Double carbon-activated power revolution: who will dominate the new energy ecosystem

I. Electronics definitions and scope

The electricity sector is the fundamental pillar of the national economy and refers to the sum of economic activities around electricity production (power generation), transmission (transfer and transformation), distribution (distribution), marketing (electricity) and services. Its core mission is to provide a safe, stable, economical and clean electricity supply to society as a whole. In the context of the “twin carbon” strategy, the modern power industry is accelerating the profound transition from the traditional one-way chain of “release-sharing-use” to a “new electricity system” that interacts with new sources of energy, the main source network of the grid, as the main battleground for the energy revolution。

According to the national economic industry classification (gb/t 4754-2017) of the national statistical office of china, the electricity sector falls under the category “d” - electricity, heat, gas and water production and supply - 44 major categories - electricity, heat production and supply”. It is officially defined as the production of electricity using energy sources such as coal, oil, gas, hydro, nuclear, wind, solar, geothermal, biomass, etc., and the assembly of activities for the transmission, distribution and sale of electricity。

Ii. State of development of the electricity sector: accelerating the transformation of cleanliness, with contradictions and opportunities

(1) historical transformation of installed and power generation structures

By the end of october 2025, our total installed capacity for wind and photovoltaic power had reached 17. 30 billion kilowatts. This figure is expected to rise further to about 1. 8 billion kilowatts by the end of 2025, taking into account the conventional increase in the last two months of 2025. However, coal still provides about 60 per cent of electricity, and the capacity of new energy sources to effectively generate and support systems needs to be improved。

(2) rapid upgrading of grid intelligence

High-tension backbones continue to be perfected, digitalized, intelligent technologies are widely used for grid movement, failure diagnosis and user services, and soft grids and smart distribution grids are the focus。

(3) core challenges

The “triple-high” (high-scale new energy, high-scale electrical and electronic equipment, high-scale high-pressure direct flow) characteristics put enormous pressure on systems to operate safely and securely, reconciling resource shortages, and market mechanisms are not yet fully aligned with transition needs。

Iii. Policy environment analysis in the electricity sector

The policy environment in china's electricity sector since the fourteenth five-year plan has been closely centred on the top-level goal of the “two-carbon” strategy, with the central orientation of “constructing new electricity systems”, which has resulted in a three-pronged policy framework for “security, transformation, market-building”. The framework identifies new energy masters and transformation paths for coal power through programmes such as the “xiv5” modern energy system plan; stimulates technological innovation and investment through such instruments as price, fiscal and green finance; and deepens market-based reforms through mechanisms such as the basic rules for the power spot market, coal power and electricity prices, with the aim of creating institutional mechanisms for adapting to a high proportion of new energy sources. The proposal of the “fifty five” plan to further upgrade this direction into a national strategy, with not only a clear indication of “investment in new electricity systems and energy power countries”, but also a more multidimensional deployment of new infrastructure, science and technology self-reliance (e. G. Ai+), national unified markets, national security capabilities, etc., signaling a shift from a “policy-driven” to a “market mechanisms and national strategies” two-wheel-driven new phase in the electricity sector, with the core task of ensuring energy security and supporting an overall green transformation of the economy and society。

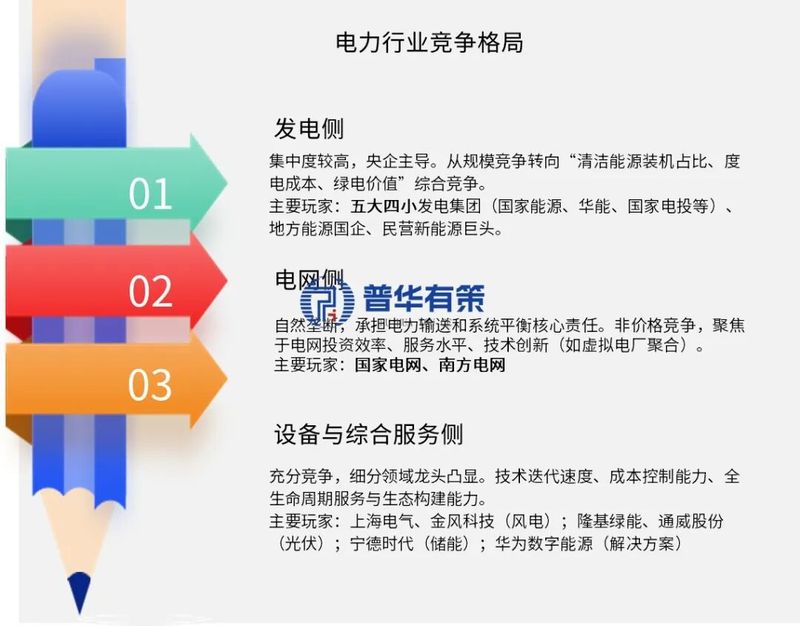

Analysis of competition patterns in the electricity sector

The pattern of competition in the industry is “triple rise”, ecological evolution

V. Main trends in electricity sector development

For the “155” and beyond, china's electricity sector, driven by a combination of policy, technology and market forces, will show the following deep and irreversible trends:

(1) power structure: new sources of energy moving from “mounted subjects” to “power subjects”, systematic re-engineering of coal electric role

Wind and voltage will continue to grow at a scale of hundreds of kilowatts, and will be progressively responsible for basic power supply as a result of technological advances in storage capacity to improve reliable power generation. At the same time, coal power positioning has been systematically transformed into “basic and system-regulated power supply”. The stock fleet will be upgraded through the "triple reconnection" and its guaranteed value will be compensated through the capacity-price mechanism, with the central role shifting to providing peak and inertial support for the system。

(2) system form: the grid accelerates the evolution towards an “invented, interactive, intelligent” energy internet

The grid will shift from a one-way "source-to-load" mode to a "source-to-net "reserve" dynamic equilibrium model of multiple interactions. On the one hand, the main grid will be stronger and the use of ultra-high-voltage channels will be highlighted; on the other hand, the distribution grid will be upgraded to the active smart distribution grid that can absorb distributed energy and support flexible access to electric vehicles. Technology such as digital twinning will make the entire grid transparent and simulated。

(3) technology driven: digitization and ai upgrading from assistive tools to core productivity

Artificial intelligence (ai) and large models will infiltrate and transform the power system in depth. On the side of power generation, ai enhances the accuracy of new energy power forecasting; on the side of the grid, ai drives autonomous movement to respond to malfunctions in milliseconds; and on the side of the load, ai optimizes the aggregation of large-scale distributed resources to facilitate the operation of the virtual power plant (vpp). In addition, ai will drive the transport model from “regular overhaul” to “predictive maintenance”, significantly improving asset efficiency and security。

(4) market mechanisms: a unified national electricity market system is in place and price signals guide the optimal allocation of resources

The national unified electricity market system will be fully implemented, creating a multi-generic complex market that includes electricity energy, ancillary services, capacity and green power trading. A well-developed market mechanism would truly restore the commodity attributes of electricity, channel investment spontaneously through clear price signals to key areas such as new energy sources, storage, and encourage users to optimize energy use behaviour, ultimately minimizing the costs of a society-wide low-carbon transformation。

In beijing, pricewaterhousecoopers ltd., the “fifty five” industrial chain research and forecasting predicatives of trends in whole-industrial chains of electricity, a system of analysis of the chinese electricity sector. First, it defines the scope of the industry and reviews its journey from infrastructure to quality transformation. The report focuses on the current state of development and the “triple-high” challenge, with new sources of energy as its main focus, and presents, in tabular form, the “triple-top” competition patterns and core players of the three blocs of electricity generation, grids and equipment services. The main policy lines for “building new electricity systems” have been identified through the mapping of “145” to “155” plans and recent key policies (with policy tables). The report further looks at the definitive opportunities presented by system regulation, grid upgrading, ai integration and “power plus” ecology, and prejudges four core trends in power structure, system shape, technology-driven and market-based mechanisms. Finally, a brief and detailed analysis of the industrial chain explains how the upstream/downstream has profoundly influenced the development pulse of the industry。

Contents

Part i: industry panorama and macro environmental analysis

Chapter i: overview and development of the electricity sector

1. 1 definition, classification and position of the electricity sector in the national economy

1. 2 overview and trends in the global electricity sector (“xivv” review)

1. 2. 1 global energy transformation and the evolution of power structures

1. 2. 2 comparison of electricity market development patterns in major countries and regions

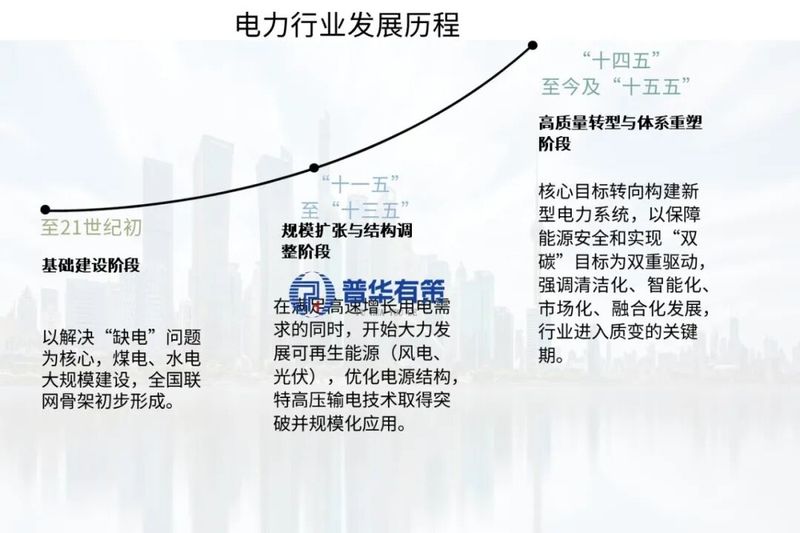

1. 3 summary of the history of the development of the electricity sector and the achievements of the “xivv” in china

1. 3. 1 review of the development process

1. 3. 2 completion of key development indicators for the “xivv” period (loading, power generation, share of non-fossil energy, etc.)

1. 3. 3 current stage of industrial development and basic characteristics

Chapter ii: macro-environmental analysis of industry development (pest model)

2. 1 political and policy environment

2. 1. 1 national strategic direction: double carbon targets, energy security, new quality productivity

2. 1. 2 core policy analysis: “fifty-five” planning proposals, blue books for the construction of new electricity systems, carbon peak implementation programmes, etc

2. 1. 3 industrial policy/planning system alignment: energy, science and technology, environmental protection, regional planning

2. 2 economic environment

2. 2. 1 impact of macroeconomic trends on electricity demand

2. 2. 2 impact of market-based electricity reforms and price mechanisms on the economic nature of industries

2. 2. 3 support for economic instruments such as green finance and fiscal subsidies

2. 3 social environment

2. 3. 1 changes in social use of electricity habits and trends in electricity substitution

2. 3. 2 increased public awareness of the environment for clean electricity

2. 4 technological environment

2. 4. 1 status and trends of relevant technological developments: new energy generation, energy storage, smart grids, hydrogen energy, ccs

2. 4. 2 impact of technology overlaps on industry costs and business models

Part ii: deep industrial chain analysis and market demand outlook

Chapter 3: supply side analysis: power generation structures and grid systems

3. 1 power side: diversity clean supply bureau

3. 1. 1 power capacity, power generation and hours of utilization by type (“xivv data and “fifty-five” projections”)

(1) coal electricity: positioning transformation and flexibility adaptation

(2) hydropower: conventional hydropower and pumping water storage

(3) nuclear power: safe and orderly development

(4) wind/pv: main energy status established, centralized versus distributed

(5) other renewable energy sources such as biomass, geothermal energy

3. 1. 2 upstream raw materials/equipment: supply patterns and price trends such as photovoltaic silicon, wind blades, lithium battery materials, ultra-high pressure equipment, etc

3. 2 electro-grid side: the carrying platform of the new electrical system

3. 2. 1 transmission links: status and planning for the construction of the high-tension backbone network

3. 2. 2 distribution links: smart upgrading and digital transformation of the distribution network

3. 2. 3 system regulation: scale and layout of extraction and development of new types of storage (electrical chemistry, compressed air, etc.)

Chapter 4: demand side analysis: downstream application of markets and regional structures

4. 1 social overview of electricity use and growth drivers

4. 1. 1 review of historical electricity use growth (“xivv”)

4. 1. 2 analysis of changes in power structure (i, ii, iii products and residents)

4. 2 size and prospects of demand for major downstream applications

4. 2. 1 industrial sector: green transformation of energy-intensive industries, demand for electricity in strategic and emerging industries (data centres, semiconductors, etc.)

4. 2. 2 in the area of transport: electric vehicle charging infrastructure network and surge demand projections

4. 2. 3 in the area of construction: electrical demand resulting from electrification and energy conservation

4. 2. 4 in the area of public consumption: the improvement of the level of electrification and the spread of intelligent households

4. 3 regional structural analysis of electricity consumption

4. 3. 1 east-west production and distribution patterns: “west electric east” and eastern coastal load centre

4. 3. 2 focused regional market demand: kyouta, long triangle, hong kong, austro bay, chengsu bi-cities, etc

Part iii: market patterns, competition dynamics and business analysis

Chapter v: market size, concentration and competition patterns

5. 1 industry market size and outlook projections

5. 1. 1 size of the market for investment in the electricity sector (“xivv” statistics and “xv5” projections)

5. 1. 2 subsistence market size projections for power generation side, grid side, integrated energy services, etc

5. 2 market concentration analysis

5. 2. 1 market concentration on the side of electricity generation (cr5/cr10): evolution of patterns dominated by five major power generation groups

5. 2. 2 market concentration on the side of the grid: national grid, double oligopoly pattern of the southern grid

5. 2. 3 centralization of the equipment manufacturing and engineering services market degrees

5. 3 analysis of industry competition patterns (port five)

5. 3. 1 the intensity of competition among existing competitors

5. 3. 2 threats from potential entrants

5. 3. 3 threat of alternatives (other forms of energy)

5. 3. 4 vendor bargaining power (upstream equipment, fuel)

5. 3. 5 buyer's bargaining power (large users, grid companies)

Chapter 6: key business/player depth analysis

6. 1 power generation group

6. 1. 1 enterprise case: national energy group, china energy group, national electricity transfer, etc

6. 1. 2 analytical dimensions: business profile and development strategy / corporate core competitiveness analysis (resources, technology, layout) / business performance analysis (assembly structure, share of renewable energy, financial performance)

6. 2 networking enterprise camp

6. 2. 1 enterprise case: national network ltd., china southern network limited

6. 2. 2 analytical dimensions: business profile and positioning / corporate core competitiveness analysis (network, technology, movement control) / enterprise business and investment planning analysis

6. 3 front camp for new energy and equipment

6. 3. 1 business cases: ninde era (storage), lungi green energy (photovoltaic), golden wind technology (wind power), special transformers (voltaic transformers), etc

6. 3. 2 analytical dimensions: business overview and market position / analysis of core competitiveness of enterprises (technology, cost, brand) / analysis of business operations and market share

6. 4 analysis of the market share of enterprises (in key subdivision areas such as photovoltaic components, wind turbines, energy storage systems, etc.)

Chapter vii: swot analysis of industry development

7. 1 advantages: strong policy support, large markets, relative integrity of industrial chains, partial technology leading globally

7. 2 disadvantages: inadequate system reconciliation capacity, “card neck” presence of key technologies, high cost of parts, market mechanisms to be developed

7. 3 opportunities

7. 3. 1 “fifty-five” plans generate significant investment needs

7. 3. 2 global green trade opportunities

7. 3. 3 the emergence of innovative scenarios for technology integration

7. 4 threats

7. 4. 1 macroeconomic volatility risks

7. 4. 2 geopolitical impact on supply chain security

7. 4. 3 extreme weather frequency

7. 4. 4 increased international competition

Part iv: future prospects, investment strategies and conclusions

Chapter viii: “fifty-five” industry drivers and market size projections

8. 1 analysis of core drivers

8. 1. 1 policy-driven: a “two carbon” strategy and new electricity system objectives

8. 1. 2 technology driven: downside efficiency and new modes of incubation

8. 1. 3 market-driven: growth in electricity demand versus green consumption okay