was good, and it remained relatively stable during the traditional off-season period。

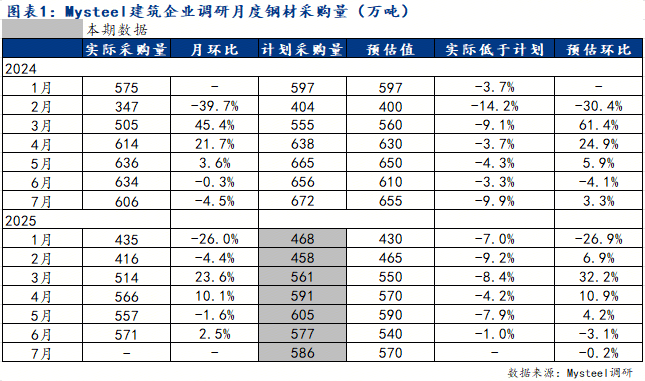

The mysteel construction enterprise research data show that actual steel purchases in june 2025 amounted to 5. 57 million tons, a 3. 5 per cent decrease compared with the projected purchases and a 2. 5 per cent increase in the monthly cycle; and the planned steel purchases in july, 5. 86 million tons, were projected to remain stable in july based on actual purchases in june, planned purchases by businesses and current market performance。

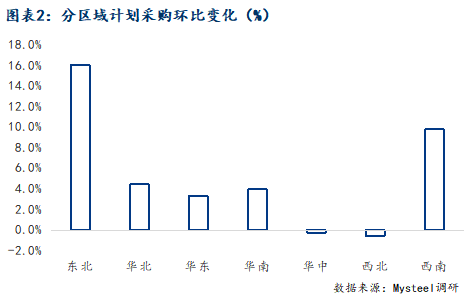

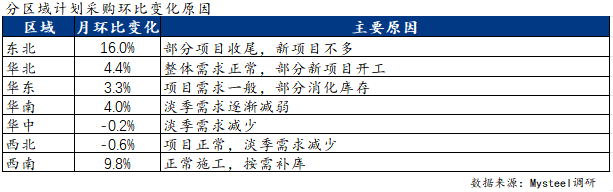

In june, the total procurement volume of steel for construction in sample enterprises increased slightly across the country, although there was some variation in performance across regions, and the north-east region continued to show growth, with an increase of 28. 4 per cent, followed by east and north china, with an increase of 11. 57 and 5. 3 per cent, respectively, and a decrease of 7. 06 per cent in other regions, particularly south-west. In the current study, the regional demand plans varied slightly, but with the exception of the reduction in the north china region, all the regions were flat or growing, although the overall increase was modest, more than 10 per cent。

In the light of the findings of the current study, the planned procurement volume for the construction enterprise increased again in july, but only slightly, owing mainly to the relatively small number of new projects and the fact that part of the region suffered from high temperatures and heavy rainfall, which did not result in a significant increase in overall demand。

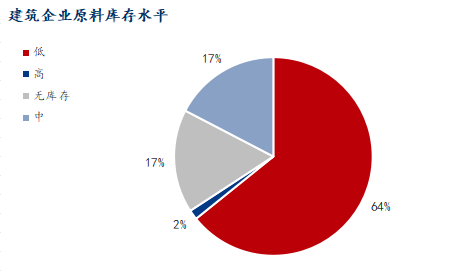

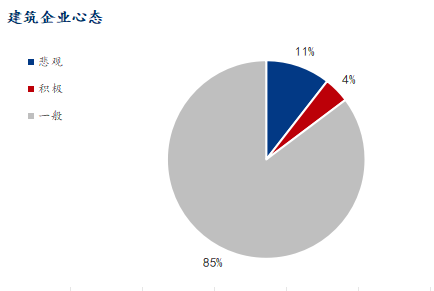

Qualitative indicator feedback: the proportion of “unstocked” stock levels in construction enterprises has increased and the proportion of “low stock” has decreased; the proportion of “low” returns continues to rise; and the proportion of “negative” construction enterprises has also continued to rise (see figure below). This also reflects an increase in uncertainty and pessimism in the market for the future, so that enterprises are more inclined to maintain low stock levels and to procure according to project requirements。

In summary, in june, while the market was in the traditional low-season season, influenced by medium- and high-level factors, terminal demand remained positive and demand for steel in the downstream construction industry remained strong. While access to the july market is expected to be better at macro level, with some regions experiencing high temperatures and reduced rainfall impact, project construction will remain relatively stable with further improvement in the project's funded rate, and construction steel demand is expected to remain relatively stable in july。