Is it always a mess when you sell a house? How much tax is it? In the past, different urban policies had varied considerably, with far-reaching northern and third-line cities implementing different standards, buyers and sellers not only cross-checking policies, but also making it easier to pay falsely for perceived deviations, and many families had been delayed in implementing housing improvement programmes because of the high taxes and fees for short-term replacements。

In response to this practical problem, the ministry of finance and the general tax administration jointly issued the bulletin of the general tax administration of the ministry of finance on the value added tax policy for the sale of housing by individuals (no. 17 of 2025) on 29 december 2025, which defines the uniform implementation criteria for the value added tax for the sale of housing by individuals, which has been in force since 1 january 2026. This new central focus on “harmonizing policies and reducing tax rates” completely addressed the fragmentation of previous territorial policies and provided a clear and clear basis for tax collection by the sellers. It will be read in conjunction with the original official communiqué and the authorities of the tax authorities, to dismantle the core of the policy, the details of the exercise and the attention given to it in the common language, and to provide compliance information for residents with a demand to sell or replace their houses。

I. New core elements: 2 harmonized standards, clear policy basis

In accordance with proclamation no. 17 of 2025 and the relevant provisions of the vat act, only two core criteria have been retained for this adjustment of the vat policy for personal sales, which is implemented uniformly throughout the country, without geographical exceptions, and all provisions have a clear legal and policy basis。

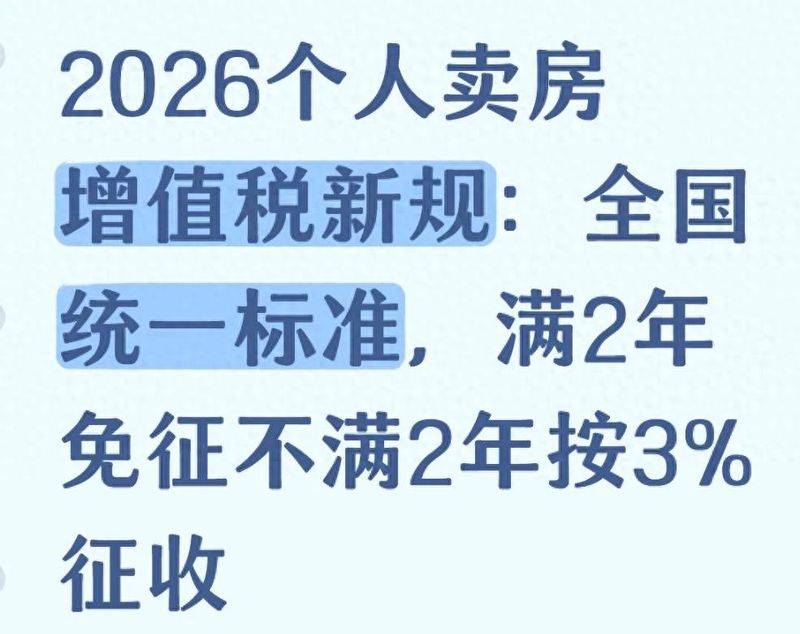

1. Sale of housing for less than 2 years: 3 per cent unified rate of vat

Article 1 of the proclamation clearly states: “an individual will pay vat in full at the rate of 3 per cent for the external sale of a house that has been purchased for less than two years.” this criterion replaces the 5 per cent rate previously implemented after the “breeding of a battalion” (fiscal tax [2016] 36 according to the circular of the ministry of finance of the national tax administration on the full deprivation of business taxes to the vat pilot)。

The policy context for the adjustment of the tax rate is the simplification of the collection rate following the formal implementation of the law of the people's republic of china on value added tax, the uniform application of the 3 per cent rate for the sale of real estate by small taxpayers, and the simultaneous enjoyment of this legislative adjustment dividend by individuals as special tax subjects. In terms of the actual amount of tax paid, for example housing with a tax value of 2. 1 million yuan, vat was paid under the original policy: 2. 1 million ÷ (1+ 5 per cent) x 5 per cent = 100,000 yuan; payments under the new policy were 2. 1 million ÷ (1+ 3 per cent) x 3 per cent ≈6. 12 million, with a direct reduction in tax and excise expenditure of about $38. 8 million, effectively reducing transaction costs for short-term replacement housing。

2. Sale of housing after 2 years: national uniform exemption from vat

Article 2 of the proclamation states: “an individual shall be exempt from vat if he or she purchases housing for a period of more than two years (including two years).” this provision completely eliminates the previous policy of geographical differentiation - – under the original policy, four cities in the northward and deep are still required to pay vat on the basis of the difference between two years of sales of non-ordinary dwellings (based on fiscal tax [2016]) annex 3 to the new rules provides for a uniform exemption “without distinction as to city or type of house”。

This means that no value added tax is payable, regardless of whether the house is located in a front-line city or a centre-western county, whether it is an ordinary or a non-ordinary dwelling, as long as it is held for two years for external sales. The policy is based on the legislative orientation derived from the vat law “to support the reasonable housing needs of the population”, which removes geographical policy barriers by harmonizing tax standards。

Scope of application of policy: individuals only, except for two categories of subjects

According to article 3 of the proclamation and as interpreted by the general tax administration, the subject of this preferential policy is “natural persons”, and the following two categories of cases are not applicable:

The sale of housing by the general taxpayer among the self-employed is subject to taxation according to the general tax method of “sale of immovable property” (9 per cent applied, according to article ii of the vat law)

2. Small-scale taxpayers in individual business households who sell purchased housing may do so by reference to individual policies, subject to confirmation by local tax authorities in conjunction with actual administration, and recommend that the competent tax authorities be consulted in advance。

In short, persons who own and sell housing in their own name and who do not belong to the general taxpayer of an individual entrepreneur are entitled to a policy of exemption from recruitment for two years and 3 per cent for less than two years。

Ii. Key details of ethics: clear implementation standards based on official regulations

In conjunction with the policy implementation guidelines annexed to proclamation no. 17 of 2025 and the practice of tax collection and administration of real estate transactions, the following practical details are given a clear policy basis and require attention:

The “two-year period” test: “the date of the tax clearance certificate or the property certificate”

In accordance with article 1 of the annex to the bulletin and the circular of the national tax administration on several specific issues in the implementation of the real estate tax policy (state tax) (no. 172) the time of purchase of the house is determined according to the “first-in-first-in-first-in-first-in-first-in-first-in” principle: the date of the netting contract, the date of delivery of the house, is not used as the basis for the determination, which is based on the earlier dates of “the date of filling in the tax certificate” and “the date of registration indicated in the certificate of title to real estate”。

For example, the tax certificate for a dwelling is dated 10 march 2024, the registration certificate is dated 15 may 2024, the age limit for holding the property is set at 10 march 2024, and sales after 10 march 2026 are eligible for tax exemption; if the tax ticket is later than the date of the property certificate, the date of the property certificate is used. This standard of determination is uniform across the country and avoids disputes over taxes and fees due to time differences。

Policy interface: undeclared transactions prior to 1 january 2026 are subject to new regulations

Article 4 of the proclamation defines the policy interface rule: “if a sales contract has been concluded before 1 january 2026 but no vat has been declared, it shall be enforceable under the conditions set out in this proclamation.” if a transaction (net-marked, household transfer) is completed before 1 january 2026 but no vat is paid, a new regulation is applied for exemption if the house has been in possession for two years; for less than two years, a 3 per cent rate is declared and no 5 per cent rate is required。

The general tax administration, in its reading, specifically cautions that such cases require additional declarations to be submitted to the competent tax authorities of the place of residence by 30 june 2026, which may result in late payments, and recommends that eligible taxpayers carry the relevant materials as soon as possible。

3. Tax-exempt declaration: national common list (based on the code of interdiction)

In accordance with the national code of tax administration (version 3. 0) and the requirements of the proclamation, applications for vat exemptions are required to provide the following material, which can be combined with actual additions, but the core material is unified throughout the country:

• certification of the identity of the taxpayer (original identity card of the buyer and the buyer and a copy thereof)

• the original and a copy of the certificate of real estate title (property certificate) (certification of title)

• originals and copies of tax clearance certificates (key basis for holding age determination)

• the original and a copy of the online sales contract (certification of the authenticity of the transaction)

• original purchase invoices or purchase contracts (ready for inspection to verify purchase time)

• supplementary information on special circumstances: notarized power of attorney is required for commissioning the chargé d'affaires; marriage certificates are required for common property of spouses; certificates of devolution of title, such as inheritance certificates, gift contracts, etc., are required for inheritance, gift and acquisition of property。

The processing takes place at the tax window of the government service centre, where the premises are located, and the process is “methodology review—registration of tax sources—registration of tax exemptions”, which is completed on an on-site basis and does not require additional approval。

4. Common error zone clarification: correction in accordance with the original policy

In conjunction with the “policy questions and answers” section of the network of officials of the general tax administration, the following areas of error need to be clarified in order to avoid prejudice to interests:

• mistake 1: no vat for falling house prices? Corrected: vat is taxed by transactional behaviour, not related to the rise or fall in the house price, and is paid at a rate of 3 per cent for all sales less than two years (in accordance with article 1 of the bulletin)

• mistake 2: 2 years, reference time for netting? Corrected: the netting date is invalid only on the date of the tax clearance certificate or the property certificate (in accordance with article 1 of the annex to the bulletin)

• mistake 3: are individual entrepreneurs directly entitled to benefits? Correction: the general taxpayer of individual business owners is not applicable and small taxpayers are required to consult local tax authorities (under article 3 of the bulletin)

• mistrial 4: recalculation of the years of possession of the house granted? Corrected: houses divided by inheritance, gift, divorce, with the number of years held according to the length of the original purchase (under state tax no。

Iii. The context of policy development: a smooth development orientation based on the real estate market

Proclamation no. 17 of 2025 marks the beginning of the fifteenth anniversary of the adoption by the state of a policy-oriented and well-founded approach to housing and decent housing needs:

1. Activating the stock market: reducing transaction costs for flow

According to the national statistical office, the trade in second-hand houses in 2025 accounted for 41 per cent of the total housing transactions, and the efficiency of the stock market directly affected the balance between supply and demand for housing. The high taxes and fees on short- and medium-term transactions of the original policy resulted in long-term unmarketable holdings of some housing sources, and the new policy, by lowering tax rates and harmonizing standards, increased the effective supply of housing stock markets, matched the policy orientation of “returning houses to residential properties”。

Support for “sale-new”: unlocking improved demand

In the fourth quarter of 2025, the central bank's municipal depositories questionnaire indicated that 35. 2 per cent of households had a need to improve their housing, of which “sell new and old” was the main method. The high tax rates for short-term replacements under the original policy were an important obstacle, as the new regulations reduced the cost of “selling old” and helped families to “sell for good” and “sell for good” while boosting the demand for new housing and creating a virtuous circle of second-hand homes。

3. Harmonizing the market environment: safeguarding tax equity

The previous policy of geographical differentiation had led to a “discretionary tax on housing”, and some of the trans-city replacements faced policy interface problems. The new regulations, which achieve national harmonization of standards, both reduce the cost of taxpayers' policy understanding and avoid inter-territorial tax competition, comply with the principle of “tax equity” and lay the institutional foundations for the smooth development of the real estate market。

Iv. Guidance on trade pits: based on legal provisions and inquisitorial practice

In addition to the value-added tax policy, housing transactions require the following compliance points, in accordance with such laws and regulations as the civil code, the provisional regulations for the registration of real property, and transaction practices:

1. Verification of property rights: ensuring that rights are not flawed

Prior to the transaction, the immovable property registry must look for a certificate of ownership of the real estate, focusing on:

• whether the owner is a registered holder of rights and whether there are co-owners (e. G. The spouses jointly need to agree to sell them)

• whether there are limitations to the right to mortgages, seals, pre-registrations, etc. (with mortgages subject to interpretative custody)

• legitimacy of tenure sources (inheritance, gift and house transfer formalities are complete)。

The fact that the property ownership was defective was not able to move through the house, which could result in the contract being avoided, and it was recommended that verification be completed prior to the transaction。

2. Taxation: written agreement to avoid disputes

Under article 510 of the civil code, the payment of the transactional fee for second-hand houses may be agreed upon by the parties, provided that it is clearly stated in the netting contract: the party responsible for the payment of taxes, such as vat, personal income tax, deed tax, etc., and that the tax is “executed in accordance with the state's latest policy, with the additional deduction”. Avoid verbal engagement and prevent disputes arising from policy adjustments。

3. Financial regulation: priority for official channels

In accordance with the circular of the ministry of housing and urban and rural construction on the regulation of the financial regulation of second-hand home transactions, it is proposed that the payment be made through the funds monitoring account set up by the bank or by the government service centre, which is the procedure whereby the buyer deposits the house in the supervisory account and completes the transfer of the funds to the seller. To avoid private transfers and to guard against the risk of “failure to pass” or “failure to get” through。

4. Factual disclosure of premises: avoidance of liability for fraud

Under article 6112 of the civil code, the seller is obliged to inform the seller in good faith of important information on the quality of the house (e. G. Structural cracks, leaks), restrictions of rights (e. G. In the case of leases). Deliberate concealment may lead to avoidance of the contract and entail liability; the buyer is required to inform the buyer of the legal provisions for “buying and selling the lease” and avoid subsequent disputes。

Summary: policy location requires “compliance declaration, accurate enjoyment”

The new regulation of the vat for the sale of housing by individuals, introduced in 2026 and centred on “national harmonization, reduction of tax rates, simplification of processes”, provides clear tax guidelines for the sale of housing by residents under the vat act and proclamation no. 17 of 2025. For individuals with transactional needs, there are three priorities:

(a) “assignment of a period of time”: the date of the tax certificate and the date of the property certificate shall be the first to determine whether the conditions for exemption have been met

2. Complete declaration: prepare for the national common list to avoid delays due to missing material

3. Compensatory completion of transactions: clear payment of taxes and fees, selection of funds, and security of transactions。

In the case of non-declared value added tax (vat) for transactions that occurred prior to 1 january 2026, additional declarations are required by 30 june to avoid delays. If there is doubt about the application of the policy, it can be consulted through the “tax service” section of the network of officials of the general tax administration, or by calling the tax service hotline of 12366, or directly consult the competent tax authorities in the place of residence to obtain authoritative answers。

This policy adjustment is an important measure of the state's support for reasonable housing needs and for the smooth and healthy development of the real estate market, reflecting both the precision of tax policy and the concept of “people-centred” development. With the implementation of the accompanying inquisitorial measures, second-hand house transactions will be made more transparent and efficient, effectively safeguarding the legitimate rights and interests of both buyers and sellers。