Wen-bank of commerce and industry, china

Summary: against the backdrop of an era of high-quality economic development in synergy with financial risk management, the effective disposal of adverse human assets has become a key issue for sound business and sustainable development of commercial banks. This paper draws heavily on the “tripleization” (resource asset assetization, asset securitization, financial leveraging) model explored by hubei province in the context of state-owned “triple capital” (resource assetization, asset securitization, financial leveraging) reform, and the practical wisdom of “feasibility, non-sale, rent-free” to try to transfer its core logic creatively to finance. The article system has built a process-wide disposal programme that covers value discovery, value transformation and value magnification. The programme responds closely to the policy call of the financial regulatory authorities for the “rich disposal of resources and means”, focusing on the fundamental mission of the banking sector to service the real economy and stock-taking of financial resources, taking into account the latest developments in financial regulation, and being theoretically forward-looking and practical, with the aim of providing a practical implementation blueprint for commercial banks to address the credit risk of stock, optimize asset structures and move towards light asset operations。

Keywords: disposal of undesirable assets; trimination; operation of special assets; securitization of assets; financial engineering

In the new situation, the strategy for the disposal of the bank's personal assets was shifted

As our economy fully moves from a high-growth phase to a high-quality development phase, the deepening of the economic structure is intertwined with cyclical fluctuations in the internal and external environment, which exposes commercial banks to unprecedented complexities and serious challenges in asset quality management. It is noteworthy that the adverse rates of personal consumer loans and credit card loans have fluctuated and that risk management for this sector has become an important variable affecting the soundness of the financial system as a whole。

The risk characteristics of an adverse human asset are quite different from those of a traditional public asset: a relatively small amount of a single-household default, but a large total stock; a highly dispersed and geographically distributed debtor; highly uncertain and volatile future cash-flow recovery; and high costs of collection and disposal from traditional manpower and significant economies of scale. These characteristics have led to long-term dependence on man-made tactics and single-collective traditional disposal models being mired in “minority gains”, as evidenced by “three failures”: the failure of efficiency, a high percentage of artificial collections, and per capita effectiveness reaching the ceiling; the failure of efficiency, a consistently low cash collection rate, a rising percentage of passive write-offs and a direct erosion of current profits and core capital of banks; and the failure of effectiveness, the difficulty of simple collection techniques to match the debtor's wide range of causes of default, and the lack of a tactical toolbox to refine the willingness and ability to pay back and to implement differentiated responses。

In the face of this systemic dilemma, the banking sector is in dire need of a profound cognitive innovation: personal non-performing loans must be redefined as “special assets” that have the potential to survive, to operate and to recover value through transactions, from the “static loss” and the “cost centre” of pure resource consumption, which are in dire need of write-off. This fundamental conceptual shift is the starting point for moving the bad asset disposal model from tradition to modern and from broad to fine strategic premises and logic。

"tripleization" reform in hubei

As the banking sector seeks to break down its path in the area of the disposal of bad assets, the hubei province's “triple capitalization” model, which has been developed in the course of deepening the state's “triple capital” management reform and promoting the construction of a large financial system, provides a strategic inspiration and a very useful methodological approach to asset-taking in the financial sector。

The reform practice in hubei province is based on three principles: “all state resources shall be capitalized to the extent possible, all state assets shall be securitized to the extent possible, and all state funds shall be leveraged to the extent possible” and science shall apply the four operational methods of “useful, non-sale, rent-free and settlement”. This reform is aimed at bringing about a profound transformation of the state's “three capital” across the province, from decentralization to centralized operation, from sleeping resources to living assets, from static assets to working capital. Public data show that, as of september 2025, hubei province, through systematic clean-up and mobilization, has over $21. 5 trillion in state-owned “three-dollar” assets, and the city of wuhan alone has an inventory of assets in excess of $200 billion, directly generating income of $111 billion, effectively achieving the comprehensive policy goal of “mapping homes, inventorying, resolving debts and promoting development”。

An in-depth analysis reveals a strong resonance at the bottom of the logic between the “triggered” reforms in hubei province and the disposal of poor personal assets by commercial banks. The central propositions that both face together are how to address large amounts of resources (assets) that are idle, settling or inefficiently used; how to transform the built-up “sink costs” into “productive capital” that can re-engage in the cycle; and the key to their success is the ability to ultimately optimize resource allocation efficiency and increase overall value through system value discovery, sophisticated value transformation and effective value magnification。

Support and guidance at the national level for the management of innovation

The innovative orientation of financialization of local reform experiences is highly consistent with current financial policy orientation at the national level. A series of policy documents issued jointly by relevant sectors also create an enabling environment for innovation. For example, a number of measures to support the financing of micro-enterprises, published jointly by the directorate-general of financial supervision and eight others, suggested that a modest increase in the list write-off ceiling for small micro-entrepreneurs could be achieved on a pilot basis, which in essence provided a policy tool for the rapid liquidation of related non-performing loans. Seven departments, including the people's bank of china, have also explicitly encouraged banks to increase the disposal of non-performing loans through various means, such as reorganization and transfer, in their guidance on financial support for new industrialization. These intensive policies, echoing the concept of marketability and diversification advocated by the “triple” approach, constitute the current window of pro-poor policies to advance innovation。

Specific application paths for a “triple” approach in a bad loan disposal

Based on the absorption and transformation of hubei's experience with reform of the “triggered” economy, we are trying to build a complete, operational programme for the disposal of the personal assets of banks. The programme follows the progressive logic of “assetization-securitization-leveraging” and aims at full-process excavation and enhancement of the value of undesirable assets。

Assetization — from poor claims to precision farming of special assets

Assetization is the cornerstone of all subsequent disposals, and its objective is to achieve “bridging” of lower-level assets through a refined classification and assessment of “special asset packages” with different risk-return characteristics and disposal strategies。

Data driven value discovery. It is necessary to break down information on internal customer credit data, repayment flows, collection records, etc., and to integrate effectively with external data (such as social security, justice, consumer behaviour, etc.) that are introduced subject to legal compliance. On this basis, a two-dimensional assessment model of “willing to pay—payability” has been developed, using mature machines to learn algorithms to map the debtor with precision. The model should be continuously and iteratively optimized to ensure the accuracy of the projections of potential repayments by clients and to provide a scientific basis for classification。

Precision stratification and differentiation strategy. Based on the output of the assessment model, the debtor could be broadly divided into three categories and applied to a very different disposal strategy。

Category a (reparable assets): refers to customers who are more willing to pay but have defaulted because of temporary difficulties (e. G. Unemployment, illness). The centrepiece of the disposal strategy is “rehabilitation”, drawing on the concept of “use versus use” to help clients recover their performance through debt restructuring, step-rate relief and “test period”, with the objective of achieving long-term value restoration for assets。

Category b (negotiable assets): refers to customers who are volatile in their willingness to pay but can be directed through external intervention. The centrepiece of the disposal strategy is “transformation”, drawing on the concept of “sale without need” and achieving medium-term cash recovery of assets by introducing third-party authorities or service providers, such as financial mediation centres, trade associations, psychological counselling, or by transferring them to professional institutions at a discount。

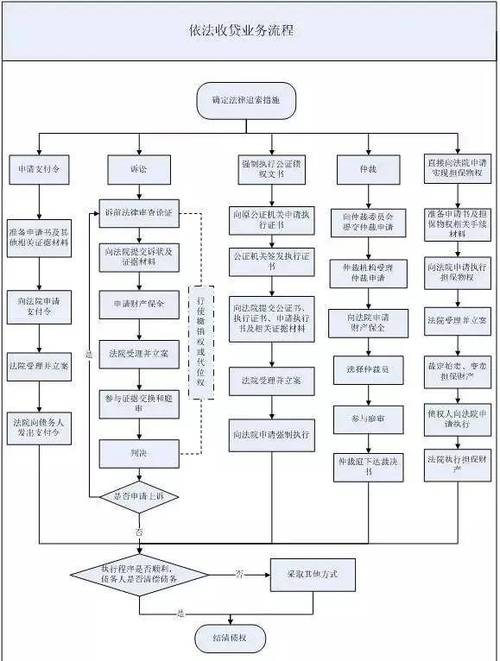

Category c (assets to be disposed of): refers to customers who have no will to pay or who have completely lost their connection. The centrepiece of the disposal strategy is “quick exit”, drawing on the idea of “no-sale, no-sale, no-sale” and preparing for subsequent bulk transfers or securitization through standardization, wholesale litigation, claims packaging, etc., with the aim of preventing further deterioration of asset values and achieving rapid realization。

Securitization - marketized exports through value

Securitization is a key link in the value leap in the disposal process, with the objective of packaging dispersed, non-targeted adverse claims and designing standardized financial products with a steady cash flow expectation, thus opening the way to capital markets and creating risk diversification, transfer and liquidity。

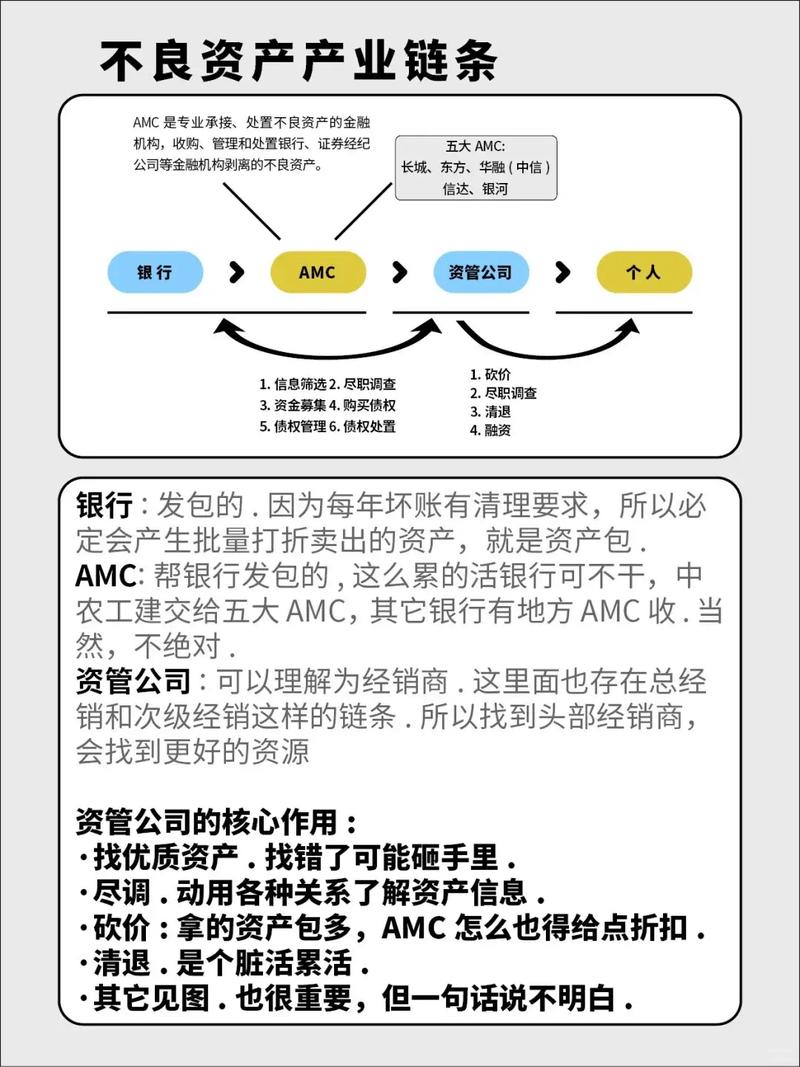

Increased effectiveness of bulk transfers. For classified category c and some category b assets, asset packages may be formed in accordance with regulatory requirements for open transfers on platforms such as the silver landing centre. Price-fixing mechanisms need to be innovative, combining methods such as cash-flow discounts, historical recovery rate analysis, and drawing on the transparent experience of the hubei reform of “a mapping, set of tabulations” and, where necessary, introducing third-party valuations to increase attractiveness to buyers such as asset management (amc)。

Assets support the innovative design of abs. This is a more forward-looking path to value realization. For example, a stable future repayment cash flow resulting from the restructuring of category a clients could be used as a base asset, with the issuance of “a bad loan restructuring abs”, which would be tantamount to the early translation of future uncertain recovery into firm current sales revenue. Product structure design is essential to attract investors with different risk preferences, such as bank finance and insurance finance, through internal credit enhancement measures such as priority/subsequent layers, setting up of excess spreads accounts, cash reserves and the introduction of external guarantees。

Frontier securitization path explores. In addition to the above, more innovative forms of securitization could be explored. For example, in the case of high-quality adverse assets with collateral, “reorganization of equity securitization” could be explored, i. E. By raising the value of assets by debt-to-equity swaps before securitization of equity gains. Single-household securitization or hierarchical securitization may also be attempted, depending on the amount and characteristics of the asset, to meet the investment needs of a more disaggregated market。

Leveraging — building an open-cooperative disposal ecology

At the heart of leveraging lies the transformation of the role of the bank from a direct, isolated “receiver” to a “finance provider, rule-maker and eco-integrator” that leverages external capital and professional capacities to multiply the efficiency of disposal by building cooperative “ecological alliances”。

Capital leverage: the establishment of an adverse asset disposal fund. Banks, in conjunction with local asset management companies, professional law firms, technology companies, etc., can launch a limited partnership fund for the disposal of adverse assets. Banks can act as poor and backward financiers and attract social capital as a priority. The fund acquires asset packages from banks at a discount and entrusts them to the most specialized cooperating institutions, with the proceeds being distributed as agreed. This model builds on the experience of hubei's “fiscal capital extraction”, allows for rapid return of bank funds and increases overall recovery rates through specialization。

Science, technology and eco-leveraging: building new paradigms for intelligent handling. Technology is the key multiplier. An ai smart-receiving platform should be built to achieve automatic matching of strategies, use relationship mapping techniques to increase failure rates, and use block chain techniques to ensure full process memory of the collection process to enhance compliance. At the same time, the establishment of an open cooperative ecological network that integrates a variety of professional forces, such as legal aid, psychological counselling, job placement and data services, provides targeted services to different categories of debtors, removes fundamental payment barriers and increases the level of precision and human care in disposal。

Risk control and regulatory compliance: a sound foundation for innovative business

In actively advancing the “triple” approach to innovation, it is important to maintain the risk threshold and compliance requirements at all times to ensure that innovation takes place within a prudent and robust framework。

(c) maintaining compliance and consumer rights protection floors. The “sun-shine disposal” requirement must be strictly enforced and disposal programmes, fee-paying items should be clear and transparent, and any hidden costs eliminated. The act of collection must be strictly regulated by law, violence, harassment and other means of violation must be strictly prohibited, with full respect for the dignity and legitimate interests of the debtor. Throughout the use of data, strict compliance with laws and regulations, such as the personal information protection act, and the establishment of a rigorous data security management system, particularly in cooperation with third parties, must be accompanied by technical means, such as binding agreements and data dissensitization, to prevent the disclosure of customer information。

A multi-level risk-control system is built. Models need to be put in place for a life-cycle management system that periodically validates the accuracy and fairness of assessment models and protects against “calculatory discrimination”. In applying the leverage strategy, the level of leverage is reasonably controlled to ensure that it matches the bank's own risk tolerance. For securitized products, adequate stress testing is required and mechanisms such as liquidity support is designed to address market volatility risks. At the same time, social responsibility should always be maintained to provide reasonable relief programmes for debtors who have difficulties, to enhance financial literacy and to effectively manage reputational risks。

Active communication and policy synergy. Before introducing innovative disposal tools, banks should proactively communicate with financial regulators to gain understanding and guidance, and apply for inclusion in the “supervisory sandbox” pilot if necessary. At the same time, full use should be made of existing policy dividends, such as obtaining tax incentives, simplifying the process of approving innovative products and actively promoting the establishment of cross-sectoral coordination mechanisms to address practical challenges in dealing with them, such as laws and taxes。

New paradigm towards the disposal of adverse bank assets

Applying the systemic thinking and operational wisdom of hubei's “triggered” reforms to the disposal of poor personal assets by commercial banks is essentially a profound paradigm revolution. It requires banks to move beyond the single role of traditional credit institutions to a shift towards “special asset operators” and “financial ecological resource integraters”。

Recall the application value of the “triggered” path: “assetization” achieved a shift from passive write-off of losses to active operating value, with potential value being tapped through precision farming of assets; “securitization” achieved a shift from passive holding to active trading and spreading of risks, and the re-engineering of liquidity and pricing mechanisms for assets through financial engineering; and “leveraging” achieved a shift from single-handedness to ecological synergy, leveraging broader social resources and professional capabilities by building open alliances。

The significance of this innovative path lies not only in helping banks to mitigate their own stock risks and optimize their financial statements, but also, more deeply, in the micro-empowerment and practicalization of the macro-strategy of financial services economy and prevention of systemic financial risk, through a systematic inventory and reallocation of financial resources that are deposited in bad forms, into the blood cycle of the real economy. As shown in hubei province's reform practice, the depth of inventory of resource assets is a key underpinning in addressing current development and risk challenges. By the same token, for the banking sector, the construction of a modern system for the disposal of poor assets based on the “triple” approach is a necessary option and a key step in improving the efficiency of financial resource allocation, a sound business base and a high quality of service development。