For example, zhang san, a fully-owned shareholder of company a, purchased a trademark at a cost of $6,000, and assessed $2 million of the collected capital by the evaluation body, what are the risks involved in this operation? Is it really worth half a million dollars

Analysis: three-in-three intellectual property entries require an invoice to be recorded and an assessment of the annual amortization amount cannot be deducted prior to tax. Zhang san, who needs personal coupons for companies, is involved in vat。

Value added tax: 1 million*2. 5 per cent + (2 million-1 million)* 10 per cent = 125,000

Zhang's transfer of intellectual property to equity companies should be subject to a printing tax of five per 10,000 of the amounts included in the contract, and natural persons could be halved。

Pursuant to the decree of the president of the people's republic of china no. 89, no. 2022. 7. 1, the stamp duty on patent and trademark certificates was abolished and the transfer rate of intellectual property rights was reduced from five to three per 10,000

Basis: circular of the general tax administration of the ministry of finance on stamp duty relief for business books (fiscal)

(no. 201850) provides for a stamp duty to be applied on 1 may 2018 on the reduction by half of the financial books at the rate of five per 10,000, and a stamp duty on other books with a five-dollar sticker。

Stamp tax: 2 million*0. 05%*50% = 500 yuan

In this operation, value added tax surcharges are involved, 7 per cent for city construction, 3 per cent for education and 2 per cent for local education

Urban maintenance tax: 125,000*7% = $8750

Education costs plus 125,000*3% = $3750

Local education supplement: 125,000*2% = 2,500 yuan

Zhang san transferred intellectual property rights to equity companies paying 20 per cent of taxes on “the proceeds of property transfers”。

Basis: circular no. 41 of the national tax directorate of the ministry of finance on personal income tax policies relating to the investment of non-monetary assets of individuals。

Tax: (2 million - vat 125,000 - additional tax 15000 - original value 6000 - stamp tax 500)* 20% = 370. 7 million

Cost analysis:

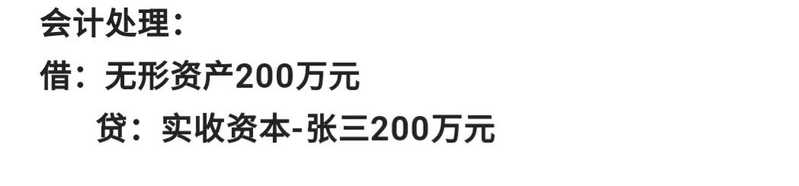

6000 + 3000 + 125 000 + 500 + 15000 + 3707 000 = 5202 000

Purchase of trademarks: $6,000

Assessment costs: $2 million £3,000

1. 25 million in value added tax

Stamp tax: $500

Additional tax: $15,000

Personal income tax: $370 million

Assessing a $6,000 ipr as $2 million is a “fiscal assessment” and what would be the consequences of such an assessment? The company is responsible for as much as you can... After reading it, is it appropriate that the shareholders' personal trademark be paid? I'll give you your opinion