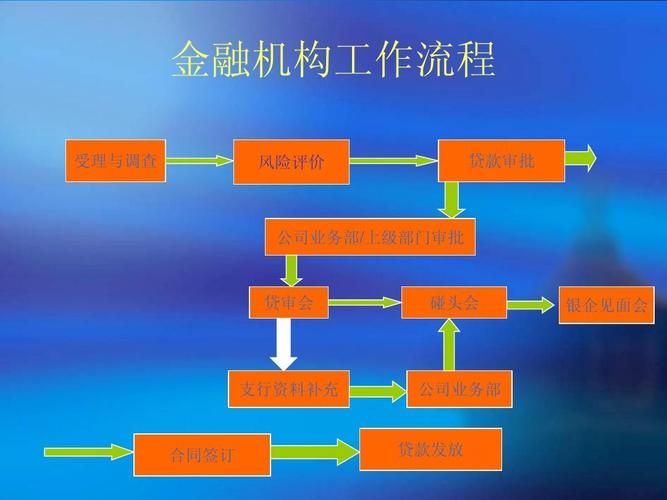

The concept of a loan is a form of credit activity in which a bank or other financial institution lends monetary funds at a certain rate of interest and subject to restitution. Loans are broadly defined as loans, discounts, overdrafts, etc. Banks can also obtain interest income on loans to increase their own accumulation, by releasing money and money from the pool, thereby meeting the needs of society to expand reproduction for supplementary funds and promoting economic development. The framework document for the loan operations, the interim scheme for the management of liquidity loans, the interim scheme for the management of individual loans, the interim scheme for the management of fixed assets loans and the operational guidelines for project financing, also known as the “three approach one guides”, initially set up and refined the legal framework for the operation of loans by our banking financial institutions. Loans: personal business type loans; personal consumption type loans; mortgages; mortgages for housing (commonly referred to as mortgages); mortgages for second-hand houses; mortgages for commercial housing (some banks classify such loans as operating types); loans for second-hand rooms; loans for second-hand rooms; loans for automobiles (including cars and commercial cars, some banks classify commercial car loans as operating-type loans); loans for second-hand cars; loans for second-hand cars; loans for second-hand cars; loans for other consumer goods; loans for renovations; loans for durable consumer goods; loans for hostage-type mortgages; physical persons or legal persons or their representatives - corporate entities, corporate corporations and other economic organizations or their heads (partnerships, individual solety enterprises); concepts for bank loans; concepts for the loan business; interest rates: interest rates on loans, which refer to the amount of interest over the period of the loan and the proportion of this amount. Our interest rates are administered centrally by the people's bank of china, and the rates set by the people's bank of china are implemented with the approval of the state council. The latest interest rate provides for an upward adjustment of the base rate on loans held in the renminbi by financial institutions, effective 7 july 2011. The benchmark interest rate on one-year loans held by financial institutions was increased by 0. 25 percentage points. The annual interest rate on loans % 6 months 6. 10 1 year 656 1 year 3 year 6. 65 3 year 5 year 6. 90 5 years and more 7. 05 year size of credit: also known as loan size, is an indicator of the central bank's pre-defined control of bank loans to achieve monetary policy objectives for a certain period. It has two layers: (a) the total loan balance at a given point in time, i. E. The total stock; and (b) the increase in loans over a given period. The size of the loans referred to here refers mainly to the latter, which refers to the maximum amount of new lending set for the achievement of monetary policy objectives over a period of time, also known as the total loan limit. The deposit reserve is a deposit in the central bank prepared by the financial institution in order to secure the withdrawal of funds from its clients and the liquidation of funds, and the proportion of the deposit reserve required by the central bank to its total deposits is the deposit reserve rate. The current rate is 21 per cent. The process of bank credit. If the borrower needs a bank loan, he or she must submit a written application to the bank or its operating agency to complete the loan application. The application shall include the amount of the loan, the purpose of the loan, its capacity to repay and the manner in which it is repaid. Bank approval, including setting, credit rating assessment of borrowers, feasibility analysis (the analysis of the financial position of the enterprise is of the utmost importance as it is the basis on which the bank masters and judges its ability to repay)*