This report is based on a platform for american data-based research — a sample of nearly 1,000 valid questionnaires collected in several rounds of app — which combines industry sales data with consumer behaviour analysis, and is designed to provide practitioners with comprehensive market insight. Research has shown that while there was a marked decline compared to 2023, the market, driven by emerging demand for sensitive muscles, anti-age, etc., is showing strong warming momentum and is expected to usher in a new growth cycle in the future. In the current context of rational consumption in parallel with the refinement of demand, industrial competition is shifting from a new phase of expansion of scale to a new phase of quality upgrading。

I. Industry insight: in structural adjustments, consumption rankings coexist with demand upgrading

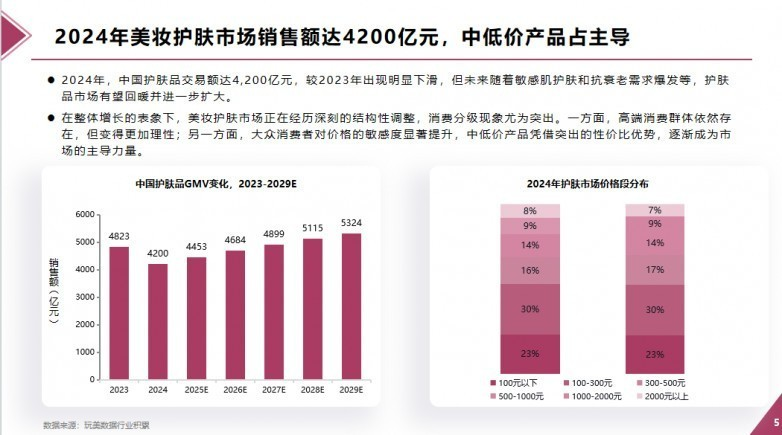

In 2024, the core of the industry was characterized by fragmentation and adjustment. Markets are undergoing profound structural adjustments, especially with regard to the classification of consumption. On the one hand, high-end consumer groups still exist but become more rational; on the other hand, the sensitivity of mass consumers to prices has increased significantly, and low- and medium-price products have gradually become dominant in the market by virtue of their prominent value for money advantage。

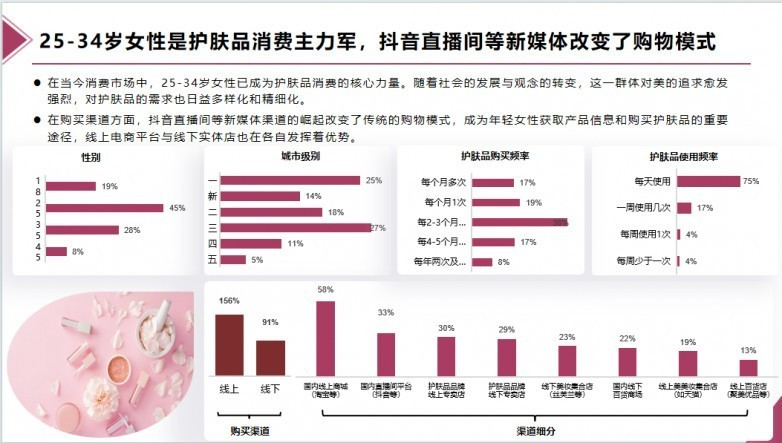

Consumer behaviour shows an important trend towards reshaping industry patterns. In terms of channels, the rise of new media channels, such as the live vibrate, has changed the traditional pattern of shopping and has become an important means for young women to access product information and to purchase skin protection. The proportion of women aged 25-34 who have become central to skin-care consumption is 45 per cent, and the demand for skin-care in this group is increasing, and expectations of skin-care products are becoming more diverse and refined. In terms of product demand, there is a high rate of basic skin permeability, with the higher the urban level, the greater the demand for advanced products, a high trend towards the high end of the whole range of demand for skin-care products in the first-line cities and a significant advance in the penetration of advanced products such as fine and eye cream。

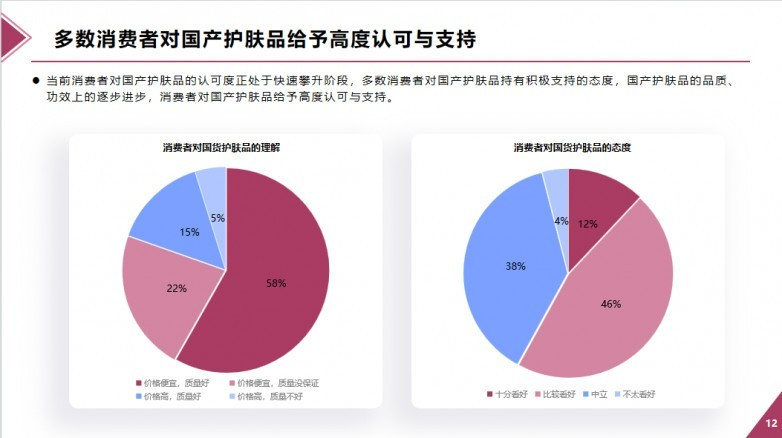

In terms of brand competition patterns, international brands continue to dominate the head, with 68 per cent of consumers thinking first of the european-american brand and only 38 per cent of consumers thinking first of the national brand. The european and american brands have a strong image and a high penetration rate because of their deep and diverse layout. However, the majority of consumers have a high level of recognition and support for domestic skin protection, and the gap between some national product plates and european and european brands is narrowing. Prices are too high and less effective than expected to be the main point of pain for brand consumers in europe and the united states, while poor performance and susceptibility to allergies are the main point of pain for national product card consumers。

Consumer interpretation; demand differentials are inevitable

There are significant differences between women of different ages in terms of skin demand, consumption capacity and brand preferences. Of the 18-24 age group of women, 81 per cent are single, have a weak overall consumption capacity and are concentrated in having to satisfy themselves in small amounts. Fifty-four per cent of the respondents used skin care on a daily basis, while 52 per cent purchased skin care every two to three months, with the main route being online。

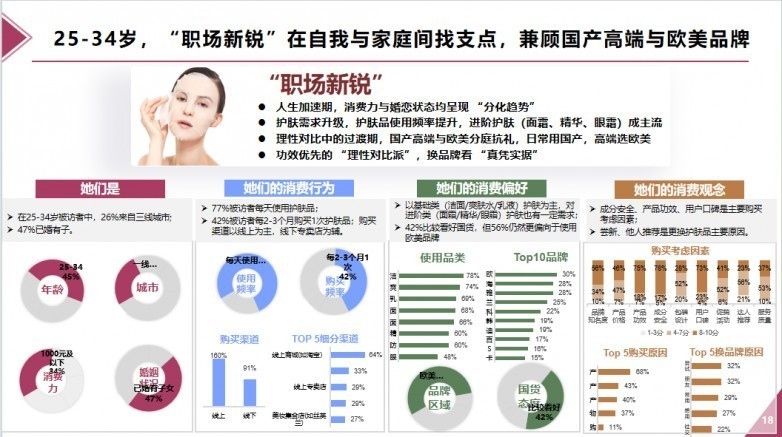

The group of women aged 25-34 is at an accelerated stage in their lives, and there is a tendency to differentiate between consumption and marriage. Of those interviewed in this age group, 47 per cent were married, 77 per cent used skin-care items every day and 42 per cent purchased skin-care items every 2-3 months. While 56 per cent of respondents preferred the european and american brands, 42 per cent preferred the national product。

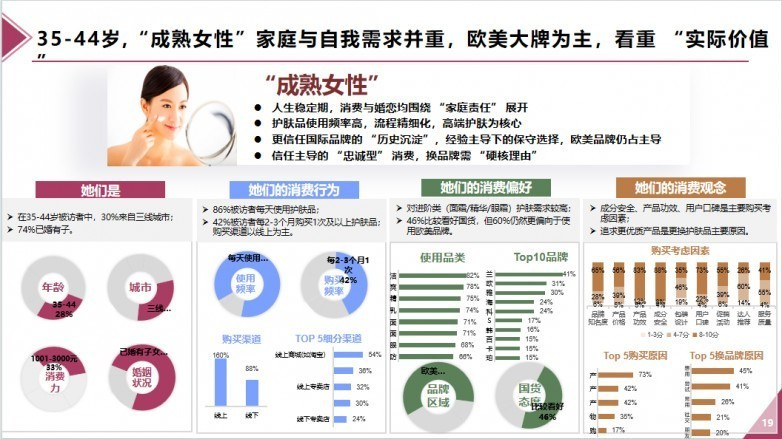

The group of women aged 35-44 years entered a life-stable period, with consumption and marital relationships surrounding family responsibilities. Of those interviewed in this age group, 74 per cent were married, 86 per cent used skin-care items every day and 42 per cent purchased skin-care items every 2-3 months. While 60 per cent of respondents continued to favour the use of the european and american brands, 46 per cent preferred the national product。

Iii. The between the business: the emergency of the negotiations respects to producing initiatives

National product plates are moving from the value-for-money dividend phase to the value competition phase, requiring a synergistic upgrading of product and marketing power。

1. In terms of product upgrading dimensions, national skin care products are undergoing systematic upgrading in terms of components, concepts, technologies and efficacy. In terms of components, the head country brands break the inherent impression of "difficult national production" through autonomous research and development of patent components; in terms of ideas, the creation of a unique brand culture through deep exploration of eastern skin-care wisdom to improve visibility; in terms of technology, the efficiency and stability of the extraction of components through greater r & d inputs; and in terms of effectiveness, the development of accurate research on the skin of the nation's population to make the product more relevant and effective in terms of its core efficacy, such as wetting and anti-degeneration。

2. In terms of the construction of marketing systems, full-source marketing can help to reach a wider audience for national skin care and enhance brand penetration and user viscosity. The front-country brand uses an all-channel grass strategy in electrician layouts, with live delivery through the brand's self-broadcasting, kol live broadcasting, and the posting of headrooms, while using social media platforms for deep content seeding. In emotional marketing, brands focus on women's issues and are widely recognized through attitude and in-depth expression, and export brand values. Stars and cross-border coalitions have also become effective ways to raise brand heat and product exposure through the selection of youth-friendly flow stars as advocates, as well as with popular ip。

The cosmetics sector is at a critical stage in the opportunities for productive change, with consumption rankings, the rise of national goods and technological innovation becoming central drivers of industry development. The report is based on american data. We are a service that focuses on market research and data analysis and is committed to helping brands to capture consumption trends and achieve sustained growth through scientific and professional data insights. These are only partial excerpts from the report, and if you need to get a full version of the comfort 2025 consumer report, we will provide you with the full text in a timely manner, as well as the attention given to the [american data] public number, the personal contact name and contact + the key word。

This is an original article and, if reproduced, please indicate the source of the latest publication of american data: insight of the consumer of the make-up 2025 and the new growth of the national brand https://news. Zol. Com. Cn/1066333164. HTML

Https://news. Zol. Com. Cn/106633364. HTMLnews. Zol. Com. Cntrue online https://news. Zol. Com. Cn/106633364. HTMLreport 3470, based on a platform of home-made research on american data — a sample of nearly 1,000 valid questionnaires collected in several rounds of app, combined with industry sales data and consumer behaviour analysis, aimed at providing full market insight for practitioners. Research shows that sales in china’s american cosmetics market amounted to $42 billion in 2024, although there was a marked decline compared to 2023, but pushing emerging demand for sensitive muscle care, anti-age...