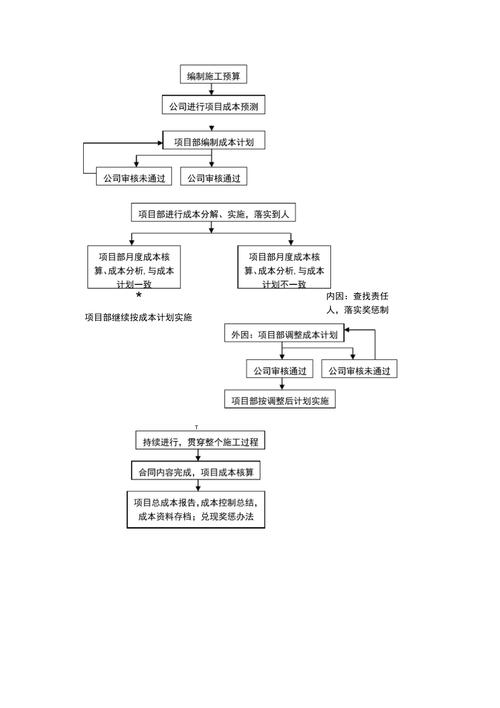

Procedures for the preparation of cost plans for the construction project

The cost-planning exercise for the construction project is a very important exercise and should not be seen simply as the preparation of a few schedules, but more importantly as the decision-making process for project cost management, i. E. The selection of technically feasible and economically sound cost-cutting options. At the same time, the target cost layer is broken down through a cost plan and implemented at every step of the construction process in order to motivate all staff to exercise cost control effectively. The procedures for preparing cost plans vary depending on the size of the project and the management requirements, and large- and medium-sized projects are generally organized in a hierarchical manner, i. E., departmental cost plans are presented by departments, followed by a consolidation of project-wide cost plans by the project manager's department; and small projects are generally centralized, i. E., departmental cost plans are prepared by the project manager's department, followed by a consolidation of project-wide cost plans. In any case, the basic procedures for its preparation are as follows:

(i) collection and collation of information is a necessary step in the preparation of cost plans. The information to be collected is also the basis for the cost plan. This information includes, inter alia:

(1) national and parent sector requirements for preparing cost plans

(2) contract contracts between the project manager and the enterprise and cost reductions, rates and other relevant technical and economic indicators issued by the enterprise

(3) relevant cost projections. Information for decision-making

(4) the construction chart budget and the construction budget for the construction project

(5) construction organization design

(6) the production capacity of the machinery used in the construction project and its utilization

(7) planning information on material consumption, material supply, labour wages and labour efficiency for construction projects

(8) information on material consumption quotas, working hours quotas, cost quotas, etc. During the plan period

(9) information on the actual implementation of past cost plans for similar projects and on the analysis of the achievement of relevant technical and economic indicators

(10) costs, quotas, information on technology-based economic indicators and experience and effective measures for savings from similar projects in the same industry

(11) the historical advanced level of the enterprise and its current best practices and measures

(12) information on advanced cost levels of similar projects abroad。

In addition, there should be an in-depth analysis of the current situation and future trends, an understanding of the advantages and disadvantages affecting cost escalation, a study of specific measures to overcome disadvantages and reduce costs, and a wealth of concrete and reliable cost information for the preparation of cost plans。

(ii) an estimate of planned costs, i. E., an estimate of the total level of production cost expenditure, after careful measurement, revision and balancing of the changes in various factors during the plan period and the various productivity-saving measures to be undertaken, based, inter alia, on, inter alia, the design, labour, machinery, energy and facilities to be invested in the project, on the basis of an analysis of the completion of the base-period cost plan, in particular, an analysis of the information available to the financial unit determining the target cost, with a view to arriving at project-wide cost-control targets. Targeting costs are determined and the overall objective is disaggregated into the relevant departments, and most teams use job decomposition。

The work decomposition method, also known as the project decomposition structure, is known abroad as wbs (workbreakdownstructure) and is characterized by the determination of cost objectives based on the design of the construction plans, the design of the project's construction organization and the technical programme developed by the enterprise, and the estimation of the actual cost of the project on the basis of actual prices and planned material, material, labour, mechanical, etc. Consumption. The practical steps are to first classify the entire project into a single element, to facilitate the small item or process for unit cost estimates, and then to estimate and summarize it from the bottom up, so that the entire project is estimated. The estimates will be aggregated taking into account risk factors and price indices, and the results will be revised。

Using the above-mentioned wbs system to carry out cost estimates, the more detailed and specific the division of work, the easier the pricing and volume of work is to be determined and the easier the work is to be estimated, the work is to be broken down from top to bottom, the cost is to be estimated from bottom to bottom, and the cost estimate for the project as a whole is to be cumulative. The cost of the engineering projects calculated on this basis is both the basis for the bid offer and the basis for cost control, as well as for comparison with the budget of the project and for estimating the level of profitability. The formula for the cost estimate is as follows: an estimate of the single x historical base x the current market x the future price cost = the number of bits the cost factor the “number of identifiable units” in the rise factor refers to tons of steel, cubic metres of wood, manual hours, etc. The “historical base cost” refers to the unit cost of the base year; and the “current market factor” refers to the price increase index from the base year to the present。

(iii) for large- and medium-sized projects, once the cost plan targets have been issued with the approval of the project manager's department, the functional units should fully engage the public in a serious discussion to identify the benefits and disadvantages of completing the current plan, taking into account the completion of the previous cost plan and taking into account the current plan targets, and propose specific measures to exploit the potential to overcome the disadvantages in order to ensure that the planned tasks are accomplished. In order for the indicators to be truly implemented, departments should, as far as possible, disaggregate them to reach groups and individuals, so that “the reduction in the target cost and the rate of reduction are fully discussed, fed and revised so that the cost plan is both realistic and a common goal of the public。

The preparatory function should also carefully discuss the cost-control indicators issued by the ministry of project manager, develop a concrete programme of technical and economic measures to be implemented, and prepare departmental cost budgets。

(iv) comprehensively balanced and the preparation of formal cost plans and cost budgets for each of the functional departments, the project manager shall first examine the soundness and feasibility of the plans and cost budgets, taking into account technical and economic measures, and establish a comprehensive balance between the plans and costs of the various departments; coordinate and integrate them; and, secondly, analyse the coordinated balance between the cost plans and the production plans, the working hours plan, the material and material supply plan, the wage costs and the wage fund plan, the financing plan, and so forth, in a holistic manner, in the event of ensuring that the cost-cutting tasks issued by the enterprise or the “target costs” of the project are met. After repeated discussions on the comprehensive balance, the final cost plan targets could serve as the basis for the preparation of the cost plan, which was formally prepared by the project manager's department and formally communicated to the enterprise's relevant departments for implementation。

Ii. Methodology for project project plan

Cost planning for the construction project is carried out primarily under the responsibility of the project manager and on a cost-preparation and decision-making basis. The key premise in preparation — setting target costs — is at the heart of the cost plan and what cost management aims to achieve. Cost targets are usually quantified in terms of overall project cost reductions and reduction rates. The orientation, comprehensiveness and predictability of project cost objectives determine the need to choose the scientific approach to targeting。

(i) cost targets for commonly used construction projects can be derived from a flat-rate estimation method, provided that the cost of the project is estimated, budgeted with a high level of strength and a relatively adequate quota, especially for construction enterprises with a more experienced construction map budget and budget preparation experience. The so-called construction chart budget is based on the construction map, which calculates the project cost on the basis of the budget flats and established rates and fees, as well as drawing works, reflecting the direct and indirect costs required to complete the construction and installation tasks of the construction project. It is the basis for the calculation of the bottom of the tender, the measure of evaluation of the bid, the criterion for controlling the project cost expenditure, measuring cost savings or overexpenditures, and the basis for evaluating the performance of the construction project. The construction budget is prepared by the construction unit (project manager departments) on the basis of the construction quota and serves as the basis for the internal economic accounting of the construction unit。

In the past, the reduction in the planned cost was usually estimated by comparing the difference with the savings resulting from the technical organization measures, which were based on the following steps taken by some construction units with the establishment of the socialist market economy:

(1) on the basis of available bids and budgetary information, determine the difference between the total price of the successful contract and the total price of the construction chart budget and the construction budget。

(2) project savings resulting from technical organizational measures are determined in accordance with technical organizational measures。

(3) items not included in the construction budget, including construction-related projects and management costs, are estimated by reference。

(4) the difference between the actual and the flat level is estimated on the basis of actual expenditure levels for the main sub-items where actual costs may significantly exceed or fall below the flat level。

(5) trial adjustment to arrive at a combined impact based on a cost-reduction plan for construction days, taking full account of unforeseen factors, time constraints and risk factors, market price fluctuations

(6) the objective cost reduction for the project as a whole is calculated in combination with the reduction rate。

Target cost reduction = target cost reduction/project budget cost reduction

(ii) the method of preparing the planned cost of the planned cost plan for the planned cost of the construction project is typically the following:

1. The construction budget method is defined as the construction budget method, which is based primarily on the physical quantities of the works in the construction plans, which is based on the construction materials consumption quota, calculates the work materials consumption and aggregates the work materials, and then reflects their construction production costs in a uniform currency. The construction production level is calculated using the construction materials consumption quota and is essentially a constant. For a construction project to achieve higher economic benefits (i. E., higher cost reductions) it is necessary to achieve the targeted cost levels of the cost plan by taking technical economy measures based on this constant to reduce consumption per unit of the consumption quota and lower prices. Therefore, in preparing the cost plan using the construction budget methodology, consideration must be given to combining the technology economy measures plan to further reduce the cost of construction production. For a particular construction project, the actual amount of the construction budget is set at a flat rate of $470. 59 million for construction materials and $14. 37 million for planned savings in technology economy measures. Calculates the planned cost。

The planned cost of the construction project = 470. 59 a14. 37 = $4. 562 million. 2. The method of technical economy measures is the method of reducing the cost of the construction project by taking into account the economic effects of the technical organization measures and economy measures planned for the construction project and then seeking the planned cost of the construction project. In formulae: planned cost of construction project = budgeted cost of construction project – planned savings from technical economy measures (reduced cost)

The cost of a construction project, at a cost of $5,622,000, after deduction of planned profits and taxes and the cost of independent enterprise management, was calculated at a budget cost of $4,842,800, resulting in savings of $287. 5 million in technical economy measures for the construction project. Calculates the planned cost。

Planned cost of construction project = 484. 22 l28. 75 = $4. 560. 7 million。

3. Cost behaviour and sexism are the application of fixed and variable costs to the preparation of cost plans, which are divided into fixed and variable costs, mainly based on cost behaviour, as planned costs. A breakdown of costs could be used。

(1) material costs. There is a direct link to production, which is a variable cost。

(2) labour costs. In the form of hourly wages, the wages of productive workers are fixed costs. Because wages are paid regardless of whether the production task is completed or not, there is no direct link to the increase or decrease in production. In the case of an excess piece salary, the element of the piece salary is a cost of work change, and the element of bonus, benefit and floating wage shall also be included in the cost of work change。

(3) mechanical usage. Some of these costs vary with production increases or decreases, such as fuel and power costs. Some costs do not vary with production, such as depreciation of machinery, major repairs, mechanics, wages of operators, etc., are fixed costs. In addition, there are machine off-site transportation costs and frequent repair costs such as mechanical assembly dismantling, replacement of spare parts and lubrication tests, which are not directly used for production and do not change with a positive percentage of output, but are less shared when production capacity is fully utilized and production growth is increased, and larger when production is reduced, so that they are part of the half-changing cost between fixed and variable costs; fixed and variable costs can be classified in proportion。

(4) other direct costs. The cost of water, electricity, wind, gas, etc., as well as the cost of secondary handling of materials on-site, mostly associated with production, are variable costs。

(5) construction management costs. Most of them are not directly related to increases or decreases in production within a given production range, such as theft of working people, exclusion of productive workers, additional wage drums, office fees, travel expenses, use of fixed assets, employee education funds, higher management fees, etc., which are essentially fixed costs. In addition, labour insurance clothing, summer cooling, winteric supplies, and the prescribed standards for use in the labour sector are essentially fixed-cost, technical safety measures, health-care fees, mostly related to output, are non-changing in the form of fees for the use of tools, fixed-cost furniture for administrative use, tools for workers, and different regulatory systems. Some enterprises are equipped with tools for mechanics, electricians, steel bars, cars, pistons, and grinders, which are regularly replaced by old ones, which are fixed-cost, while the fixed number of labour, pricing packages for tools for civilian workers, carpentry, as well as for paint workers, are subject to change costs。

When costs are routinely divided into fixed and variable costs, the following formula can be used: construction project

For a construction project, the total variable cost measured by sub-divisions was $393. 01 million and the fixed cost was $6. 307 million. Calculates the planned cost。

The planned cost of the construction project of $23. 9301 million, or $10. 6307 million, was $4. 5608 million. 4 on a realistic basis, this is the basis for the planned cost to be controlled by the relevant functional unit (persons) of the construction project manager based on the material analysis of the project's construction chart budget. Based on the actual level and requirements for the execution of the construction quota by the construction project manager, the planned costs are calculated at the expense of the functional units。

(1) the planned costs of labour costs are calculated by the labour unit (personnel) of the project management team。

The planned cost of labour costs = the rate of wages at the actual level of the planned work volume x, the planned work volume = 2 (the fixed number of days worked on a project volume x), and the daily rate may be increased, as appropriate, depending on the actual level, taking into account advancedness。

(2) the planned cost of material costs is calculated by the material unit (personnel) of the project management team。

Planned cost of materials (planned usage of major materials x actual price) x x (planned usage of decorative materials x actual value) x ten (construction)