“prisoner's plight” is a classic example of game theory, ranging from childhood to people-to-people life, to competition between businesses and even between nations. There is then a “prisoner dilemma” in investment in rights. Today we are trying to explore the reflection of the “prisoner dilemma” in equity-like investments and to find solutions to this dilemma。

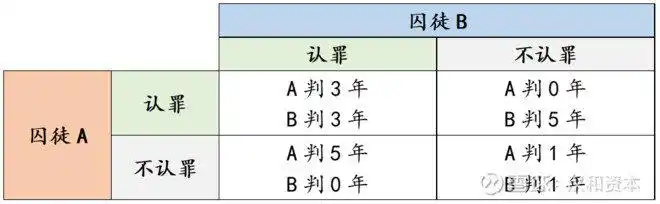

The theory that the “prisoners' dilemma” was raised in the 1950s can be described by a simple story: two suspects, a and b, were captured by the police after committing the crime and held in two rooms for interrogation. The police knew that the two men were guilty, but lacked sufficient evidence and hoped that the suspects would be allowed to confess their guilt. The police then told the two suspects separately:

A: if both persons do not plead guilty, the sentence is one year each

B: three years each if both persons plead guilty

C: if one of them pleads guilty and the other pleads not guilty, the non-guilty party is given a five-year sentence and the guilty party is rewarded with acquittal. If a pleads guilty, b pleads not guilty, b is sentenced to five years, a is acquitted and vice versa

It is clear that, for both suspects a and b, the choice not to plead guilty is the best solution to the above situation, and both have been sentenced to only one year's imprisonment. But think carefully, this optimal solution does not reach the final equilibrium, or is not possible, meaning that it is not in the best interests of both a and b suspects. Why do you say that

In the case of suspect a, the option of “guilty plea” or “non-guilty plea” may be taken into account before choosing. In the case of suspect b's “guilty plea”, in the case of suspect b, the option of guilty plea is 3 years each with suspect b, the option of not guilty plea is 5 years each, and in the case of suspect a, the option of guilty plea is the best for suspect a; in the case of suspect b's “guilty plea”, the option of not guilty plea is 1 year each with suspect b, but in the case of guilty plea, suspect b is sentenced 5 years each, while in the case of suspected b's choice of “no guilty plea”, a's best sentence is “guilty plea”. In turn, for suspect b, it can be analysed that “guilty pleas” are the best for himself. Thus, in the above-mentioned examples, both a and b suspects will ultimately choose “guilty pleas”, although this is the best option for individuals a and b to maximize their benefits, but not for both a and b as a whole。

The “prisoner dilemma” also exists in a number of other areas, such as business competitions where lower prices for enterprises can gain a greater market share, but when there is a price war in the industry, it affects the interests of all firms in the industry; when there is danger, for example, it is the best option for individuals to run out of the building at the fastest speed possible, but the fastest possible way out of the building leads to congestion and even to stepping, which increases the risk of group injury. The same holds true for equity investments, for a simple example, assuming that there are two investors, a and b, who do not know each other and do not communicate with each other, in a small closed trading market (the number of people involved in the transaction is very low), and that one day there was a sudden news of a profit-making event, at which time there were several options for the two investors:

A: when the choice was made to hold the shares, the shares fell by 3 per cent and both lost 3 per cent

B: a 5 per cent drop in shares and a 5 per cent loss for both

C: 1 per cent for the seller and 10 per cent for the holder

In this example, the best option for both investors as a whole was to choose to hold them, and both had a loss of 3 per cent. However, applying the analysis in the case of former suspects, it can be found that the ultimate stabilizing result must be that both a and b investors chose to sell because the choice of maximizing the benefits of both investors themselves was sold. The result was a 5 per cent loss for both investors。

This is, of course, a significantly simplified model, and the actual market is much more complex than this example, with far more than two first traders involved, and the choice that can be made is not just to hold or sell, how much to sell and when to sell. But a simple model does not imply a mistake of conclusion, and the choices made by participants in a real market in the face of information, like those made by investors in a and b in this example, are based on the expectation of maximization of their own interests, but the result is that every investor in the market suffers even greater losses。

Then why does the issue of "prisoners' plight" exist in investment? We look at the following:

1. The root cause of “prisoners' plight” is the contradiction between individual reason and collective reason, i. E. Collective irrationality resulting from individual reason. In the first example, the individual conduct of the two suspects in pursuit of their own interests was a rational choice for themselves, but the result was a more unfavourable outcome for both. The same is true of the second investment-related case, where the choice of sale is a rational choice for both investors, but the result is that both of them will have to bear greater losses。

The short-term impact factor is unpredictable, i. E. The investor is unable to make an accurate judgement in advance of sudden information, whether beneficial to the business or beneficial to the air. As in the above-mentioned example, investors can only make a sale or hold of an operational choice after an emergency has come out and become aware of it. The result is that a large number of investor-based transactions occur within a short period of time。

Each individual investor is independent, i. E. As a single investor in the market, it is impossible to know what other investors in the market think. Also, as in the two cases mentioned above, the prisoners who were tried in separate rooms, as well as the investors who did not know each other and did not communicate with each other, were unaware of what the other party would decide before making a judgement. This is why people choose to maximize their expectations based on their own interests。

It is certain that, at this point, you will expect solutions to the “prisoner dilemma” of investment, but the conclusion may disappoint you that the problem of the “prisoner dilemma” of investment cannot be solved, because you are neither aware of the idea of the whole market, nor able to anticipate events, nor can you resolve the contradiction between individual and collective rationality. But you need not be too disappointed to be able to resolve the problem of “prisoners' plight”, which does not mean that there is no good response. What we need to do is accept the fact that there is a “prisoner dilemma” in the investment and jump out of the “prisoner dilemma” to think about the investment。

1. The fact that “prisoners' plight” exists in the investment received. We often lament that “markets are too irrational” when markets are booming or falling, and that is the collective irrationality of all participating investors in the market. The choice of a large number of investors in the market to maximize their own benefits could instead exacerbate short-term stock price volatility. In other words, the collective irrationality resulting from individual rationality in the “prisoners' plight” is manifested in the “volatilization” of stock prices. Volatility is an inherent attribute of equity-type investments, for which no investor is immune and can only endure. Thus, the fact that there is a “prisoner dilemma” in the acceptance of investments is, in effect, to endure fluctuations in asset prices during equity investments。

(b) jumping out of “prisoners' plight” to think about investment. When we understand that the “prisoner dilemma” of investment is actually the volatility of stock prices, it is easy to think about investment by jumping out of the “prisoner dilemma”, which concerns changes in the long-term value of assets rather than short-term price fluctuations. Why focus on the long-term value of assets? The contradiction of individual and collective rationality, which is one of the root causes of the “prisoner dilemma” of investment, should more accurately be described as a contradiction of short-term individual and collective rationality. Returning to the above examples, investors a and b did not analyse the negative impact of this news on the long-term value of the enterprise invested, and if there is no negative impact on the long-term value of the enterprise, the “sell-out” option based on maximizing the individual's own interests is an irrational performance rather than the option of maximizing their own interests; and if there is a negative impact on the long-term value of the enterprise, there is no need to worry that even the 5 per cent drop in the stock price option will be sold, because if it is not sold, more will be lost thereafter. Thus, the “prisoner dilemma” of investment is manifested at the level of short-term transactions, and investment decisions based on the long-term value of the enterprise are not constrained。

At the end:

The “prisoner dilemma” manifests itself in investment in practice in terms of the volatility of asset prices, which is an inherent attribute of equity-type investments that cannot be avoided by investors, and therefore there is no direct solution to the “prisoner dilemma” of investments. All investors can do is endure fluctuations in asset prices and accept the inherent fact that the “prisoner dilemma” of investment exists. However, the “prisoner dilemma” of investments is also limited to the short-term transactional dimension, and is not limited to judgements based on the long-term value of assets. So the only way out of the "prisoner dilemma" of investment is to get out of it, get on a higher level and think and judge investment in the longer term