Today we are entering a formal learning process, and the version of my study divides the entire accounting into nine topics, the first of which is called general remarks。

Today's content includes a summary of the topics, key considerations, the nature of accounting, and financial reporting objectives:

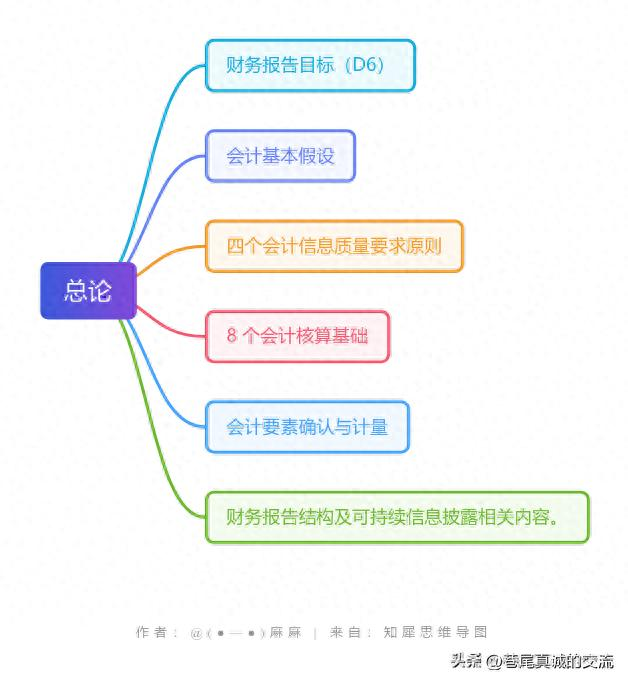

I. Overview of the topic

Key elements: financial reporting objectives, basic accounting assumptions, four principles of accounting information quality requirements, eight accounting bases, accounting elements recognition and measurement, financial reporting structure and sustainable information disclosure。

Values are low, but they are fundamental and need to be understood。

Key points

1. Principles for the quality of accounting information (8 in total, 4 easy to assess)

Comparability

Importance

Prudence

Material over form

Requirements: understand and theoretically link practical application。

2. Element identification

Loss recognition

Profit and loss are split between current gains and losses and directly include owner's interests

Definition of assets, liabilities, income, costs

3. Scope of application of measurement attributes

Clear application of measurement attributes such as historical cost, present value, fair value, net realizable value, etc. To different scenarios。

4. Changes in accounting elements

Consider business-induced changes in accounting elements from the point of view of accounting entries, which are regularly taken into account in primary accounting, and are occasionally referred to。

5. Legislative provisions

Ethical content of accounting

Principles for sustainable information disclosure

6. Nature and process of accounting

Essential: accounting is an act of accounting that reflects the financial movement and oversight, an information processing system, and the final product is a financial statement。

Process:

(1) registration of initial information on the financial campaign with original documents

(2) preparation of accounting vouchers

(3) information entry book

(4) four notes in statement i (balance sheet, profit statement, cash flow statement, change in ownership interest statement and notes) are issued periodically。

7. Financial reporting objectives

(1) providing useful information for decision-making:

Provide neutral and impartial information to users of financial reporting information。

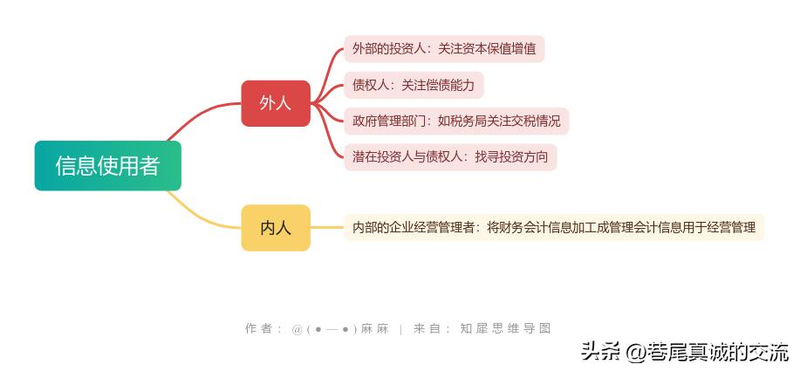

Users include:

External investors (concerning value added for capital)

Creditors (concerning solvency)

Potential investors and creditors in government administrations (e. G. Tax authorities concerned with tax payments) (seeking direction of investment)

Internal business managers (processing financial accounting information into management accounting information for operational management)。

(2) reflecting the performance of fiduciary responsibilities

The separation of ownership and operating rights of the property of a modern equity limited liability company is the responsibility of management to the board of directors for the presentation of financial statements reflecting the financial position, results of operations and cash flows during the management period, as a statement of assignment。