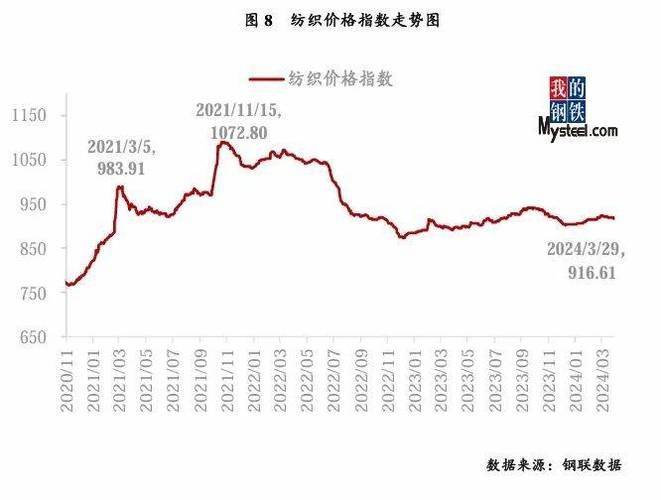

Each accounting, micro-enterprise finance, carries over the avat at the end of the month。

Progress, sales, non-payment of vat, transfer of non-payment of vat, round-the-clock transactions, many of whom know only to carry forward but have no idea of the direction of lending, the logic of carrying forward, and the principle of taxing。

Many bosses also wonder: how does it carry over at the end of the month? How's the balance leveled? What's the returns

Today's full-blown rhetoric, without obscure professional terminology, brings vat to the bottom logic at the end of the month, three tax payments, standard entries, tax reconciliations, and fresh accounting becomes clear at once。

I. Understanding: why vat must be carried over at the end of the month

The day-to-day operation of the business gives rise to tax sales, and the receipt of a receipt credit is the receipt of a tax。

The sale is the money we're going to give to the tax authorities, and the proceeds can be offset by less tax。

Regular books, sales and entries are kept on each other's accounts and have been kept on the books。

By the end of the month, the tax authorities would only see how much you should pay, how much you should pay, and how much you should pay。

Finance must therefore take a step forward: by aggregating all entries and sales for the month, calculating the value added tax that will eventually be paid this month, or by remaining behind with a credit。

In a simple sentence, the carry-over at the end of the month is the consolidation of the bulk sales item into one subject, the calculation of the tax due for the month and the facilitation of tax reporting, reconciliation and reconciliation of accounts。

Ii. General and easy to explain: what is an advance, what is a sale

Foreign sales, the provision of services, the issuance of tickets, and the amount of the face tax are tax payments, which are liabilities and are owed to the tax service。

The amount of the tax that can be deducted from the receipt of goods, the cost of procurement, and the obtaining of a special receipt is the amount of the revenue tax that can be deducted from the value added tax to be paid。

The final formula is very simple:

Vat due this month = tax on sale – revenue

Carry-over at the end of the month is the settlement around this formula。

In total, there are three situations in which sales exceed the amount of the proceeds to be taxed, in which the proceeds exceed the amount of the proceeds to be set aside, and in which the balance is not processed。

Iii. First scenario: sales > proceeds, taxes due this month

This month, businesses pay more, less, less, more and less, and account for the difference and pay taxes at the end of the month。

Logging: transfer of excess tax arrears to non-value added tax。

The difference between the transfer of all sales and the transfer of all entries is the amount of tax due for the month。

Upon completion of the carry-over, the balance at the end of the month of the sales and additions is completely flat and does not accrue。

After the following month's withdrawal, the outstanding vat was offset and the accounts were closed。

Many small businesses have not been carried forward, and the number of sales entries has increased, with year-end accounts being confused and checks, audits and tax alerts checked。

Iv. Second situation: progress > closure of projects between income and income

The month was marked by large purchases, large invoices, significant sales credits and low sales revenue。

The advance is greater than the sale, and the excess tax and tax authority is not required to return it, and can keep it on the books and continue to credit next month and the next quarter, i. E. The entry is set off against the tax。

The processing of the accounts in this case was simple and did not have to be carried over by force。

Excess tax deductions are automatically retained in the amount of the added tax and continue to be offset against the billing charges next month。

The e-tax office's statements, the tax crediting system, are now kept on the books, the accounts are clear and the tax ratio is fully consistent。

Many of the new accountants, regardless of whether they were forced to carry them over, simply miscalculated their credits, were unable to apply for tax refunds and were unable to report the amounts。

V. Third scenario: sales = progress, sales equal

The amount of the monthly billing tax is exactly the same as the amount of the tax deductible, offset by the fact that no tax is paid or set off。

At the end of the month, carry-over entries could be made without separate entries, the accounts would be naturally balanced and tax zero would be sufficient and the operation would be simple。

General taxpayers are different from small ones

Small taxpayers do not have an entry credit, do not have an entry for sale and do not carry it over。

It is only necessary to pay vat when revenue is recognized, and the next month's deduction is offset, and the accounts are simple。

Many newcomers were unable to distinguish between general taxpayers and small players, carry-over entries and misdirect accounts。

Vii. Additional tributions to the vat

Many only carry over vat, forgetting the surcharge。

The city building tax, the education supplement and the local education supplement are calculated on the basis of the actual value added tax due。

The value-added tax was carried over at the end of the month and the additional tax was applied simultaneously after determining the amount due for the month。

Value added tax (vat) is balanced, additional taxes are complete and the tax amounts in the tax returns are fully matched and no tax abnormalities occur。

Value added tax (vat) is tax-free, set-off and surcharges are not charged, and the logic of accounting is fully matched。

Viii. The 5 biggest taxes on daily books the pit

First, sales items were never carried forward throughout the year, there was a large backlog of project balances and early warning of tax winds。

Second, the retention of tax credits is carried over by force, the lending direction is wrong and the books and declarations are never matched。

Third, the advance invoice was not certified as a credit, and the blind entry was carried forward and the credit chain was confused。

Fourth, the value added tax (vat) is transferred only, without any additional taxes, and the reporting tax is abnormal。

Fifth, the following monthly deductions do not offset outstanding vat and the balance of transactions is not maintained。

Once the carry-over is incorrect and the vat returns, the financial statements and the fare book amounts are not matched, it is easy for the tax administration to trigger verification and requires a top-down correction, which is cumbersome。

Ix. Practical effects affected

At the end of the first month, the items were cleared and the accounts kept clean and clean, and the balance was not accumulated。

Second, to accurately account for the monthly tax burden and to control the rate of sales and to avoid overtaxation。

Thirdly, the book value and the electronic tax office report data are fully consistent and there is no risk in accounting。

Fourth, it is clear that the tax is offset, invoices are checked, and annual remittances are clear。

Fifthly, equity transfers, tax audits, internal audit accounts are clear。

In the case of micro-enterprise owners, it is not necessary to do the accounting in person, provided that the logic is understood: the sales are for taxes, the proceeds are for credits and the month-end hedges are calculated。

Accounting standards are carried forward, tax returns are not erroneous and tax risks are significantly reduced。

X. Safe corrective corrective controls, complete to murder vat

There is a rhythm of business billings and purchases, and monthly imbalances are normal。

The month-end carry-over allows for a clear view of the monthly amount of taxes paid and a reasonable validation of the rate of receipt of invoices。

Most of the proceeds are set aside for the following month, while more sales are made in a timely manner, keeping the vat liability within a reasonable range and away from tax anomalies。

The end-of-month carry-over has been smooth for the general taxpayer, the tripartite data are fully matched and fiscal management is well planned。

Final summary

The value added tax (vat) was carried forward at the end of the month, which was essentially a tax liability, a credit for the proceeds and a uniform hedge at the end of the month。

Disaggregation of tax dues, retention of entries in both cases, corresponding to standard transactions, closure of sales at the end of the month and simple and clear reporting of tax reconciliations。

General taxpayers do the core basic work of accounting, learn to carry the logic, no longer use the month-end headaches, and keep their fiscal accounts in order。