In its annual strategy for 2021, the starstone presented a “new economic cycle” in which the economy is expected to be sustained or stronger than expected, not just as a rehabilitation after the outbreak, but as a cycle of expansion driven by supply and demand gaps。

What is the production cycle

By law, economists divide the economic cycle into three: the real estate cycle of about 20 years (kuznets cycle), the production cycle of about 10 years (jugra cycle) and the inventory cycle of 3-5 years (kchin cycle)。

The production cycle, also known as the equipment investment cycle, or the guerra cycle, was proposed by the french economist c. Juglar。

The energy cycle is due to a number of factors: internal factors include equipment wear and tear, external factors include demand expansion, technological advances, policies, etc. When the economy as a whole is at the peak of equipment upgrades, there will be more investment in fixed assets that will drive the economy into prosperity。

The production cycle is mainly related to manufacturing, with observations on industrial boiler production, excavator production sales, industrial enterprise capacity utilization, investment in equipment for 5,000 industrial enterprises, value added in the general equipment manufacturing industry, fixed asset investment completion, etc。

In terms of indicators, china's economy is indeed characterized by a productive cycle, and since the opening up of the reforms we have gone through a total of five rotational cycles, 1977-1987; 1988-1998; 1999-2008; 2009-2016; and 2016-present。

Increased supply and demand gap and opening of a new production cycle

Starbite believes that the economy of this round is at the beginning of a new production cycle, far from just the rehabilitation of the epidemic。

Before discussing the current cycle, it should be noted that:

The cycle gives the star stone a sense of location in which to analyse macroeconomic fluctuations, but it does not recommend rotational patterns to judge the future, as they are not driven by the economy, but only a summary of phenomena。

For example, there is no precise pattern of the duration of the life cycle. In the case of china, for example, the energy cycle for 1999-2008 lasted 10 years, of which the previous period lasted 7 years, mainly because of the renewed expansion of the textile sector after the liquidation of the capacity in 1998 and the external demand in the context of our accession to wto at the end of 2001. The capacity cycle for 2009-2016 was about eight years, with a shorter lead period of about two years. Mostly driven by $4 trillion in investment, excess capacity began to come out in 2011。

So cycle patterns can only serve as references. In the light of reality, it is more important to judge the cycle in which the economy emerges。

The production cycle is essentially a demand-driven mismatch between supply and demand。

The reason why the stones judged 2021 to be the start of the production cycle was that, after the expansion of capacity in 2009, a decade of long and thorough production had been achieved, while china’s economy had gone from a high rate of growth to a medium rate of growth, with the demand side remaining weak, so the willingness to invest remained weak. As demand recovers after the epidemic, the capacity gap between the two continues to widen and will drive a new wave of expansion。

Supply end: three long rounds of production are clear and supply is contained

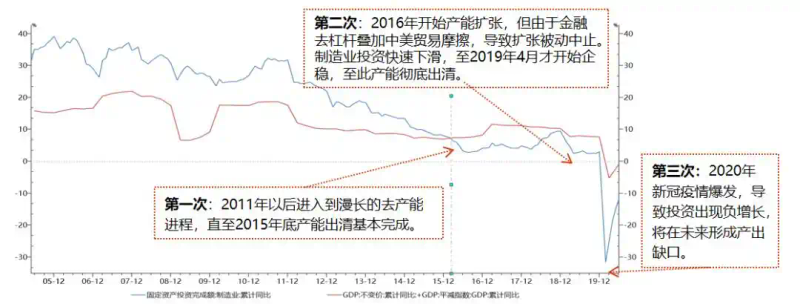

The first round was essentially clear: after 4 trillion billion dollars, since 2011, as the economy slowed down, aggregate demand continued to decline, excess capacity began to be phased out, mainly in traditional industries such as chemicals, paper, glass, cement, steel, coal and machinery, and a large number of small and medium-sized enterprises withdrew and the viable utilization of their productive capacity declined。

In 2016, supply-side reforms and environmental inspectors were launched, and administrative reforms accelerated the production process, which was largely completed in the first round. This round also corresponds to the downfall of the round's capacity cycle from 09 to 16 years。

The second round was completely clear: the financial deleveraging in 2017, the contraction of credit, the decline in business confidence in the context of the us-china trade war in 2018, led to the suspension of the expansion of productive capacity and the rapid decline in investment in manufacturing

Source: wind, starstone investment

The third round was over-clear: the outbreak of the new coronary outbreak in 2020, the temporary freezing of demand, and renewed shocks to business confidence led to negative growth in manufacturing investment and a nearly 10 per cent reduction in industrial capacity utilization, leading to over-surge on the supply side。

It is worth mentioning that the new production cycle should have started in 2016. Indeed, the expansion of capacity began again in the third quarter of 2016, with a small increase in fixed-asset investment performance in the same year and a discussion in the market at that time of the start of a new cycle, but with financial deleveraging and trade wars between china and the united states that led to a halt. The star stone believes that as production capacity is fully and effectively cleared, the new production cycle, although late, will not be absent。

Demand-side: domestic demand has recovered and the rise in domestic and foreign demand will resonate in 2021

On the demand side, the chinese economy is now showing an increasing capacity for endogenous recovery:

High rates of export growth have led to high levels of industrial production, accelerated rehabilitation of investment in manufacturing, and sustained recovery of consumer confidence in social retailing。

As many new crown vaccines around the globe are expected to land, high-income countries are expected to achieve around 70 per cent coverage by the summer of 2021, when overseas demand will also accelerate recovery。

A supply-demand gap has emerged, with capacity expansion imminent, and economic push is expected to exceed market expectations, thanks to a combination of supply and demand。

Why is the production cycle more dynamic for the economy

Unlike the inventory cycle, a more sustainable and economically driven production cycle is based on:

First, the capacity cycle is an increase in economic activity above the stock cycle。

When demand fluctuates, enterprises experience stock adjustments before channelling them to capacity utilization and equipment investments. When the supply is less than demand, it first consumes the enterprise's inventory, when it is insufficient, and when it is saturated, but still insufficient to meet the demand, the enterprise considers investing more in purchasing more equipment for production. Thus, expansion of capacity occurs only after enterprises have made sufficiently large judgements about supply and demand gaps。

Second, the expansion of productive capacity leads to investment, which is an important sub-point within the troika of the economy and is a leading indicator. At the end of 2019, investment contributed 44 per cent to GDP growth (of which manufacturing investment accounted for over 30 per cent). Consumption is a lag, driven by investment, exports and so on, and when production expands and profits rise, employment and wage levels are pushed accordingly, leading to consumption growth。

Finally, expansion of capacity can drive more links, consumption at the enterprise level. The construction process of capacity is more complex and time-consuming than the replenishment process, involving not only the enterprises themselves, upstream and downstream, but also the producers of fixed assets, such as construction enterprises, mechanical enterprises, shipping and automobile manufacturing enterprises. The expansion of productive capacity is consumption at the enterprise level. According to the widely distributed securities study, the operation of the production cycle is linked to capital expenditure (funds), construction in progress (construction), fixed assets (input) and the operation of the inventory cycle may relate only to demand and inventory。

Thus, once the production cycle begins, the driving force of the economy will be very long or strong。

Who would benefit most from the opening of a new round of capacity expansion

Once the economy is clear, business profits will pick up rapidly. The logic is as follows:

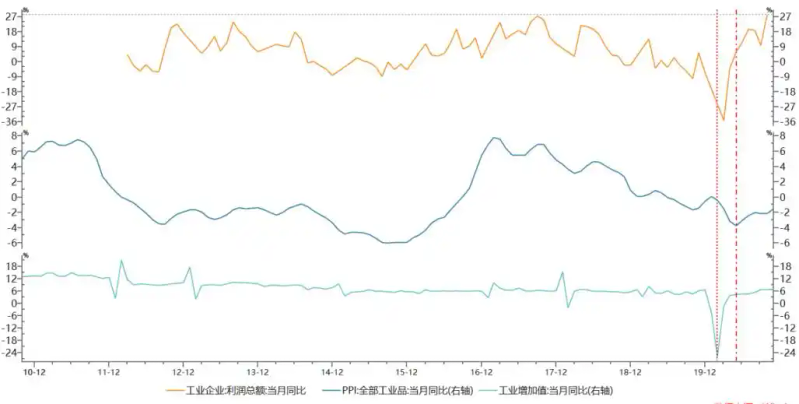

Upon completion, demand improved, business production responded first and business profits began to recover; as demand expanded further, but supply of capacity was difficult to follow quickly, supply gaps began to emerge, prices rose and business profits accelerated。

This year, this logical chain has been developed, starting with industry value added (green line, representing the level of industrial output) and showing that the firm's output responds to demand recovery. The bottom line is then seen for the profits of industrial enterprises (yellow line, representing profit), indicating that the business profits began to repair the ppi (blue line, representing the price of industrial goods) and that the supply gap led to an increase in prices and a strong rebound (yellow line)。

Total profits of industrial enterprises increased by 28 per cent in november over the same period, achieving the highest level since the availability of data. This is the first time that a new cycle of expansion of production has begun。

Starstone is expected to record the strongest growth in corporate performance in nearly 10 years in 2021, with profitability being the core driver of the stock market in 2021。

Investments need to be made in alpha, and they need to be successful。