(attached as figure 1)

1 overall increase in deposits

First, the monetary supply perspective. At the end of november, the m2 balance stood at $33. 699 trillion, an increase of 8. 0 per cent over the same period, at a more stable rate than in the preceding period. The m1 balance of rmb 11,289 trillion, representing an increase of 4. 9 per cent over the same year, began to decline after the increase continued at the end of the first three quarters of the year (a new m1 calibration was introduced in january 2025). The balance of m0 was rmb 13. 74 trillion, an increase of 10. 6 per cent over the previous year。

Second, the overall perspective of deposit. At the end of november, the foreign currency deposit balance was $33,446 trillion, an increase of 8. 0 per cent over the same period; of this, the rmb deposit balance was $32,696 million, an increase of 7. 7 per cent over the same period, which was lower than in the second and third quarters of the year (see annex, figure 2 for details). The net increase in rmb deposits over the previous 11 months was $24,73 trillion, an increase of $5. 34 trillion over the same period。

In terms of quarterly increases, in 2025 there was a net increase of 12,97 trillion yuan in the opening of red rmb deposits in the boom season, an increase of 17,26. 3 billion yuan over the same period; a net increase of 495 trillion yuan over the same period, an increase of 47,39 billion yuan over the same period; and a net increase of 476 trillion yuan over the same period. A combined net increase of $202. 1 billion in october and november was $74. 46 billion。

Without regard to other factors, it is projected that if the rmb deposits are reduced to about 7. 4 per cent by the end of march next year, based on the level of increments for the last three years and recent trends, the increase in open-door deposits could reach about $13 trillion in the quarter due to the larger base figure, equivalent to the average increase in open-door red deposits for the three years 2023-2025。

As a whole, therefore, banking institutions can be more comfortable with the increase in the size of deposits in their marketing for the 2026 season; of course, for institutions with higher loan ratios and higher fluctuations in their front share, a high priority should be given to competitive approaches to open deposit markets。

(attached as figure 2)

2. Growth of deposit structure

First, the savings deposit perspective. At the end of november, rmb had a personal savings balance of $16,331 trillion, an increase of 9. 6 per cent compared to the previous three years; although there had been a decline over the previous three years, the increase in savings had remained at a high level (see figure 3 for more details for calendar years). In the first 11 months, savings deposits increased by a net of $12. 06 trillion, 10. 9 billion less than in the same period the previous year, with a relatively small change in the increase. At the end of november, time savings amounted to 74. 04 per cent, an increase of 0. 70 percentage points over the same period of the previous year。

Second, the business deposit perspective. At the end of november, rmb non-financial enterprises had a balance of 79. 34 trillion yuan, an increase of 3. 8 per cent over the previous year. In the first 11 months, there was a net increase of $0. 97 trillion in business deposits, an increase of $28,67. 3 million over the same period of the previous year (a negative increase in the same period of the previous year). At the end of november, enterprise time deposits accounted for 72. 80 per cent, a decrease of 1. 52 percentage points over the same period of the previous year, showing a certain trend towards “activity”。

In addition, the balance of institutional group deposits was $39. 85 trillion, or 6. 0 per cent over the same period; deposits of “non-soldier” financial institutions were $34. 93 trillion, or 11. 4 per cent over the same period (reflecting the relative dynamism of the capital market); and fiscal balances were $7. 67 trillion, or 5. 7 per cent over the same period。

(attached as figure 3)

3 growth of deposit institutions

First, a large-scale deposit perspective. At the end of november, the balance of rmb deposits in the “seven major lines” was $15. 580 trillion, an increase of 7. 6 per cent over the same period, at a relatively lower rate than the average. In the previous 11 months, there had been a net increase of $1295. 69 billion in “seven major lines”, an increase of $29. 17 billion over the same period the previous year。

Second, the perspective of small and medium-sized banks. At the end of november, small and medium-sized banks had a rmb balance of rmb 14,499 trillion, an increase of 9. 3 per cent over the same period. In the first 11 months, there was a net increase of $10,944. 6 billion in small and medium-sized bank deposits, an increase of $816. 8 billion over the same period of the previous year。

In terms of growth, the savings of small and medium-sized banks increased at a relatively faster rate at the end of november (see figure 4 for more details); in terms of volume, the savings of small and medium-sized banks in the previous 11 months increased relatively slightly, after all, with a smaller base。

Where the average level of interest paid on deposit is significantly lower, a larger share of the increase can be obtained by the business, mainly for two main reasons. On the one hand, more deposits are generated by ensuring a “return rate” of loans after more loans are put in place; on the other hand, lower-cost deposits are generated by securities trading, fund hosting, financial settlements, and the sinking of funds. Although small and medium-sized banks are unlikely to be able to be as “advanced” as large businesses, they should be equally important。

If these two points are taken into account, small and medium-sized banks may gain greater advantage in the competition for deposit operations. For example, at the end of september this year, hangzhou bank and nimbau bank balances were $13,48. 6 billion and $20,47. 8 billion, respectively. This represents an increase of 14. 59 per cent and 9. 87 per cent, respectively, which is significantly higher than the average growth rate of 7. 47 per cent in zhejiang province during the same period。

(attached as figure 4)

4 growth of deposit areas

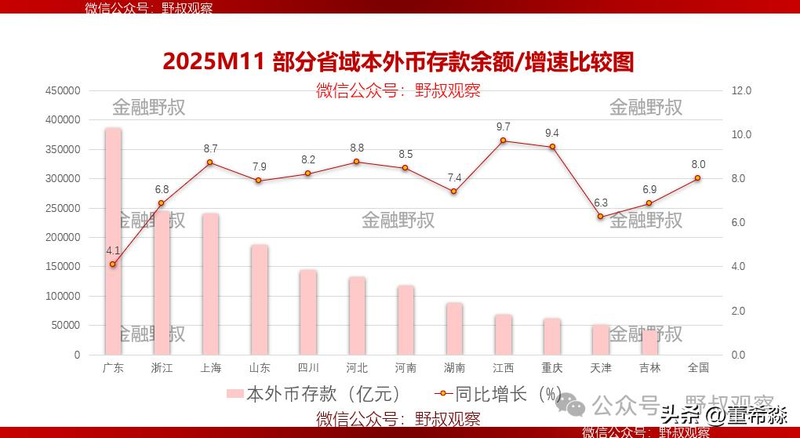

By 19 december, more than a dozen provinces had disclosed financial data at the end of november. In terms of balance, guangdong's foreign currency deposits of $38. 61 trillion still rank first; jiangsu's total deposits may be second (27. 69 trillion yuan at the end of october and data not yet available at the end of november)。

In terms of growth, the balance of foreign currency deposits at the end of november was $6. 77 trillion, a relatively high increase of 9. 7 per cent over the same period. Zhejiang's foreign currency deposit balance is $24. 46 trillion, an increase of 6. 8 per cent over the same period (see figure 5 for details), which is 1. 2 percentage points lower than the national average during the same period; given that the current province-wide loan ratio is over 100 per cent, competition in the deposit market is expected to be more intense in 2026。

(attached as figure 5)

5 changes in deposit rates

After several prior adjustments, the current interest rate on bank deposits and actual interest payments are both historically low. For example, the annual and three-year term savings deposit listing rates of the general state-owned majors in december were 1. 10 per cent (as low as 0. 95 per cent in the third quarter of this year) and 1. 55 per cent, respectively; one of the majors increased temporarily in december to 1. 30 per cent and 1. 60 per cent, respectively. In the second half of the year, the one-year and three-year periodic savings listing rates of 1. 3 per cent and 1. 75 per cent, respectively, were set at a commercial bank in a city and in december a large scale of 1. 80 per cent was introduced。

According to the data of the institute of digital science and technology 360, the average interest rates on one-year and three-year term deposits in september of this year were 1. 277 per cent and 1. 68 per cent, respectively; 28. 9 bps and 35. 4 bps, respectively, were below march (reflecting the current year's level of red payments), with a clear downward trend, after all, of “net interest rates on security” for all types of institutions; compared to june, only a slight downward trend remained relatively stable。

In front of the first line of research, uncle nok learned that the average rate of payment of savings by a county farmer bank in the first three quarters of the year had been controlled at 1. 41 per cent (which had already reached the level of interest payments by major businesses, such as the average rate for bank deposits in the first half of the year, which was 1. 45 per cent), a decrease of 27 bps from the previous year; while the regional market share remained at 41. 7 per cent (first in the county-wide financial institutions). This is a remarkable performance。

In terms of a 10-year rate of return on national debt (deposit rate reference), the level of return since april of this year has shown a moderate upward trend, ranging from around 1. 62 per cent at that time to around 1. 78 per cent by mid-december (see figure 6 for details). The current pressure may be slightly reduced for commercial bank deposit cost control。

Taking into account the above-mentioned factors and the latest practicalities, some institutions, particularly small and medium-sized banks, were likely to experience a phased, low-intensity upward adjustment in the pricing of deposit rates during their 2026 opening hours, especially in the highly competitive regions; but the overall direction of the downscaling efficiency gains will certainly not and cannot be changed。

(attached as figure 6)

Uncle nok's closing remarks

In fact, uncle nou used to write less about the competitive strategy of the deposit business, because after entering a deep aging age in 2021 (the proportion of the population over 65 years of age exceeds 14 per cent), since the consumption of older people and the willingness to save are different from the demand, the personal deposit base will remain relatively high for a certain period of time, although it is already relatively large; after that period savings will begin to be released because of old age needs and intergenerational transmission. The future point of both is likely to be around 2032, largely in line with the time of super-age。

By some coincidence, our rmb savings balance at the end of 2021 exceeded $1 million, eight years after 50 trillion dollars; three years later, however, savings amounted to 151. 25 trillion by the end of 2024. Uncle nobo predicted that, after more than three years (2025-2027), individual savings could exceed $20 trillion in 2028. Thus, the overall size of the opening of the red deposit business in 2026 is largely not critical, but cost management. (this is the view of the author and does not represent the position under the heading)