The survey of accounting essentials in the digital economy . Doc is shared by members and can be read online, and more of the relevant research of accounting basics in the digital economy . Doc (4-page collection) is available for on-line search。

The digital economy explores the underlying accounting assumptions of the digital economy. The digital economy, through the identification and filtering, storage and use of digital knowledge and information, is the culmination of the re-integration and optimization of resources, a new economic system following the agricultural and industrial economy, which has undergone fundamental changes in the overall economic environment and economic activity. The “digital economy” is divided into two forms: digital industrialization, i. E. The industrialization of information, an industry that integrates the production of information products, information development and information services; second is the digitalization of industry, i. E. The development of the use of traditional industries in units to increase productivity by integrating with information (ii) the basic characteristics of the digital economy. Data become the key factors of production driving economic development, using data and information networks as vehicles, and, as a production factor, promoting supply-side structural reforms through the flow of information to enhance overall social productivity。

According to the world bank analysis, for every 10 per cent increase in digitization, 0. 5 per cent of GDP growth, 0. 5 per cent of gross domestic product, 0. 5 per cent of gross domestic product (GDP) per capita economic development, digitalized information connectivity, economic cooperation is no longer subject to time and space constraints, but will also be shortened over the course of operations. Building new types of information is the basic digital economy of digital economic development. Building new types of information is required in traditional agriculture, industry, services, etc., to enable resource-sharing through modern information technology, optimize supply-and-demand linkages, promote industrial integration. As a result, new information-based systems are being built, internet-based information highways are being built, infrastructure such as sensory, digitalized facilities are being installed, resource allocation is being fully optimized, data information is being improved as a new digital economy for producers and consumers, and digital information is becoming a new digital economy for producers and consumers。

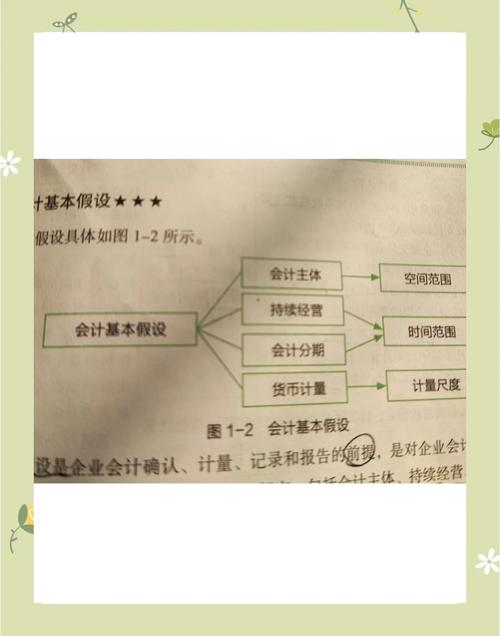

The underlying accounting assumptions, which are premised on accounting recognition, measurement, recording and reporting, are reasonable assumptions about the timing, spatiality, etc. Of accounting, including the emergence of new digital economic developments in accounting subjects, going concern, accounting segmenting and monetary measurement, and fundamental changes in the socio-economic environment that have had some impact on current accounting theory (i) the effect on current accounting body assumptions (i) the effect on current accounting theory (i) the effect of cross-regional, cross-industry consolidation, which would result in multiple layers of accounting or oversight, the impact on existing accounting body assumptions under a spatial digital economy under accounting recognition, measurement and reporting, on one hand, under economic integration, with a high frequency of capital flows under the multilayered digital economy, a large number of networked economic agents, a large change in the size of the economic entity, and the emergence of strong alliances into liquidation at any time, and therefore a multi-layered feature under which, in addition, the extent to which operations are expected to continue to be subject to increasing competition, are expected to be subject-to-competering, assuming that the effects of a continuing operation are expected to be sustained and to be sustained。

On the one hand, there is increased uncertainty in the operating environment, with accounting entities readily entering the new economy of the liquidation process, with adequate sharing of information, increased market competitiveness, increased market uncertainty, economic agents taking over market share, constantly seeking innovation and financing the enhancement of research and development in high-technology technologies, but once research and development fails, economic agents will enter the liquidation process with only 10 per cent of the success rate of high-technology enterprise development in the united states, while optimizing resource allocation rates, restructuring and merging accounting entities and increasing economic agents to maximize economic benefits, allowing for the rapid pooling of high-quality resources and optimized industrial structures, for “short-term” operations, for a “short-term” operation, for a period of time, for a period of time, for an appropriate intervention or exit, or for a post-mandate declaration of organizational break-up (iii) impact on the accounting stagger assumptions。

(iv) impacts on monetary measurement assumptions: monetary measurement assumptions that monetary units can be used to express transactions or transactions, finance staff can use monetary econometric operations and transmit their measurements to the digital economy, with some limitations in monetary measurement, financial reporting that discloses a large amount of non-monetary information under the current monetary accounting system, some of which is of value, such as human resources of economic agents, brand value added, patent value, geographical advantages, etc.; therefore, current financial reporting based solely on monetary measurement is difficult to measure in monetary terms to meet the information needs of users, on the other hand, the rapid development of new economies with regularization of non-monetary payments, “internet+”, the increasing number of information payments, the emergence of third-party electronic agents of transactions and new electronic payment platforms, the shift in monetary nature from physical to intangible to optimal accounting assumptions under the digital economy. The second objective of external disclosure information is to consolidate related industrial chain units into a “accountant organization” to provide external information in a digital economy in which the economic organization is the main accounting entity and other relevant links in the industrial chain are the supporting accounting entity, with the joint disclosure of information as an accounting organization。

Third is that accounting organizations can reflect business results as a whole, that self-accounting entities within an accounting organization can disclose business results individually to society, that each accounting organization can come together with several independent units, that individual units can publish business results externally, or that the individual unit can publish business results jointly with other related units of the industry (ii) optimize business continuity assumptions, that the “continuing business” evolves into “risk operations”, that there may be risks associated with a “risk business scenario”, that there is a need for a “risk business scenario” digital economy, that the economic environment changes rapidly, that economic organizations can move into a state of insolvency liquidation at any time, and that the business entity's operational life is reduced by a “risk business assumption”, that the risk business assumption is one that a combination of a continuing business assumption and a liquidation assumption reflects a business start-up, management of operations, payment of funds, etc., that there may be risks associated with the establishment of a “risk-business scenario”, that can lead to risk identification and risk avoidance of risk, that there is a need to be an effective financial reporting basis for reporting, and that there is a need for information to be an efficient reporting by the。

Different review permissions may also be granted to different users of information to provide targeted financial information, improve the quality of the use of information (iv) optimize the monetary measurement assumptions, introduce monetary measurement as a preponderance, and combine monetary and non-monetary measurement assumptions. On the one hand, where non-monetary measurement is not possible, where intangible assets such as brand brands, patented technologies, non-proprietary technologies are present, and cannot be measured in monetary terms, it is possible to activate non-monetary measures that require the use of monetary equivalents, such as the selection of new e-measures, but under the digital economy, the disclosure of these resources to the greatest extent possible of the potential wealth, value and profitability of a pool of highly qualified experts, technicians and workforces is required to be measured in terms of experts, engineers' functional titles, professional levels, and their inventions. Rethinking j. Accounting study on the basic accruals of financial accounting, 2002 (01): 5-10+64. 2 li hongjiang. Friends of accounting under the age of the knowledge economy, j. Accounting friends (mid-term), 2006 (08): 85-86. (author: chinese academy of tropical agriculture institute of fragrance beverages)。