“if finance is not business-wise, it is accounting, not finance.”

This sentence, rightly speaking, breaks the core of financial integration。

In reality, the perception of “financial understanding of business” is biased:

(a) business perception of non-reimbursement and co-operation

Financially thought it was a line of sight and a contract

The management considered the additional meetings to be integration。

These errors keep the finance locked in a “post-entry” cage, unable to truly embed operations and create value。

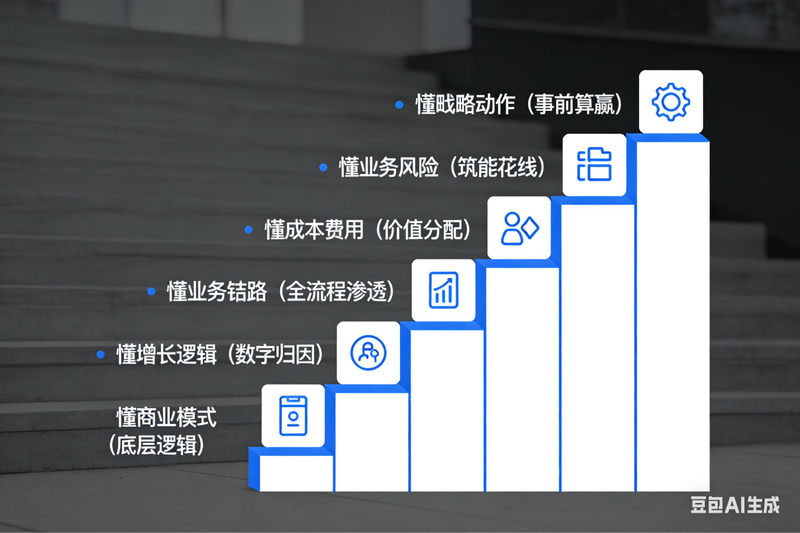

A true understanding of business is the use of financial data to visualize the nature of business, to match financial decision-making with business needs and to find a balance between control and support. This paper dismantles the financer's “seven understand” approach and gives an operational growth path from mr. Accounts to business partners。

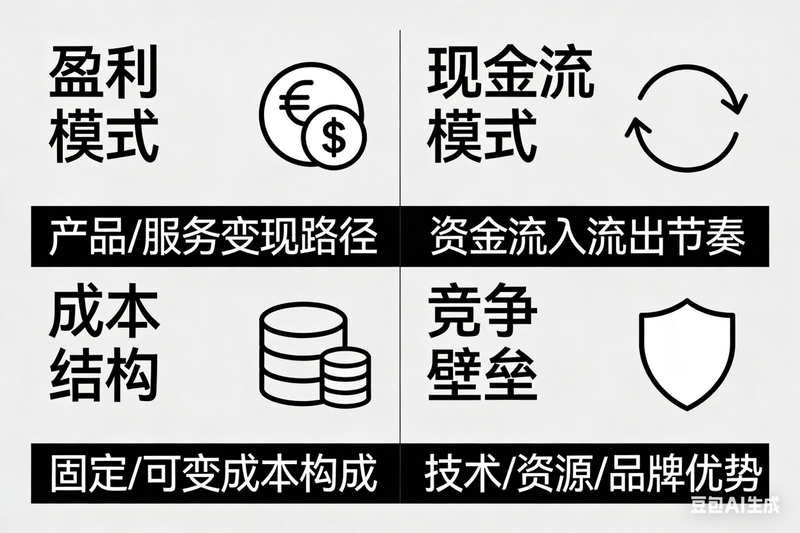

I. Understanding business models: understanding the bottom logic of companies making money

Not knowing business models, all financial data are soulless figures. Financially, the bottom code of the company's profits is broken, and the core is at four dimensions:

1. Profit patterns: where does money come from? Whether it's departure (sizing size, lowering marginal costs), premium (based on branding, differentiation), turnover (asset efficiency), subscription (retention, life-cycle value) or ecology (based on platform, network effect)

- example: china looks at the project's maori, payback cycle for the operator's business; catering companies look at single store maori, rate of loss; internet enterprises look at paid users, rate of renewal。

Cash flow patterns: how does money flow? Do you take the money and work, or do you take the money? What is the pace of payments between customers and supply chains

- for example: china has advanced money for the tob project and has been slow to pay back, and the finance needs to measure the cost of the funds in advance and provide early warning of the payments。

3. Cost structure: where is the money spent? :: depreciation of heavy raw materials, equipment for manufacturing; heavy manpower, project implementation costs for tob service enterprises; re-acquirement of internet enterprises, r & d costs。

4. Barriers to competition: how to keep money? Is it technology patents, exclusive resources, brand premiums, or costs, channel advantages

Core: understanding the origin, destination, profit logic and retention capacity of money to anchor financial data in the nature of business。

Ii. Understanding business growth logic: seeing business actions from digital fluctuations

It is a typical expression of financial ignorance of the business to say, “failure to meet the standards and decrease in the gross domestic product”, without any explanation. Behind the fluctuations in performance are the results of business operations, where finance establishes a “business action-based financial outcome” counterpart:

1. Dismantling sources of growth: does the growth come from new customer development, repurchase by older clients, new product breakthroughs, old product price increases/disbursements, regional/industry expansion? Correspondingly, attention needs to be paid to indicators such as cost of access, retention rates, and plentiful new products。

Business tempo: there are different rhythms in different industries, such as tob enterprise q1 reserve business, q2-q3 delivery, q4 repayment, which require financial attention to be adjusted on a quarterly basis。

3. Attribution of performance fluctuations: distinguishing between controllable internal factors (sale movements, quality of delivery, cost control) and external factors subject to prejudgement (policy, competition, raw material prices, economic cycle)。

Core: do not do digital microphones, do business action analysts and find the root causes of data fluctuations。

Iii. Understanding the business chain: financial penetration from clues to refunds

Finance is not required to master operational details, but to understand the financial logic of each link and achieve full chain financial empowerment, from clues to repayments. In the case of tob operations, the financial value points for key links are clear:

Business, finance

Thread acquisition, client cost, lead quality, accounting channel roi, optimize channel layout

Follow-up business opportunities, follow-up cycles, costs, success rates, account for unit costs, optimize business opportunities strategies

Cost accounting and formulation of a reasonable pricing strategy

Financial implications of contract terms participation in contract evaluation and avoidance of financial risk

(c) optimizing cost structures and improving delivery efficiency

Receiving and inspection standards, billing nodes, payment rhythms, reducing bad debts, accelerating the return of funds

After sale, after-sale cost drivers, impact on repurchase, control after-sale costs, help product optimization

Core: embedding financial controls into the business-wide process, enabling, monitoring and not ex post facto accounting。

Iv. Understanding the structure of profit: seeing who makes money and who burns money

Looking at corporate profits alone is a major shortcoming in financial analysis. With limited resources, it is important to favour high-profit, high-growth products, clients, regions and finance with three dimensions:

Product dimension: analysis of the revenue/māori ratio, māori rate, life cycle phase of each product, distinguishing between cash cattle, stars, problems, thin dog products, suggesting trade-offs or optimization。

Client dimension: distinguishing quality clients (high māori, high payback, short term, low maintenance costs) from poor quality clients by industry, size, years of cooperation, etc., to guide business precision services。

3. Regional dimensions: identification of areas with high potential (increased inputs), mature areas (optimization of stocks), inefficient areas (considering abandonment) and optimization of resource allocation。

Core: let financial data guide resource allocation and spend it where more money can be made。

Understanding the business substance of costs: not just control, but empowerment

It was a low-level financial error to see cost increases demand reductions. The finance needs to tie costs to business operations to understand the value of each penny:

1. Dismantling drivers: travel costs correspond to client visits, channel fees correspond to sales, r & d costs correspond to the number of projects, raw material costs correspond to production and loss rates。

Assessing the ratio of inputs to outputs: whether it is an effective input, regardless of how much it is spent, how much money it can generate, and how much māori growth it is。

3. Distinguishing types of inputs: strategic inputs (short-term no returns, long-term core competitiveness) look at long-term values; operational inputs (short-term returns, maintenance of day-to-day operations) look at efficiency and value for money。

Core: cost control is not “one size fits all”, but rather a distinction between effective and ineffective inputs, enabling operations to spend reasonable money and create value。

Understanding operational risks: the “firewall” for doing business

One of the core values of finance is that the nature of the business is to flush performance, to maintain the risk threshold, to identify the financial risks behind business operations and to perform four types of controls:

1. Refund risk: avoidance through the establishment of a customer credit rating and participation in contract evaluation due to customer credit differentials, long term accounts and unclear terms。

2. Profitability risk: as a result of low-priced bids, out-of-control costs and delivery back to work, which is resolved through price accounting, cost monitoring。

3. Compliance risk: prevention through the establishment of a compliance system and the regulation of processes, as a result of false billings, false charges, contract non-compliance。

4. Operational risk: loss reduction through pre-judgement of financial impact and development of response measures due to insufficient capacity, stock backlogs and supply chain fractures。

Core: become the “firewall” of operations to support quality and safe growth rather than blind performance。

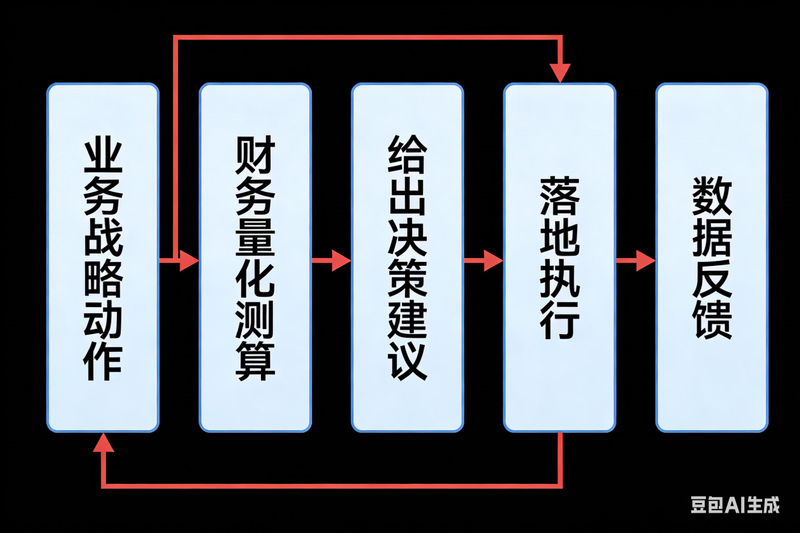

Strategic action to understand business: from “post-accounting” to “win-win”

The highest level of financial integration is financial participation in business strategy decision-making to achieve “pre-win” with three main competencies at its core:

1. Feeding strategies: understand the purpose of corporate long-term strategies, annual strategies and business sector strategic actions。

2. Quantification of impact: translating business strategy actions into financial indicators that accurately measure financial consequences。

- example: business offers a 10 per cent discount, and the financial needs measure the insured sales, the change in the gross domestic product, the impact of cash flows and long-term market returns。

Provide policy advice: avoid empty words such as “prudential decision-making” and, in conjunction with measurements, give concrete reductions, offset targets and cost-control recommendations。

Core: upgrade from strategic implementer to decision partner, with data support and financial security for each business strategy。

Concluding remarks: the financial “seven know” road to progress

Finance is business-friendly, not as a substitute for business, nor as a word of business, but rather as a professional enabler of business, allowing financial and operational resonance。

“seven understand” is a complete framework for growth:

- understanding business models, growth logic as the basis for understanding the nature of business

- understanding the whole business chain, the profit structure is the core, allowing you to deepen value creation

- understanding costs and operational risks is key to balancing control and empowerment

- understand strategic action is promotion, making you business partner。

There are no shortcuts to this road, and it will require financiers to sink into the business landscape and create business value with finance expertise. When you truly understand business, finance will no longer be a “trainstone” to business, but the most trusted partner。

Self-measurement and thinking

What did your financial team do in seven

Initial phase (1-2 understand): largely at the accountancy level

Growing up (under 3-4): starting to understand business but with limited participation

Adultity (under 5-6): deep engagement, operational partner

Excellence phase (7 understood): participation in strategic decision-making, driving value creation

A “understand” could be chosen as a breakthrough point, starting from a small point and moving gradually from accounting to business partners。

Interactive topic: what do you think is the hardest thing about finance? Welcome to the comment section